What is Global Chamber Liner for Semiconductor Etching Equipment Market?

The Global Chamber Liner for Semiconductor Etching Equipment Market is a specialized segment within the semiconductor manufacturing industry. Chamber liners are critical components used in etching equipment, which is essential for the production of semiconductor devices. These liners serve as protective barriers within the etching chambers, preventing damage to the chamber walls from the harsh chemicals and plasma used in the etching process. The market for these chamber liners is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and industrial sectors. As semiconductor technology advances, the need for more precise and efficient etching processes grows, further fueling the demand for high-quality chamber liners. The market encompasses various types of liners, including ceramic and metal variants, each offering distinct advantages in terms of durability, thermal stability, and chemical resistance. The global market for chamber liners is characterized by continuous innovation and development to meet the evolving needs of the semiconductor industry.

Ceramic Chamber Liner, Metal Chamber Liner (aluminium alloy) in the Global Chamber Liner for Semiconductor Etching Equipment Market:

Ceramic Chamber Liners and Metal Chamber Liners, particularly those made from aluminum alloy, are two primary types of chamber liners used in the semiconductor etching equipment market. Ceramic chamber liners are known for their excellent thermal stability and chemical resistance, making them ideal for high-temperature and corrosive environments. These liners are typically made from materials such as alumina or silicon carbide, which can withstand the harsh conditions of the etching process without degrading. The use of ceramic liners helps in maintaining the integrity of the etching chamber, ensuring consistent performance and longevity of the equipment. On the other hand, metal chamber liners, especially those made from aluminum alloy, offer a different set of advantages. Aluminum alloy liners are valued for their lightweight properties and good thermal conductivity, which can help in dissipating heat more effectively during the etching process. This can be particularly beneficial in applications where precise temperature control is crucial. Additionally, aluminum alloy liners can be engineered to provide a good balance between durability and cost-effectiveness, making them a popular choice in various semiconductor manufacturing settings. Both types of liners play a crucial role in protecting the etching equipment and ensuring the quality of the semiconductor devices produced. The choice between ceramic and metal liners often depends on the specific requirements of the etching process, including the types of chemicals used, the operating temperatures, and the desired lifespan of the equipment. As the semiconductor industry continues to evolve, the demand for advanced chamber liners that can meet the increasingly stringent requirements of modern etching processes is expected to grow. Manufacturers are continually exploring new materials and technologies to enhance the performance and durability of these liners, ensuring they can keep pace with the rapid advancements in semiconductor technology.

12 inch Etching Equipment, 8 inch Etching Equipment in the Global Chamber Liner for Semiconductor Etching Equipment Market:

The usage of Global Chamber Liners for Semiconductor Etching Equipment is critical in both 12-inch and 8-inch etching equipment, which are commonly used in semiconductor manufacturing. In 12-inch etching equipment, which is used for processing larger semiconductor wafers, the demand for high-performance chamber liners is particularly high. These larger wafers require more precise and uniform etching processes to ensure the quality and yield of the semiconductor devices. Ceramic chamber liners are often preferred in 12-inch equipment due to their superior thermal stability and resistance to chemical corrosion. These properties help in maintaining a stable etching environment, which is crucial for achieving the high precision required in processing larger wafers. Additionally, the use of ceramic liners can help in reducing particle contamination, which is a significant concern in semiconductor manufacturing. On the other hand, 8-inch etching equipment, which is used for processing smaller wafers, also benefits from the use of high-quality chamber liners. While the requirements for thermal stability and chemical resistance may not be as stringent as in 12-inch equipment, the need for durability and cost-effectiveness remains critical. Metal chamber liners, particularly those made from aluminum alloy, are often used in 8-inch equipment due to their good balance of performance and cost. These liners provide adequate protection for the etching chamber while offering the benefits of lightweight and good thermal conductivity. The choice of chamber liner material in both 12-inch and 8-inch etching equipment is influenced by various factors, including the specific etching process, the types of chemicals used, and the desired lifespan of the equipment. As semiconductor technology continues to advance, the need for more efficient and reliable etching processes will drive the demand for high-performance chamber liners in both types of equipment. Manufacturers are continually innovating to develop new materials and designs that can meet the evolving needs of the semiconductor industry, ensuring that both 12-inch and 8-inch etching equipment can deliver the precision and reliability required for modern semiconductor manufacturing.

Global Chamber Liner for Semiconductor Etching Equipment Market Outlook:

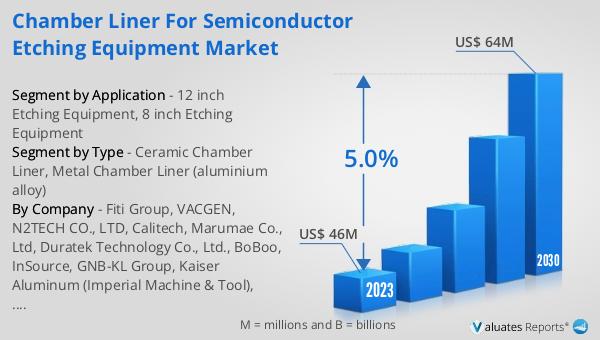

The global Chamber Liner for Semiconductor Etching Equipment market was valued at US$ 46 million in 2023 and is anticipated to reach US$ 64 million by 2030, witnessing a CAGR of 5.0% during the forecast period 2024-2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings.

| Report Metric | Details |

| Report Name | Chamber Liner for Semiconductor Etching Equipment Market |

| Accounted market size in 2023 | US$ 46 million |

| Forecasted market size in 2030 | US$ 64 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Fiti Group, VACGEN, N2TECH CO., LTD, Calitech, Marumae Co., Ltd, Duratek Technology Co., Ltd., BoBoo, InSource, GNB-KL Group, Kaiser Aluminum (Imperial Machine & Tool), LACO Technologies, Sprint Precision Technologies Co., Ltd, KFMI, Shenyang Fortune Precision Equipment Co., Ltd, Tolerance Technology (Shanghai), Sanyue Semiconductor Technology, Cast Aluminum Solutions (CAS), Hansol IONES, SK enpulse, Mitsubishi Chemical (Cleanpart), Htc vacuum, Yeedex, ZHENBAOTECH, Nikkoshi Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |