What is Global SiC Diodes Market?

The Global SiC Diodes Market refers to the worldwide industry focused on the production, distribution, and utilization of Silicon Carbide (SiC) diodes. SiC diodes are semiconductor devices that offer superior performance compared to traditional silicon-based diodes, particularly in high-temperature and high-voltage applications. These diodes are known for their high efficiency, fast switching capabilities, and robustness, making them ideal for various industrial and commercial applications. The market encompasses a wide range of products, including discrete SiC diodes and SiC diode power modules, which are used in sectors such as automotive, renewable energy, industrial motors, and data centers. The growing demand for energy-efficient and high-performance electronic components is driving the expansion of the Global SiC Diodes Market. As industries continue to seek advanced solutions to enhance their operational efficiency and reduce energy consumption, the adoption of SiC diodes is expected to rise significantly.

SiC Diodes Discrete, SiC Diodes Power Module in the Global SiC Diodes Market:

SiC diodes come in two primary forms: discrete SiC diodes and SiC diode power modules. Discrete SiC diodes are individual semiconductor devices that are used in various electronic circuits to control the flow of current. These diodes are known for their high breakdown voltage, low forward voltage drop, and excellent thermal stability, making them suitable for high-frequency and high-efficiency applications. They are commonly used in power supplies, inverters, and motor drives, where their fast switching capabilities and low power losses contribute to improved system performance and energy savings. On the other hand, SiC diode power modules are integrated solutions that combine multiple SiC diodes and other components into a single package. These modules are designed to handle higher power levels and provide enhanced reliability and thermal management. They are used in more demanding applications such as electric vehicle (EV) powertrains, renewable energy systems, and industrial automation. The integration of SiC diodes into power modules allows for more compact and efficient designs, reducing the overall size and weight of electronic systems. Both discrete SiC diodes and SiC diode power modules play a crucial role in the Global SiC Diodes Market, catering to the diverse needs of various industries and driving the adoption of advanced semiconductor technologies.

Automotive & EV/HEV, EV Charging, Industrial Motor/Drive, PV, Energy Storage, Wind Power, UPS, Data Center & Server, Rail Transport, Others in the Global SiC Diodes Market:

The usage of SiC diodes in the Global SiC Diodes Market spans across multiple sectors, each benefiting from the unique properties of these advanced semiconductor devices. In the automotive and EV/HEV (Electric Vehicle/Hybrid Electric Vehicle) sector, SiC diodes are used in powertrains, inverters, and onboard chargers, enhancing the efficiency and performance of electric vehicles. They enable faster charging times, longer driving ranges, and improved thermal management, contributing to the overall advancement of EV technology. In EV charging infrastructure, SiC diodes are employed in fast chargers and charging stations, providing high efficiency and reliability, which are essential for the widespread adoption of electric vehicles. In the industrial motor/drive sector, SiC diodes are used in motor controllers and drives, offering high-speed switching and reduced power losses, which lead to increased energy efficiency and lower operational costs. In photovoltaic (PV) systems, SiC diodes are utilized in inverters and power optimizers, improving the conversion efficiency of solar energy and enhancing the overall performance of solar power installations. In energy storage systems, SiC diodes are used in battery management systems and power converters, ensuring efficient energy transfer and reliable operation. In wind power applications, SiC diodes are employed in wind turbine converters, providing high efficiency and robustness in harsh environmental conditions. In uninterruptible power supplies (UPS), SiC diodes are used to ensure reliable and efficient power backup, critical for data centers and server farms. In rail transport, SiC diodes are used in traction systems and power converters, offering high efficiency and reliability for modern rail networks. Other applications of SiC diodes include aerospace, telecommunications, and medical devices, where their high performance and reliability are essential. The diverse usage of SiC diodes across these sectors highlights their importance in the Global SiC Diodes Market and their contribution to the advancement of various technologies.

Global SiC Diodes Market Outlook:

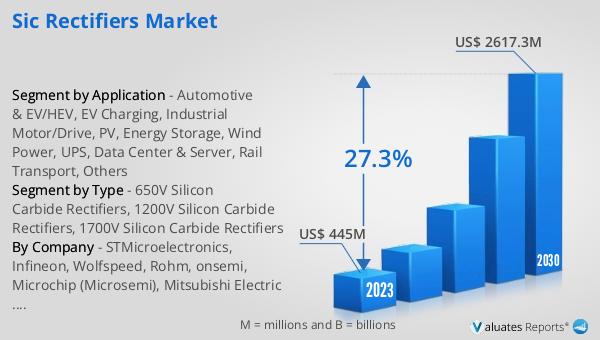

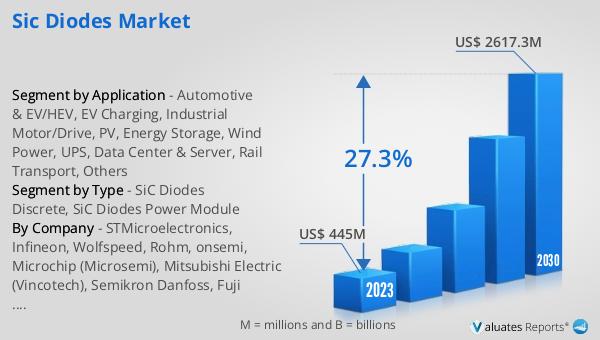

The global SiC Diodes market was valued at US$ 445 million in 2023 and is anticipated to reach US$ 2617.3 million by 2030, witnessing a CAGR of 27.3% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for high-performance and energy-efficient semiconductor devices across various industries. The market is dominated by the top five players, who collectively hold a share of over 70 percent. These leading companies are driving innovation and development in the SiC diodes sector, contributing to the rapid expansion of the market. The growing adoption of SiC diodes in applications such as electric vehicles, renewable energy systems, and industrial automation is fueling this growth. As industries continue to seek advanced solutions to enhance their operational efficiency and reduce energy consumption, the Global SiC Diodes Market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | SiC Diodes Market |

| Accounted market size in 2023 | US$ 445 million |

| Forecasted market size in 2030 | US$ 2617.3 million |

| CAGR | 27.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, Microchip (Microsemi), Mitsubishi Electric (Vincotech), Semikron Danfoss, Fuji Electric, Navitas (GeneSiC), Toshiba, Qorvo (UnitedSiC), San'an Optoelectronics, Littelfuse (IXYS), CETC 55, WeEn Semiconductors, BASiC Semiconductor, SemiQ, KEC Corporation, PANJIT Group, Nexperia, Vishay Intertechnology, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, Yangzhou Yangjie Electronic Technology, Changzhou Galaxy Century Microelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |