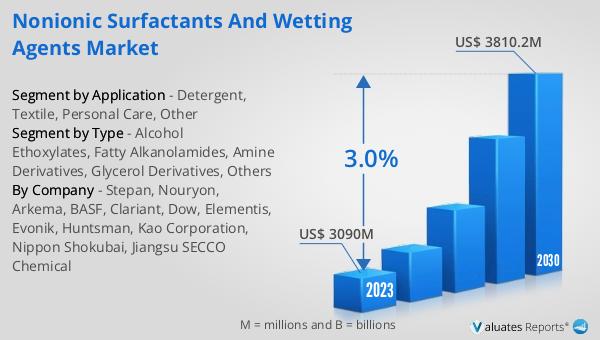

What is Global Low Foam Nonionic Surfactants Market?

The Global Low Foam Nonionic Surfactants Market is a specialized segment within the broader surfactants industry. These surfactants are unique because they produce minimal foam, making them ideal for applications where excessive foaming can be problematic. Nonionic surfactants do not carry any charge, which means they are less likely to interact with other ions in a solution, providing stable performance across a wide range of conditions. They are widely used in various industries, including detergents, textiles, personal care, petrochemicals, and paints & coatings. The market for these surfactants is driven by their versatility, effectiveness, and the growing demand for high-performance cleaning and emulsifying agents. As industries continue to seek more efficient and environmentally friendly solutions, the demand for low foam nonionic surfactants is expected to grow. These surfactants are also favored for their biodegradability and lower toxicity compared to other types of surfactants, making them a preferred choice in applications where environmental impact is a concern.

Alcohol Ethoxylates, Fatty Alkanolamides, Amine Derivatives, Glycerol Derivatives, Others in the Global Low Foam Nonionic Surfactants Market:

Alcohol Ethoxylates, Fatty Alkanolamides, Amine Derivatives, and Glycerol Derivatives are key components in the Global Low Foam Nonionic Surfactants Market. Alcohol Ethoxylates are produced by the reaction of fatty alcohols with ethylene oxide. They are known for their excellent cleaning properties and are widely used in household and industrial cleaning products. These surfactants are effective in removing oils and greases, making them ideal for use in detergents and degreasers. Fatty Alkanolamides are derived from fatty acids and alkanolamines. They are used as foam stabilizers and viscosity enhancers in various formulations. These surfactants are commonly found in personal care products such as shampoos and body washes, where they help to create a rich lather and improve the texture of the product. Amine Derivatives are produced by the reaction of fatty acids with amines. They are used as emulsifiers and dispersants in a wide range of applications, including agrochemicals, paints, and coatings. These surfactants help to improve the stability and performance of formulations by reducing surface tension and promoting the even distribution of ingredients. Glycerol Derivatives are produced by the reaction of glycerol with fatty acids or other compounds. They are used as emulsifiers, humectants, and solubilizers in various applications. These surfactants are commonly found in personal care products, where they help to improve the moisture content and texture of the product. Other types of low foam nonionic surfactants include block copolymers and alkyl polyglucosides. Block copolymers are produced by the polymerization of ethylene oxide and propylene oxide. They are used as dispersants and emulsifiers in a wide range of applications, including detergents, paints, and coatings. Alkyl polyglucosides are produced by the reaction of fatty alcohols with glucose. They are used as mild surfactants in personal care products and household cleaners, where they provide excellent cleaning performance with low irritation potential. The versatility and effectiveness of these surfactants make them an essential component in many industrial and consumer products.

Detergent, Textile, Personal Care, Petrochemical, Paints & Coatings, Other in the Global Low Foam Nonionic Surfactants Market:

The Global Low Foam Nonionic Surfactants Market finds extensive usage across various industries, including detergents, textiles, personal care, petrochemicals, and paints & coatings. In the detergent industry, these surfactants are highly valued for their ability to provide effective cleaning with minimal foam production. This is particularly important in automatic dishwashing and laundry applications, where excessive foam can interfere with the cleaning process and damage equipment. Low foam nonionic surfactants help to ensure that detergents perform efficiently, even in high-efficiency washing machines that use less water. In the textile industry, these surfactants are used in various stages of textile processing, including scouring, bleaching, dyeing, and finishing. They help to remove impurities, improve wetting and penetration of dyes, and enhance the overall quality of the finished fabric. The low foam properties of these surfactants are particularly beneficial in continuous processing operations, where excessive foam can cause defects and reduce productivity. In the personal care industry, low foam nonionic surfactants are used in a wide range of products, including shampoos, body washes, facial cleansers, and lotions. They provide gentle yet effective cleansing, making them suitable for use in products designed for sensitive skin. These surfactants also help to improve the texture and stability of personal care formulations, ensuring that products remain effective and pleasant to use over time. In the petrochemical industry, low foam nonionic surfactants are used as emulsifiers, dispersants, and wetting agents in various applications, including oilfield chemicals, lubricants, and fuel additives. They help to improve the performance and stability of formulations, ensuring that products meet the demanding requirements of the industry. In the paints & coatings industry, these surfactants are used to improve the dispersion of pigments and other ingredients, ensuring that coatings provide uniform coverage and consistent color. The low foam properties of these surfactants help to prevent defects such as pinholes and craters, resulting in a smooth and durable finish. Other applications of low foam nonionic surfactants include agrochemicals, where they are used to improve the effectiveness of pesticides and herbicides, and industrial cleaning, where they provide efficient cleaning with minimal foam production. The versatility and effectiveness of these surfactants make them an essential component in many industrial and consumer products.

Global Low Foam Nonionic Surfactants Market Outlook:

The global Low Foam Nonionic Surfactants market was valued at US$ 2789 million in 2023 and is anticipated to reach US$ 3554.6 million by 2030, witnessing a CAGR of 3.6% during the forecast period from 2024 to 2030. This market growth is driven by the increasing demand for high-performance cleaning and emulsifying agents across various industries. The versatility and effectiveness of low foam nonionic surfactants make them an essential component in many industrial and consumer products. As industries continue to seek more efficient and environmentally friendly solutions, the demand for these surfactants is expected to grow. The market is also driven by the growing awareness of the environmental impact of surfactants, with low foam nonionic surfactants being favored for their biodegradability and lower toxicity compared to other types of surfactants. This makes them a preferred choice in applications where environmental impact is a concern. The market outlook for low foam nonionic surfactants is positive, with steady growth expected over the forecast period.

| Report Metric | Details |

| Report Name | Low Foam Nonionic Surfactants Market |

| Accounted market size in 2023 | US$ 2789 million |

| Forecasted market size in 2030 | US$ 3554.6 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Stepan, Nouryon, Arkema, BASF, Clariant, Dow, Elementis, Evonik, Huntsman, Kao Corporation, Nippon Shokubai, Jiangsu SECCO Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |