What is Global Rapid Start Operation Lamp Electrodes Market?

The Global Rapid Start Operation Lamp Electrodes Market refers to the industry focused on the production and distribution of electrodes used in rapid start operation lamps. These lamps are designed to light up quickly and efficiently, making them ideal for various applications. The market encompasses a wide range of electrode types, including preheat electrodes and cathode guard ring electrodes, which are essential components in ensuring the proper functioning and longevity of these lamps. The demand for rapid start operation lamp electrodes is driven by their extensive use in residential, commercial, industrial, outdoor, and automotive lighting solutions. As energy efficiency and quick illumination become increasingly important, the market for these specialized electrodes continues to grow, catering to the needs of diverse sectors worldwide.

Preheat Electrode, Cathode Guard Ring Electrode in the Global Rapid Start Operation Lamp Electrodes Market:

Preheat electrodes and cathode guard ring electrodes are two critical components in the Global Rapid Start Operation Lamp Electrodes Market. Preheat electrodes are designed to warm up the lamp's cathode before the main discharge occurs, ensuring a smooth and efficient start. This preheating process reduces the stress on the lamp, thereby extending its lifespan and improving its overall performance. Preheat electrodes are commonly used in fluorescent lamps, where a rapid and reliable start is essential. On the other hand, cathode guard ring electrodes serve a different purpose. They are designed to protect the cathode from sputtering, a process where material from the cathode is ejected due to the high-energy discharge. This protection is crucial in maintaining the integrity of the lamp and preventing premature failure. Cathode guard ring electrodes are often used in high-intensity discharge (HID) lamps, which require robust components to handle the intense energy levels. Both types of electrodes play a vital role in the rapid start operation of lamps, ensuring that they light up quickly and efficiently while maintaining their durability. The market for these electrodes is driven by the need for reliable and long-lasting lighting solutions across various applications. As technology advances, the design and materials used in these electrodes continue to evolve, offering improved performance and efficiency. The demand for preheat electrodes and cathode guard ring electrodes is expected to grow as industries seek more energy-efficient and durable lighting options. These electrodes are essential in meeting the stringent requirements of modern lighting systems, making them a crucial component in the Global Rapid Start Operation Lamp Electrodes Market.

Residential, Commercial, Industrial, Outdoor, Automotive in the Global Rapid Start Operation Lamp Electrodes Market:

The usage of Global Rapid Start Operation Lamp Electrodes Market spans across various sectors, including residential, commercial, industrial, outdoor, and automotive applications. In residential settings, these electrodes are used in fluorescent lamps and compact fluorescent lamps (CFLs), providing homeowners with energy-efficient and quick-start lighting solutions. The rapid start feature is particularly beneficial in areas where lights are frequently turned on and off, such as kitchens, bathrooms, and hallways. In commercial environments, rapid start operation lamp electrodes are essential in office buildings, retail stores, and hospitality establishments. They ensure that lighting systems are reliable and efficient, reducing energy consumption and maintenance costs. The quick start capability is crucial in creating a comfortable and well-lit environment for employees and customers. In industrial applications, these electrodes are used in high-bay and low-bay lighting systems, providing bright and consistent illumination in warehouses, manufacturing plants, and other industrial facilities. The durability and efficiency of rapid start operation lamps make them ideal for demanding industrial environments. Outdoor lighting is another significant area where these electrodes are utilized. Streetlights, parking lot lights, and landscape lighting all benefit from the quick start and energy efficiency of rapid start operation lamps. These electrodes ensure that outdoor spaces are well-lit and safe, enhancing visibility and security. In the automotive sector, rapid start operation lamp electrodes are used in headlights, taillights, and interior lighting systems. The quick start feature is essential for automotive lighting, ensuring that drivers have immediate and reliable illumination. The energy efficiency of these electrodes also contributes to the overall efficiency of the vehicle's electrical system. Overall, the Global Rapid Start Operation Lamp Electrodes Market plays a crucial role in providing efficient and reliable lighting solutions across various sectors. The demand for these electrodes is driven by the need for quick-start, energy-efficient, and durable lighting systems that meet the diverse requirements of residential, commercial, industrial, outdoor, and automotive applications.

Global Rapid Start Operation Lamp Electrodes Market Outlook:

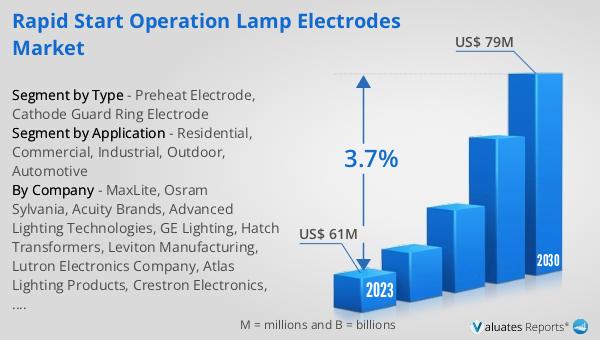

The global Rapid Start Operation Lamp Electrodes market was valued at US$ 61 million in 2023 and is anticipated to reach US$ 79 million by 2030, witnessing a CAGR of 3.7% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing demand for rapid start operation lamp electrodes across various sectors. The projected growth rate indicates a positive trend, driven by the need for energy-efficient and reliable lighting solutions. As industries and consumers continue to prioritize quick-start and durable lighting options, the market for these specialized electrodes is expected to expand. The valuation of US$ 61 million in 2023 reflects the current market size, while the anticipated growth to US$ 79 million by 2030 underscores the potential for further development and innovation in this field. The CAGR of 3.7% signifies a consistent and sustainable growth trajectory, indicating that the market is poised for steady expansion over the forecast period. This growth can be attributed to advancements in technology, increasing awareness of energy efficiency, and the rising demand for high-performance lighting solutions in residential, commercial, industrial, outdoor, and automotive applications. The Global Rapid Start Operation Lamp Electrodes Market is set to experience significant growth, driven by the continuous evolution of lighting technologies and the increasing emphasis on energy conservation and sustainability.

| Report Metric | Details |

| Report Name | Rapid Start Operation Lamp Electrodes Market |

| Accounted market size in 2023 | US$ 61 million |

| Forecasted market size in 2030 | US$ 79 million |

| CAGR | 3.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MaxLite, Osram Sylvania, Acuity Brands, Advanced Lighting Technologies, GE Lighting, Hatch Transformers, Leviton Manufacturing, Lutron Electronics Company, Atlas Lighting Products, Crestron Electronics, Eaton |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |