What is Global Coating for Semiconductor Equipment Parts Market?

The global coating for semiconductor equipment parts market is a specialized sector that focuses on providing protective and functional coatings for various components used in semiconductor manufacturing. These coatings are essential for enhancing the performance, durability, and reliability of semiconductor equipment parts, which are subjected to extreme conditions during the manufacturing process. The coatings help in reducing wear and tear, preventing corrosion, and improving thermal and electrical conductivity. This market is driven by the increasing demand for semiconductors in various applications such as consumer electronics, automotive, and industrial sectors. As the semiconductor industry continues to evolve with advancements in technology, the need for high-quality coatings for equipment parts becomes even more critical. Companies in this market are continuously innovating to develop advanced coating solutions that can meet the stringent requirements of semiconductor manufacturing processes.

in the Global Coating for Semiconductor Equipment Parts Market:

The global coating for semiconductor equipment parts market offers a variety of coating types to cater to the diverse needs of customers. One of the most commonly used coatings is the PVD (Physical Vapor Deposition) coating, which is known for its excellent hardness and wear resistance. PVD coatings are widely used in applications where high durability and performance are required. Another popular type is the CVD (Chemical Vapor Deposition) coating, which provides superior chemical resistance and is ideal for environments where parts are exposed to corrosive substances. ALD (Atomic Layer Deposition) coatings are also gaining traction due to their ability to provide ultra-thin and uniform coatings, making them suitable for advanced semiconductor applications. Additionally, there are specialized coatings such as DLC (Diamond-Like Carbon) coatings, which offer exceptional hardness and low friction properties, making them ideal for high-precision applications. Customers in the semiconductor industry choose these coatings based on their specific requirements, such as the need for enhanced durability, chemical resistance, or thermal stability. For instance, manufacturers of etch equipment may opt for PVD coatings to ensure the longevity and performance of their components, while those involved in deposition processes might prefer CVD or ALD coatings for their superior chemical resistance and uniformity. The choice of coating also depends on the type of semiconductor device being manufactured and the specific conditions of the manufacturing process. As the semiconductor industry continues to advance, the demand for specialized coatings that can meet the evolving needs of customers is expected to grow. Companies in this market are investing in research and development to create innovative coating solutions that can address the challenges faced by semiconductor manufacturers.

Semiconductor Etch Equipment, Deposition (CVD, PVD, ALD), Ion Implant Equipment, Others in the Global Coating for Semiconductor Equipment Parts Market:

The usage of global coating for semiconductor equipment parts market is crucial in various areas such as semiconductor etch equipment, deposition (CVD, PVD, ALD), ion implant equipment, and others. In semiconductor etch equipment, coatings play a vital role in protecting the components from the harsh chemical environments and high temperatures involved in the etching process. These coatings help in reducing wear and tear, thereby extending the lifespan of the equipment and ensuring consistent performance. In deposition processes such as CVD, PVD, and ALD, coatings are essential for maintaining the integrity of the equipment parts. CVD coatings, for example, provide excellent chemical resistance, making them ideal for environments where parts are exposed to corrosive substances. PVD coatings, on the other hand, offer superior hardness and wear resistance, which are crucial for high-performance applications. ALD coatings are known for their ultra-thin and uniform properties, making them suitable for advanced semiconductor applications where precision is key. In ion implant equipment, coatings are used to protect the components from the high-energy ions that are implanted into the semiconductor wafers. These coatings help in minimizing damage to the equipment and ensuring accurate implantation of ions. Other areas where coatings are used include cleaning and inspection equipment, where they help in maintaining the cleanliness and functionality of the components. Overall, the usage of coatings in semiconductor equipment parts is essential for enhancing the performance, durability, and reliability of the equipment, thereby ensuring the efficient and cost-effective production of semiconductor devices.

Global Coating for Semiconductor Equipment Parts Market Outlook:

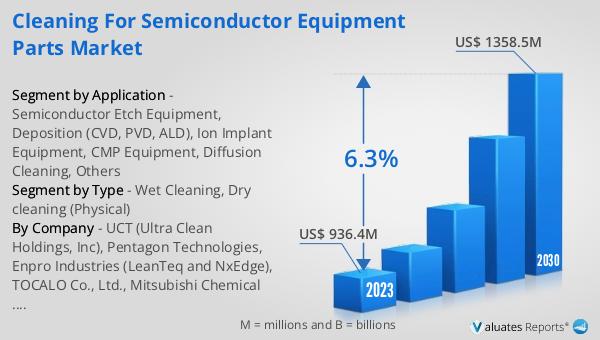

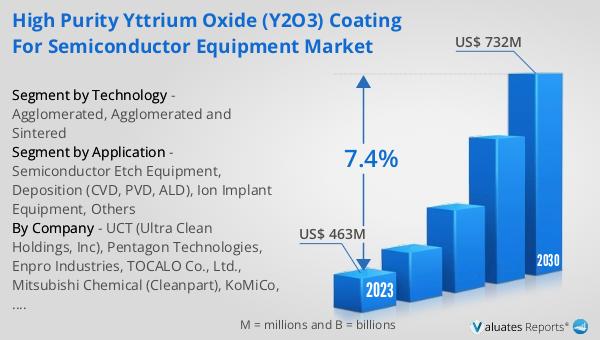

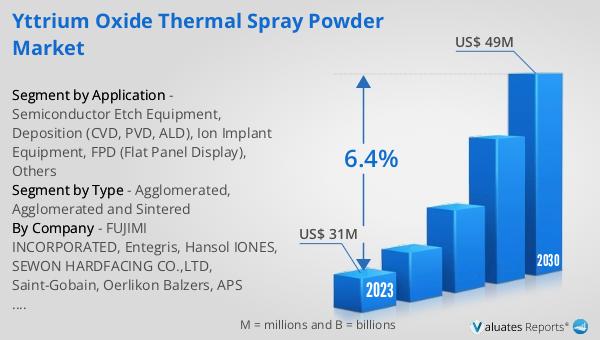

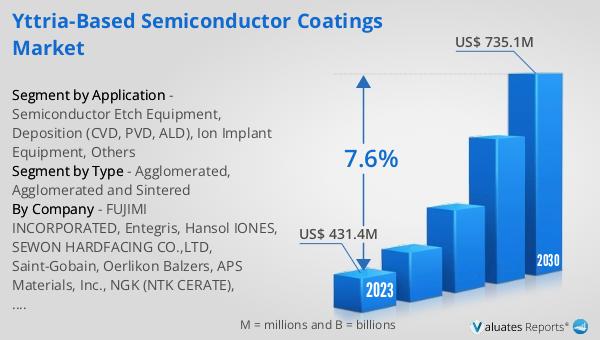

The global coating for semiconductor equipment parts market was valued at US$ 766 million in 2023 and is anticipated to reach US$ 1217.1 million by 2030, witnessing a CAGR of 7.0% during the forecast period 2024-2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022 despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings. This growth in the semiconductor equipment market is indicative of the increasing demand for advanced semiconductor devices across various industries. The continuous advancements in technology and the growing need for high-performance electronic devices are driving the demand for semiconductor equipment, which in turn is boosting the market for coatings used in these equipment parts. Companies in this market are focusing on developing innovative coating solutions that can meet the stringent requirements of semiconductor manufacturing processes, thereby ensuring the efficient and reliable production of semiconductor devices.

| Report Metric | Details |

| Report Name | Coating for Semiconductor Equipment Parts Market |

| Accounted market size in 2023 | US$ 766 million |

| Forecasted market size in 2030 | US$ 1217.1 million |

| CAGR | 7.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Coating Material |

|

| Segment by Application |

|

| By Region |

|

| By Company | UCT (Ultra Clean Holdings, Inc), Pentagon Technologies, Enpro Industries, TOCALO Co., Ltd., Mitsubishi Chemical (Cleanpart), KoMiCo, Cinos, Hansol IONES, WONIK QnC, DFtech, TOPWINTECH, FEMVIX, SEWON HARDFACING CO.,LTD, Frontken Corporation Berhad, Value Engineering Co., Ltd, KERTZ HIGH TECH, Hung Jie Technology Corporation, Oerlikon Balzers, Beneq, APS Materials, Inc., SilcoTek, Alumiplate, Alcadyne, ASSET Solutions, Inc., Jiangsu Kaiweitesi Semiconductor Technology Co., Ltd., HCUT Co., Ltd, Ferrotec (Anhui) Technology Development Co., Ltd, Shanghai Companion |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |