What is Global CIGS Photovoltaic Device Market?

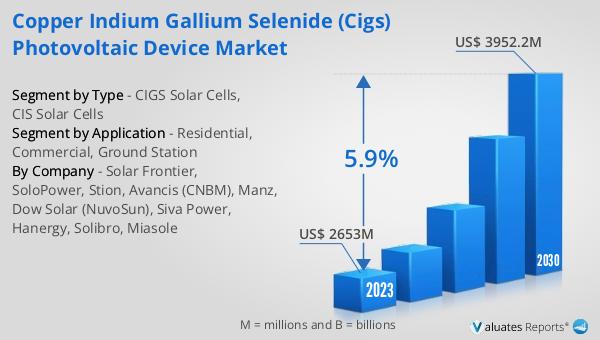

The global CIGS Photovoltaic Device market is a rapidly evolving sector within the renewable energy industry. CIGS stands for Copper Indium Gallium Selenide, a semiconductor material used in the production of thin-film solar cells. These devices are known for their high efficiency and flexibility, making them suitable for a variety of applications. The market for CIGS photovoltaic devices was valued at US$ 2653 million in 2023 and is projected to reach US$ 3952.2 million by 2030, growing at a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2030. This growth is driven by increasing demand for renewable energy sources, advancements in CIGS technology, and supportive government policies aimed at reducing carbon emissions. The versatility of CIGS photovoltaic devices allows them to be used in residential, commercial, and ground station applications, contributing to their widespread adoption. As the world continues to shift towards sustainable energy solutions, the CIGS photovoltaic device market is expected to play a significant role in meeting global energy needs.

CIGS Solar Cells, CIS Solar Cells in the Global CIGS Photovoltaic Device Market:

CIGS solar cells are a type of thin-film solar cell that uses a combination of copper, indium, gallium, and selenium as the semiconductor material. These cells are known for their high efficiency and ability to perform well in low-light conditions, making them an attractive option for various solar energy applications. The manufacturing process of CIGS solar cells involves depositing the semiconductor material onto a substrate, which can be made of glass, plastic, or metal. This flexibility in substrate choice allows for the production of lightweight and flexible solar panels, which can be integrated into a wide range of products, including building materials and portable devices. CIS solar cells, on the other hand, use a similar semiconductor material but without the addition of gallium. While CIS cells are generally less efficient than CIGS cells, they are still a viable option for certain applications due to their lower production costs. Both CIGS and CIS solar cells are part of the broader thin-film solar cell market, which offers several advantages over traditional silicon-based solar cells, including lower material costs, lighter weight, and the ability to be manufactured using roll-to-roll processes. These advantages make CIGS and CIS solar cells an important part of the global photovoltaic device market, as they provide a cost-effective and versatile solution for harnessing solar energy.

Residential, Commercial, Ground Station in the Global CIGS Photovoltaic Device Market:

The usage of CIGS photovoltaic devices spans across various sectors, including residential, commercial, and ground station applications. In residential settings, CIGS solar panels are used to generate electricity for homes, reducing reliance on traditional energy sources and lowering utility bills. The flexibility and lightweight nature of CIGS panels make them easy to install on rooftops and other structures, providing homeowners with a sustainable and efficient energy solution. In commercial applications, CIGS photovoltaic devices are used to power office buildings, factories, and other commercial properties. The high efficiency and durability of CIGS panels make them an ideal choice for large-scale installations, helping businesses reduce their carbon footprint and energy costs. Ground station applications involve the use of CIGS solar panels in large solar farms and power plants. These installations are designed to generate significant amounts of electricity, which can be fed into the grid to supply power to entire communities. The scalability and efficiency of CIGS photovoltaic devices make them well-suited for these large-scale projects, contributing to the overall growth of the renewable energy sector. As the demand for clean energy continues to rise, the versatility and efficiency of CIGS photovoltaic devices will play a crucial role in meeting the energy needs of various sectors.

Global CIGS Photovoltaic Device Market Outlook:

The global CIGS Photovoltaic Device market was valued at US$ 2653 million in 2023 and is anticipated to reach US$ 3952.2 million by 2030, witnessing a CAGR of 5.9% during the forecast period from 2024 to 2030. This market growth is driven by several factors, including the increasing demand for renewable energy sources, advancements in CIGS technology, and supportive government policies aimed at reducing carbon emissions. The versatility of CIGS photovoltaic devices allows them to be used in residential, commercial, and ground station applications, contributing to their widespread adoption. As the world continues to shift towards sustainable energy solutions, the CIGS photovoltaic device market is expected to play a significant role in meeting global energy needs. The high efficiency and flexibility of CIGS solar cells make them an attractive option for various solar energy applications, further driving market growth. Additionally, the lower production costs and scalability of CIGS photovoltaic devices make them a cost-effective solution for harnessing solar energy, which is essential for the continued expansion of the renewable energy sector.

| Report Metric | Details |

| Report Name | CIGS Photovoltaic Device Market |

| Accounted market size in 2023 | US$ 2653 million |

| Forecasted market size in 2030 | US$ 3952.2 million |

| CAGR | 5.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Solar Frontier, SoloPower, Stion, Avancis (CNBM), Manz, Dow Solar (NuvoSun), Siva Power, Hanergy, Solibro, Miasole |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |