What is Global Blood and Fluid Warming Rapid Infuser Market?

The global Blood and Fluid Warming Rapid Infuser market is a specialized segment within the medical devices industry that focuses on devices designed to rapidly warm blood and other fluids before they are infused into patients. This is particularly crucial in emergency situations, surgeries, and intensive care units where patients may require large volumes of blood or fluids quickly. The warming process helps to prevent hypothermia, a condition where the body loses heat faster than it can produce it, which can be life-threatening. These devices are essential in maintaining the patient's body temperature, thereby improving the overall outcome of medical treatments. The market for these devices is driven by the increasing number of surgical procedures, rising incidences of trauma cases, and the growing prevalence of chronic diseases that require frequent blood transfusions or fluid replacements. Technological advancements in medical devices and the increasing adoption of these devices in healthcare settings are also contributing to the market's growth.

Stationary, Portable in the Global Blood and Fluid Warming Rapid Infuser Market:

The Global Blood and Fluid Warming Rapid Infuser Market can be broadly categorized into two types: stationary and portable devices. Stationary blood and fluid warmers are typically larger and are designed to be used in fixed locations such as hospitals and clinics. These devices are often integrated into the hospital's central heating system and can handle large volumes of fluids, making them ideal for use in operating rooms, intensive care units, and emergency rooms. They are equipped with advanced features such as precise temperature control, alarms for temperature deviations, and the ability to warm fluids to body temperature quickly and efficiently. On the other hand, portable blood and fluid warmers are smaller, lightweight, and designed for use in various settings, including ambulances, military field hospitals, and remote locations. These devices are battery-operated or can be plugged into a vehicle's power supply, making them highly versatile and convenient for use in emergency situations where immediate warming of fluids is required. Portable warmers are also used in home healthcare settings for patients who require regular infusions or transfusions. Both stationary and portable devices play a crucial role in ensuring that patients receive warm fluids, thereby preventing hypothermia and improving patient outcomes. The choice between stationary and portable devices depends on the specific needs of the healthcare facility and the nature of the medical procedures being performed.

ICU, Emergency Room, Operating Room, Infusion & Dialysis Room, Others in the Global Blood and Fluid Warming Rapid Infuser Market:

The usage of Global Blood and Fluid Warming Rapid Infuser Market devices spans across various critical areas in healthcare settings, including the Intensive Care Unit (ICU), Emergency Room (ER), Operating Room (OR), Infusion & Dialysis Room, and other specialized medical areas. In the ICU, these devices are essential for patients who are critically ill and require continuous monitoring and treatment. The rapid infusers help in maintaining the patient's body temperature during prolonged treatments and surgeries, thereby reducing the risk of complications. In the Emergency Room, the need for rapid infusion of warm fluids is paramount, especially in trauma cases where patients may have lost a significant amount of blood. The quick warming and infusion of fluids can be life-saving in such scenarios. In the Operating Room, blood and fluid warming devices are used during surgeries to ensure that the fluids being administered to the patient are at body temperature, which helps in maintaining the patient's core temperature and reduces the risk of hypothermia. In Infusion & Dialysis Rooms, these devices are used for patients undergoing regular treatments that involve the administration of large volumes of fluids. The warming of these fluids helps in improving patient comfort and reducing the risk of adverse reactions. Other areas where these devices are used include neonatal care units, where maintaining the body temperature of newborns is critical, and in military field hospitals, where rapid response and treatment are required. Overall, the usage of blood and fluid warming rapid infusers is integral to modern medical practices, ensuring patient safety and improving treatment outcomes.

Global Blood and Fluid Warming Rapid Infuser Market Outlook:

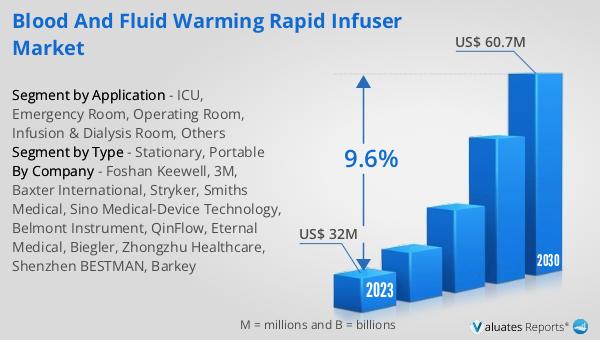

The global Blood and Fluid Warming Rapid Infuser market was valued at US$ 32 million in 2023 and is anticipated to reach US$ 60.7 million by 2030, witnessing a CAGR of 9.6% during the forecast period 2024-2030. This significant growth can be attributed to several factors, including the increasing number of surgical procedures, the rising incidence of trauma cases, and the growing prevalence of chronic diseases that necessitate frequent blood transfusions or fluid replacements. Additionally, technological advancements in medical devices and the increasing adoption of these devices in healthcare settings are contributing to the market's expansion. The demand for both stationary and portable blood and fluid warmers is expected to rise as healthcare facilities continue to prioritize patient safety and improve treatment outcomes. The market's growth is also supported by the increasing awareness among healthcare professionals about the importance of maintaining body temperature during medical procedures. As a result, the adoption of blood and fluid warming rapid infusers is expected to become more widespread, further driving the market's growth.

| Report Metric | Details |

| Report Name | Blood and Fluid Warming Rapid Infuser Market |

| Accounted market size in 2023 | US$ 32 million |

| Forecasted market size in 2030 | US$ 60.7 million |

| CAGR | 9.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Foshan Keewell, 3M, Baxter International, Stryker, Smiths Medical, Sino Medical-Device Technology, Belmont Instrument, QinFlow, Eternal Medical, Biegler, Zhongzhu Healthcare, Shenzhen BESTMAN, Barkey |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |