What is Global Ultra-Short Baseline Acoustic Positioning System Market?

The Global Ultra-Short Baseline (USBL) Acoustic Positioning System Market refers to the industry focused on the development, production, and application of USBL systems. These systems are used for underwater positioning and navigation, providing precise location data for various underwater operations. USBL systems work by emitting acoustic signals from a transceiver, which are then received by a series of hydrophones. The time it takes for the signals to travel between the transceiver and hydrophones is used to calculate the position of the underwater object. This technology is crucial for activities such as underwater surveying, marine research, and subsea construction. The market for USBL systems is driven by the increasing demand for accurate underwater positioning in various sectors, including oil and gas, marine civil engineering, and defense. As underwater operations become more complex and widespread, the need for reliable and precise positioning systems continues to grow, making the USBL market an essential component of the broader marine technology industry.

Shallow Water, Deep Water in the Global Ultra-Short Baseline Acoustic Positioning System Market:

In the context of the Global Ultra-Short Baseline Acoustic Positioning System Market, shallow water and deep water applications are critical areas of focus. Shallow water environments, typically defined as water depths less than 200 meters, present unique challenges for USBL systems. These environments often have higher levels of acoustic noise and signal reflection due to the proximity of the seabed and surface. Despite these challenges, USBL systems are highly effective in shallow water for tasks such as underwater construction, pipeline installation, and environmental monitoring. The ability to provide precise positioning in these conditions is essential for ensuring the accuracy and safety of operations. On the other hand, deep water applications, which involve depths greater than 200 meters, require USBL systems to operate over longer distances and often in more challenging conditions. Deep water environments are characterized by lower temperatures, higher pressures, and reduced light, making reliable positioning systems even more critical. USBL systems used in deep water must be robust and capable of maintaining signal integrity over long distances. These systems are vital for deep-sea exploration, oil and gas extraction, and scientific research. The ability to accurately position equipment and vehicles in deep water is crucial for the success of these operations. Both shallow and deep water applications of USBL systems highlight the versatility and importance of this technology in the marine industry. As the demand for underwater operations continues to grow, the need for reliable and precise positioning systems in both shallow and deep water environments will remain a key driver of the USBL market.

Oil and Gas, Renewables, Marine civil engineering, Defense, Others in the Global Ultra-Short Baseline Acoustic Positioning System Market:

The Global Ultra-Short Baseline Acoustic Positioning System Market finds extensive usage across various sectors, including oil and gas, renewables, marine civil engineering, defense, and others. In the oil and gas industry, USBL systems are essential for subsea operations such as drilling, pipeline installation, and maintenance. Accurate positioning is crucial for these activities to ensure the safety and efficiency of operations. USBL systems help in precisely locating underwater equipment and monitoring their movements, which is vital for avoiding collisions and ensuring proper alignment. In the renewables sector, particularly in offshore wind farms, USBL systems are used for the installation and maintenance of underwater structures. These systems provide accurate positioning data that is essential for the correct placement of turbines and other infrastructure. In marine civil engineering, USBL systems are used for underwater construction projects such as bridge foundations, tunnels, and harbors. The ability to provide precise positioning data ensures that these structures are built accurately and safely. In the defense sector, USBL systems are used for various applications, including submarine navigation, mine detection, and underwater surveillance. The ability to accurately position and track underwater vehicles and equipment is crucial for defense operations. Other sectors that utilize USBL systems include marine research and environmental monitoring. In these fields, USBL systems are used to track underwater vehicles, monitor marine life, and conduct surveys of the seabed. The versatility and reliability of USBL systems make them an indispensable tool for a wide range of underwater applications.

Global Ultra-Short Baseline Acoustic Positioning System Market Outlook:

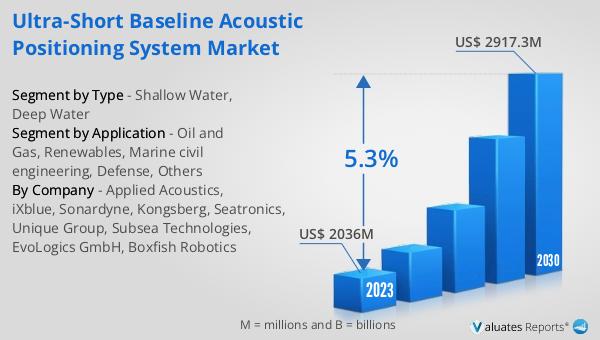

The global Ultra-Short Baseline Acoustic Positioning System market was valued at US$ 2036 million in 2023 and is anticipated to reach US$ 2917.3 million by 2030, witnessing a CAGR of 5.3% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for precise underwater positioning systems across various industries. The market's expansion is driven by the need for accurate and reliable positioning data in complex underwater environments. As underwater operations become more prevalent and sophisticated, the importance of USBL systems continues to rise. These systems are essential for ensuring the safety, efficiency, and success of underwater activities. The projected growth of the USBL market highlights the ongoing advancements in marine technology and the increasing reliance on precise positioning systems for a wide range of applications. The market outlook indicates a positive trend, with significant opportunities for growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Ultra-Short Baseline Acoustic Positioning System Market |

| Accounted market size in 2023 | US$ 2036 million |

| Forecasted market size in 2030 | US$ 2917.3 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Applied Acoustics, iXblue, Sonardyne, Kongsberg, Seatronics, Unique Group, Subsea Technologies, EvoLogics GmbH, Boxfish Robotics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |