What is Global Drafting and 3D Modeling Market?

The global Drafting and 3D Modeling market is a rapidly evolving sector that encompasses the creation of detailed technical drawings and three-dimensional representations of objects. This market includes a wide range of software and services that enable professionals to design, visualize, and simulate products and structures before they are built. The applications of drafting and 3D modeling are vast, spanning industries such as architecture, engineering, construction, manufacturing, automotive, transportation, government, defense, and agriculture. These tools help in improving accuracy, reducing errors, and enhancing the efficiency of the design and production processes. With advancements in technology, the capabilities of drafting and 3D modeling software have expanded, allowing for more complex and detailed designs. The market is driven by the increasing demand for precision and efficiency in various industries, as well as the growing adoption of digital technologies. As a result, the global Drafting and 3D Modeling market is expected to continue its growth trajectory in the coming years.

Software, Services, Others in the Global Drafting and 3D Modeling Market:

The Global Drafting and 3D Modeling Market is segmented into software, services, and others, each playing a crucial role in the overall ecosystem. Software in this market includes a variety of applications designed to create detailed technical drawings and 3D models. These software solutions range from basic drafting tools to advanced 3D modeling applications that offer features like parametric modeling, simulation, and rendering. Popular software in this category includes AutoCAD, SolidWorks, and Revit, which are widely used across different industries for their robust capabilities and user-friendly interfaces. These tools help professionals in creating precise and detailed designs, which are essential for the successful execution of projects. Services in the Global Drafting and 3D Modeling Market encompass a wide range of offerings that support the use and implementation of drafting and 3D modeling software. These services include training, consulting, and technical support, which are essential for ensuring that users can effectively utilize the software to its full potential. Training services help users to understand the functionalities and features of the software, enabling them to create accurate and efficient designs. Consulting services provide expert advice on the best practices and methodologies for using the software, helping organizations to optimize their design processes. Technical support services ensure that any issues or challenges faced by users are promptly addressed, minimizing downtime and enhancing productivity. The "others" category in the Global Drafting and 3D Modeling Market includes hardware and other ancillary products that are essential for the effective use of drafting and 3D modeling software. This includes high-performance computers, graphics cards, and input devices like digital pens and tablets, which are necessary for creating detailed and complex designs. Additionally, this category also includes cloud-based solutions that offer storage and collaboration capabilities, enabling teams to work together seamlessly on design projects. The integration of cloud technology has revolutionized the drafting and 3D modeling market, allowing for real-time collaboration and access to designs from anywhere in the world. Overall, the Global Drafting and 3D Modeling Market is a dynamic and multifaceted sector that is driven by the continuous advancements in technology and the growing demand for precision and efficiency in various industries. The combination of software, services, and other essential products creates a comprehensive ecosystem that supports the creation of detailed and accurate designs, ultimately contributing to the success of projects across different sectors.

Architecture, Engineering and Construction (AEC), Manufacturing, Automotive and Transportation, Government and Defense, Agriculture, Others in the Global Drafting and 3D Modeling Market:

The usage of the Global Drafting and 3D Modeling Market spans across various industries, each benefiting from the precision and efficiency offered by these tools. In the Architecture, Engineering, and Construction (AEC) sector, drafting and 3D modeling software are essential for creating detailed architectural plans, structural designs, and construction blueprints. These tools enable architects and engineers to visualize their designs in three dimensions, identify potential issues, and make necessary adjustments before construction begins. This not only improves the accuracy of the designs but also reduces the risk of errors and rework during the construction phase. In the manufacturing industry, drafting and 3D modeling software are used to design and simulate products before they are produced. This allows manufacturers to test the functionality and performance of their products, identify any design flaws, and make necessary modifications before mass production. This not only improves the quality of the products but also reduces the time and cost associated with the production process. In the automotive and transportation sector, drafting and 3D modeling software are used to design and develop vehicles and transportation systems. These tools enable automotive engineers to create detailed models of vehicles, simulate their performance, and make necessary adjustments to improve their efficiency and safety. This not only enhances the quality of the vehicles but also reduces the time and cost associated with their development. In the government and defense sector, drafting and 3D modeling software are used to design and develop military equipment and infrastructure. These tools enable defense engineers to create detailed models of military vehicles, weapons, and facilities, simulate their performance, and make necessary adjustments to improve their efficiency and effectiveness. This not only enhances the quality of the military equipment and infrastructure but also reduces the time and cost associated with their development. In the agriculture sector, drafting and 3D modeling software are used to design and develop agricultural equipment and infrastructure. These tools enable agricultural engineers to create detailed models of farming equipment, simulate their performance, and make necessary adjustments to improve their efficiency and effectiveness. This not only enhances the quality of the agricultural equipment and infrastructure but also reduces the time and cost associated with their development. Overall, the usage of drafting and 3D modeling software in various industries has revolutionized the way designs are created and executed, leading to improved accuracy, efficiency, and cost-effectiveness.

Global Drafting and 3D Modeling Market Outlook:

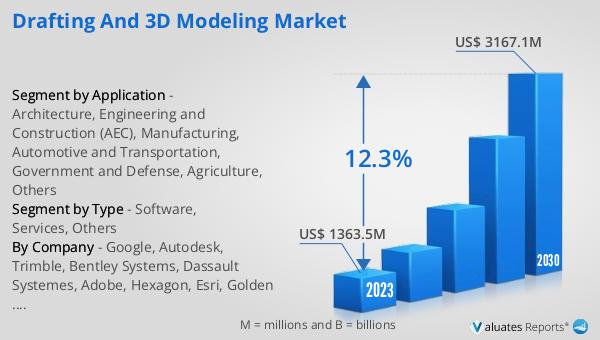

The global Drafting and 3D Modeling market, valued at US$ 1363.5 million in 2023, is projected to grow significantly, reaching an estimated US$ 3167.1 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 12.3% over the forecast period from 2024 to 2030. This substantial increase underscores the rising demand for advanced drafting and 3D modeling solutions across various industries. The market's expansion is driven by the continuous advancements in technology, which have enhanced the capabilities of drafting and 3D modeling software, making them more powerful and user-friendly. Additionally, the growing adoption of digital technologies in industries such as architecture, engineering, construction, manufacturing, automotive, transportation, government, defense, and agriculture has further fueled the demand for these tools. The ability to create precise and detailed designs, visualize and simulate products and structures, and collaborate in real-time has become increasingly important in today's fast-paced and competitive business environment. As a result, organizations are investing in advanced drafting and 3D modeling solutions to improve their design processes, enhance productivity, and reduce costs. The projected growth of the global Drafting and 3D Modeling market reflects the increasing recognition of the value and benefits offered by these tools, and their critical role in driving innovation and efficiency across various sectors.

| Report Metric | Details |

| Report Name | Drafting and 3D Modeling Market |

| Accounted market size in 2023 | US$ 1363.5 million |

| Forecasted market size in 2030 | US$ 3167.1 million |

| CAGR | 12.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Google, Autodesk, Trimble, Bentley Systems, Dassault Systemes, Adobe, Hexagon, Esri, Golden Software, Maxon, Topcon, CyberCity 3D, Pix4D, Apple, Onionlab, Mapbox, Saab AB, Airbus, Intermap Technologies, The Foundry Visionmongers, Mathworks, Blender Foundation, Civil Maps |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |