What is Global Semiconductor Spare Parts Market?

The Global Semiconductor Spare Parts Market is a crucial segment within the semiconductor industry, providing essential components required for the maintenance and operation of semiconductor manufacturing equipment. These spare parts are indispensable for ensuring the smooth functioning and longevity of semiconductor fabrication plants, which produce the integrated circuits and microchips used in a wide array of electronic devices. The market encompasses a diverse range of parts, including mechanical components, gas and liquid systems, mechatronics, electrical instruments, and optical parts. The demand for semiconductor spare parts is driven by the continuous advancements in semiconductor technology, the increasing complexity of semiconductor devices, and the need for high precision and reliability in manufacturing processes. As semiconductor manufacturers strive to enhance production efficiency and reduce downtime, the importance of having a reliable supply of high-quality spare parts becomes paramount. This market is characterized by a high degree of specialization, with suppliers often providing custom-designed parts tailored to the specific needs of semiconductor fabrication equipment. The global reach of the semiconductor industry means that the spare parts market is also international, with key players and suppliers operating across various regions to meet the demands of semiconductor manufacturers worldwide.

Mechanical Parts (Metal Parts, Chamber, Showerhead, etc.), Gas/Liquid/Vacuum System (Pump, Valves, etc.), Mechatronics (Robot, EFEM, etc.), Electrical (RF Generator), Instruments (MFC, Vacuum Gauge), Optical Parts, Others in the Global Semiconductor Spare Parts Market:

Mechanical parts in the Global Semiconductor Spare Parts Market include metal parts, chambers, and showerheads, which are essential for the structural integrity and functionality of semiconductor manufacturing equipment. Metal parts are often custom-fabricated to meet specific design requirements and are used in various components of the equipment. Chambers are critical for maintaining controlled environments during semiconductor processing, ensuring that the conditions are optimal for the precise fabrication of semiconductor devices. Showerheads are used in chemical vapor deposition (CVD) processes to evenly distribute gases over the wafer surface. The gas, liquid, and vacuum systems encompass pumps and valves that are vital for controlling the flow of gases and liquids, as well as maintaining vacuum conditions necessary for certain semiconductor processes. Pumps are used to move fluids and gases through the system, while valves regulate the flow and pressure. Mechatronics, including robots and equipment front-end modules (EFEM), play a crucial role in automating the handling and processing of wafers, enhancing efficiency and reducing the risk of contamination. Robots are used for precise and repeatable movements, while EFEMs serve as interfaces between the wafer handling system and the processing equipment. Electrical components such as RF generators are used to provide the necessary power for plasma generation in processes like etching and deposition. Instruments like mass flow controllers (MFCs) and vacuum gauges are essential for monitoring and controlling the flow of gases and maintaining the required vacuum levels. Optical parts are used in lithography and inspection equipment, where precision optics are necessary for the accurate patterning and examination of semiconductor wafers. Other components in the market include various specialized parts that cater to specific needs within the semiconductor manufacturing process. Each of these components plays a vital role in ensuring the efficiency, precision, and reliability of semiconductor fabrication, making the Global Semiconductor Spare Parts Market an integral part of the semiconductor industry.

Etch Equipment, Lithography Machines, Track, Deposition, Cleaning Equipment, CMP, Heat Treatment Equipment, Ion Implant, Metrology and Inspection, Others in the Global Semiconductor Spare Parts Market:

The usage of Global Semiconductor Spare Parts Market spans across various types of semiconductor manufacturing equipment, each with its unique requirements and challenges. Etch equipment, for instance, relies heavily on spare parts such as RF generators, vacuum pumps, and showerheads to create precise patterns on the semiconductor wafers by removing material through chemical or physical means. Lithography machines, which are used to transfer circuit patterns onto wafers, require high-precision optical parts, as well as mechanical components like stages and alignment systems to ensure accurate patterning. Track equipment, which handles the coating and development of photoresist on wafers, depends on pumps, valves, and mechatronic systems for precise chemical delivery and wafer handling. Deposition equipment, used for adding material layers onto wafers, utilizes components like chambers, gas delivery systems, and RF generators to achieve uniform and controlled deposition. Cleaning equipment, essential for removing contaminants from wafers, relies on a variety of pumps, valves, and chemical delivery systems to ensure thorough and efficient cleaning processes. Chemical Mechanical Planarization (CMP) equipment, which smooths and planarizes wafer surfaces, uses mechanical parts, slurry delivery systems, and polishing pads to achieve the desired surface finish. Heat treatment equipment, used for processes like annealing and diffusion, requires precise temperature control systems, including heaters, thermocouples, and gas delivery systems. Ion implant equipment, which introduces dopants into the wafer, relies on high-voltage power supplies, vacuum systems, and beamline components to achieve accurate implantation. Metrology and inspection equipment, used for measuring and inspecting wafers, depend on high-precision optical parts, sensors, and alignment systems to ensure accurate measurements and defect detection. Other types of equipment in the semiconductor manufacturing process also require a variety of spare parts to maintain optimal performance and reliability. Each piece of equipment has specific requirements for spare parts, and the availability of high-quality, reliable components is crucial for minimizing downtime and ensuring the efficiency and precision of semiconductor manufacturing processes.

Global Semiconductor Spare Parts Market Outlook:

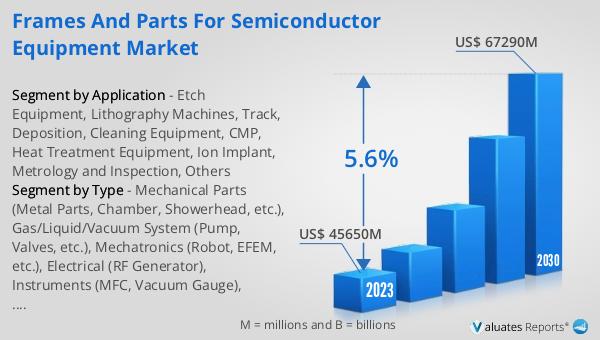

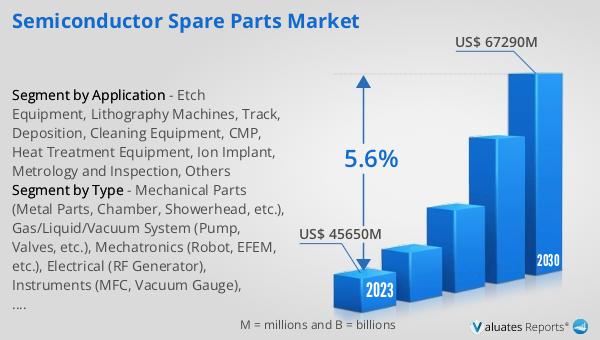

The global Semiconductor Spare Parts market was valued at US$ 45,650 million in 2023 and is anticipated to reach US$ 67,290 million by 2030, witnessing a CAGR of 5.6% during the forecast period from 2024 to 2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased by 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings. This growth reflects the ongoing demand for semiconductor devices across various industries, including consumer electronics, automotive, and telecommunications. The increasing complexity of semiconductor manufacturing processes and the need for high precision and reliability in production are driving the demand for high-quality spare parts. As semiconductor manufacturers continue to invest in advanced manufacturing technologies and equipment, the importance of having a reliable supply of spare parts becomes even more critical. The global reach of the semiconductor industry means that the spare parts market is also international, with key players and suppliers operating across various regions to meet the demands of semiconductor manufacturers worldwide.

| Report Metric | Details |

| Report Name | Semiconductor Spare Parts Market |

| Accounted market size in 2023 | US$ 45650 million |

| Forecasted market size in 2030 | US$ 67290 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | ZEISS, MKS, Edwards, NGK Insulators, Applied Materials, Advanced Energy, Lam Research, Horiba, VAT, Entegris, Ichor Systems, Ultra Clean Tech, Pall, ASML, Ebara, Camfil, Coorstek, Atlas Atlas Copco, TOTO Advanced Ceramics, Parker, CKD, SHINKO, Shimadzu, Shin-Etsu Polymer, Kyocera, Ferrotec, MiCo Ceramics Co., Ltd., Fujikin, TOTO, Schunk Xycarb Technology, KITZ SCT, Swagelok, Sevenstar, Nippon Seisen, GEMU, SMC, XP Power, IHARA, YESIANG Enterprise, Trumpf, Exyte Technology, Comet Plasma Control Technol, Ecopro, Chuang King Enterprise, Brooks Instrument, Kyosan Electric Manufacturing, Rotarex, AAF International, Donaldson Company, Purafil, Asahi-Yukizai, ASUZAC Fine Ceramics, Mott Corporation, Gudeng Precision, Sumitomo Osaka Cement, Presys, Porvair, MKP, Azbil, Kofloc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |