What is Global Alkaline Electrolyte Fuel Cell Market?

The Global Alkaline Electrolyte Fuel Cell Market refers to the worldwide industry focused on the development, production, and distribution of alkaline electrolyte fuel cells. These fuel cells are a type of electrochemical cell that converts chemical energy from a fuel into electricity through a chemical reaction with oxygen or another oxidizing agent. Alkaline electrolyte fuel cells are known for their high efficiency and ability to operate at lower temperatures compared to other types of fuel cells. They are particularly useful in applications where reliability and efficiency are critical, such as in space missions, military operations, and various forms of power generation. The market encompasses a wide range of activities, including research and development, manufacturing, and sales of these fuel cells, as well as the infrastructure needed to support their use. The growth of this market is driven by increasing demand for clean and efficient energy solutions, advancements in fuel cell technology, and supportive government policies promoting the use of renewable energy sources.

Cycle, Fixed, Soluble in the Global Alkaline Electrolyte Fuel Cell Market:

In the context of the Global Alkaline Electrolyte Fuel Cell Market, the terms Cycle, Fixed, and Soluble refer to different types of fuel cells and their operational characteristics. Cycle-based alkaline electrolyte fuel cells are designed for applications where the fuel cell needs to be repeatedly charged and discharged. These are typically used in scenarios where there is a need for a reliable and consistent power supply over long periods, such as in backup power systems or remote power generation. Fixed alkaline electrolyte fuel cells, on the other hand, are designed for stationary applications where the fuel cell remains in a fixed location. These are commonly used in industrial settings, power plants, and other large-scale power generation facilities. Fixed fuel cells are known for their durability and ability to provide a steady and continuous power output. Soluble alkaline electrolyte fuel cells are a more recent development and involve the use of a soluble electrolyte that can be easily replenished or replaced. This type of fuel cell offers the advantage of easier maintenance and potentially lower operational costs. Soluble fuel cells are being explored for a variety of applications, including portable power devices and smaller-scale power generation systems. Each of these types of fuel cells has its own set of advantages and challenges, and their use depends on the specific requirements of the application. For example, cycle-based fuel cells are ideal for applications where portability and flexibility are important, while fixed fuel cells are better suited for large-scale, stationary power generation. Soluble fuel cells, with their ease of maintenance, are being considered for applications where operational efficiency and cost-effectiveness are key considerations. The choice between these types of fuel cells depends on factors such as the required power output, operational environment, and maintenance capabilities. As the technology continues to evolve, we can expect to see further advancements in each of these areas, leading to more efficient and versatile fuel cell solutions.

Space Vehicle, Military Equipment Power Supply, Automotive Power Supply, Civil Power Generation Device, Others in the Global Alkaline Electrolyte Fuel Cell Market:

The Global Alkaline Electrolyte Fuel Cell Market finds its usage in a variety of areas, including space vehicles, military equipment power supply, automotive power supply, civil power generation devices, and other applications. In space vehicles, alkaline electrolyte fuel cells are highly valued for their high efficiency and reliability. They have been used in various space missions to provide a dependable source of power for spacecraft systems and instruments. The ability to operate in extreme conditions and provide a continuous power supply makes them ideal for space exploration. In military equipment, these fuel cells are used to power various devices and systems, including communication equipment, surveillance systems, and portable power units. The military values these fuel cells for their robustness, reliability, and ability to operate in harsh environments. In the automotive industry, alkaline electrolyte fuel cells are being explored as a potential power source for electric vehicles. They offer the advantage of longer driving ranges and shorter refueling times compared to traditional batteries. This makes them an attractive option for the development of next-generation electric vehicles. In civil power generation, these fuel cells are used in a variety of applications, including backup power systems, remote power generation, and grid stabilization. Their ability to provide a steady and reliable power supply makes them suitable for use in critical infrastructure and emergency power systems. Other applications of alkaline electrolyte fuel cells include portable power devices, industrial power systems, and renewable energy integration. The versatility and efficiency of these fuel cells make them a valuable solution for a wide range of power generation needs. As the demand for clean and efficient energy solutions continues to grow, the usage of alkaline electrolyte fuel cells is expected to expand across various sectors.

Global Alkaline Electrolyte Fuel Cell Market Outlook:

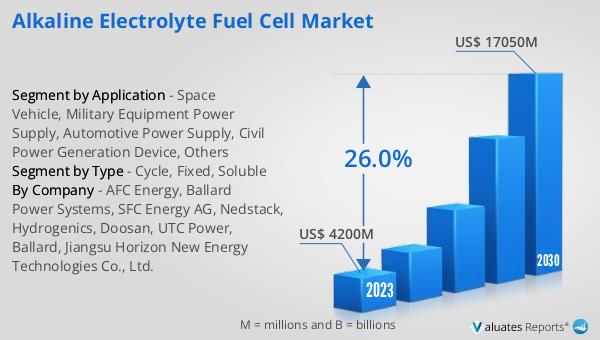

The global Alkaline Electrolyte Fuel Cell market was valued at US$ 4200 million in 2023 and is anticipated to reach US$ 17050 million by 2030, witnessing a CAGR of 26.0% during the forecast period 2024-2030. This significant growth reflects the increasing demand for efficient and reliable energy solutions across various industries. The market's expansion is driven by advancements in fuel cell technology, supportive government policies, and the growing need for clean energy sources. The high growth rate indicates a strong interest and investment in the development and deployment of alkaline electrolyte fuel cells. As more industries recognize the benefits of these fuel cells, such as their high efficiency, reliability, and ability to operate in diverse environments, the market is expected to continue its upward trajectory. The projected growth also highlights the potential for innovation and further advancements in fuel cell technology, which could lead to even more efficient and versatile energy solutions in the future.

| Report Metric | Details |

| Report Name | Alkaline Electrolyte Fuel Cell Market |

| Accounted market size in 2023 | US$ 4200 million |

| Forecasted market size in 2030 | US$ 17050 million |

| CAGR | 26.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | AFC Energy, Ballard Power Systems, SFC Energy AG, Nedstack, Hydrogenics, Doosan, UTC Power, Ballard, Jiangsu Horizon New Energy Technologies Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |