What is Global Battery Oxygen Concentrator Market?

The Global Battery Oxygen Concentrator Market is a rapidly evolving segment within the broader medical device industry. These devices are designed to provide supplemental oxygen to individuals who require respiratory support, particularly those with chronic obstructive pulmonary disease (COPD), asthma, or other respiratory conditions. The market is driven by the increasing prevalence of respiratory diseases, the aging population, and the growing demand for portable and efficient oxygen delivery systems. Battery oxygen concentrators are particularly appealing because they offer mobility and convenience, allowing users to maintain an active lifestyle while receiving the necessary oxygen therapy. Technological advancements have led to the development of more compact, lightweight, and energy-efficient models, further boosting their adoption. Additionally, the market is witnessing a surge in demand due to the COVID-19 pandemic, which has highlighted the importance of respiratory care devices. As healthcare systems worldwide continue to prioritize patient-centered care, the Global Battery Oxygen Concentrator Market is poised for significant growth, driven by innovation and the increasing need for home-based healthcare solutions.

Portable Battery Oxygen Concentrator, Fixed Battery Oxygen Concentrator in the Global Battery Oxygen Concentrator Market:

Portable Battery Oxygen Concentrators are a key component of the Global Battery Oxygen Concentrator Market, offering users the flexibility to move freely while receiving oxygen therapy. These devices are compact, lightweight, and designed for ease of use, making them ideal for individuals who lead active lifestyles or require oxygen support while traveling. The portability of these concentrators is a significant advantage, as it allows users to maintain their independence and engage in daily activities without being tethered to a stationary oxygen source. Technological advancements have led to the development of portable concentrators with longer battery life, quieter operation, and improved oxygen delivery efficiency. These features enhance user experience and satisfaction, contributing to the growing popularity of portable models. On the other hand, Fixed Battery Oxygen Concentrators are designed for stationary use, typically in a home or healthcare setting. These devices are larger and more powerful than their portable counterparts, providing a continuous and reliable source of oxygen for patients who require constant respiratory support. Fixed concentrators are often used for patients with severe respiratory conditions who spend most of their time at home. They are equipped with robust filtration systems and advanced monitoring features to ensure optimal oxygen delivery and patient safety. While they lack the mobility of portable models, fixed concentrators offer higher oxygen output and are generally more cost-effective for long-term use. The choice between portable and fixed battery oxygen concentrators depends on the patient's lifestyle, mobility needs, and the severity of their respiratory condition. Both types of concentrators play a crucial role in the Global Battery Oxygen Concentrator Market, catering to diverse patient needs and preferences. As the market continues to evolve, manufacturers are focusing on enhancing the performance, efficiency, and user-friendliness of both portable and fixed models to meet the growing demand for oxygen therapy solutions.

Hospital, Health Center, Residential, Others in the Global Battery Oxygen Concentrator Market:

The usage of Global Battery Oxygen Concentrators spans various settings, including hospitals, health centers, residential areas, and other environments where respiratory support is needed. In hospitals, these devices are essential for providing supplemental oxygen to patients with acute respiratory conditions or those recovering from surgery. Battery oxygen concentrators offer a reliable and efficient solution for delivering oxygen therapy in emergency rooms, intensive care units, and general wards. Their portability allows healthcare professionals to easily transport them between different departments, ensuring that patients receive timely and adequate oxygen support. In health centers, battery oxygen concentrators are used to manage chronic respiratory conditions, such as COPD and asthma. These devices enable healthcare providers to offer personalized oxygen therapy to patients, improving their quality of life and reducing the risk of complications. Health centers often use a combination of portable and fixed concentrators to accommodate the varying needs of their patients. In residential settings, battery oxygen concentrators provide a convenient and effective solution for individuals who require long-term oxygen therapy. These devices allow patients to receive continuous oxygen support in the comfort of their homes, promoting independence and enhancing their overall well-being. The availability of portable models enables users to engage in outdoor activities and social interactions, contributing to a more active and fulfilling lifestyle. Other areas where battery oxygen concentrators are utilized include nursing homes, rehabilitation centers, and palliative care facilities. In these settings, the devices play a crucial role in managing respiratory conditions and ensuring patient comfort. The versatility and adaptability of battery oxygen concentrators make them an invaluable tool in various healthcare environments, supporting the diverse needs of patients and healthcare providers alike.

Global Battery Oxygen Concentrator Market Outlook:

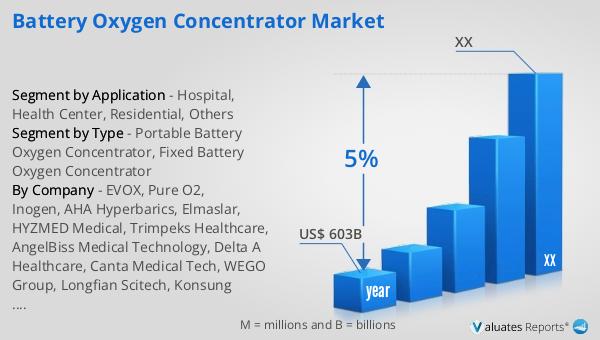

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory underscores the increasing demand for innovative medical technologies and solutions that cater to the evolving needs of healthcare systems worldwide. The medical device industry encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a critical role in enhancing patient care and improving health outcomes. The projected growth of the market is driven by several factors, including the rising prevalence of chronic diseases, advancements in medical technology, and the growing emphasis on personalized medicine. Additionally, the aging global population and increasing healthcare expenditure are contributing to the expansion of the medical device market. As healthcare providers continue to seek efficient and cost-effective solutions to meet the demands of modern healthcare, the medical device industry is poised for sustained growth and innovation. The Global Battery Oxygen Concentrator Market is a significant segment within this broader industry, reflecting the increasing need for respiratory care solutions and the ongoing advancements in oxygen therapy technology.

| Report Metric | Details |

| Report Name | Battery Oxygen Concentrator Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | EVOX, Pure O2, Inogen, AHA Hyperbarics, Elmaslar, HYZMED Medical, Trimpeks Healthcare, AngelBiss Medical Technology, Delta A Healthcare, Canta Medical Tech, WEGO Group, Longfian Scitech, Konsung Medical Group, Shanghai Huifeng Medical Instrument |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |