What is Global Mono-oriented Polypropylene (MOPP) Packaging Film Market?

The Global Mono-oriented Polypropylene (MOPP) Packaging Film Market refers to the worldwide industry focused on the production and distribution of MOPP films. These films are a type of polypropylene film that is stretched in one direction, which enhances their strength and clarity. MOPP films are widely used in various packaging applications due to their excellent mechanical properties, such as high tensile strength, good barrier properties, and resistance to moisture and chemicals. They are commonly used in industries like food and beverage, pharmaceuticals, and cosmetics, where packaging integrity and product protection are crucial. The market for MOPP packaging films is driven by the increasing demand for flexible and durable packaging solutions, as well as the growing awareness of the benefits of using polypropylene materials in packaging. The global market is characterized by a diverse range of products, catering to different thickness requirements and application needs.

Thickness Below 50 µm, Thickness Between 51 to 100 µm, Thickness Above 100 µm in the Global Mono-oriented Polypropylene (MOPP) Packaging Film Market:

In the Global Mono-oriented Polypropylene (MOPP) Packaging Film Market, the thickness of the films plays a significant role in determining their suitability for various applications. Films with a thickness below 50 µm are typically used for lightweight packaging needs. These thinner films are ideal for applications where flexibility and cost-effectiveness are prioritized. They are commonly used in the packaging of snacks, confectionery, and other lightweight food products. The thinness of these films allows for easy wrapping and sealing, ensuring that the products remain fresh and protected. On the other hand, films with a thickness between 51 to 100 µm offer a balance between strength and flexibility. These medium-thickness films are suitable for a wider range of packaging applications, including the packaging of heavier food items, pharmaceuticals, and cosmetics. They provide better protection against external factors such as moisture and oxygen, which can compromise the quality of the packaged products. Additionally, these films are often used in the labeling and printing industry due to their excellent printability and durability. Films with a thickness above 100 µm are the thickest and most robust in the MOPP film category. These heavy-duty films are designed for applications that require maximum strength and protection. They are commonly used in industrial packaging, where the packaged items need to withstand rough handling and transportation. The high tensile strength of these films ensures that the packaging remains intact, preventing any damage to the contents. Moreover, these thick films are also used in the agricultural sector for packaging seeds, fertilizers, and other agricultural products. The durability and resistance to environmental factors make them ideal for such demanding applications. Overall, the varying thicknesses of MOPP films cater to different packaging needs, ensuring that there is a suitable solution for every application.

Pharmaceuticals, Food and Beverage, Cosmetic Industry, Others in the Global Mono-oriented Polypropylene (MOPP) Packaging Film Market:

The usage of Global Mono-oriented Polypropylene (MOPP) Packaging Film Market spans across various industries, including pharmaceuticals, food and beverage, cosmetics, and others. In the pharmaceutical industry, MOPP films are used for packaging medicines, medical devices, and other healthcare products. The films provide excellent barrier properties, protecting the contents from moisture, oxygen, and other contaminants. This ensures the efficacy and safety of the pharmaceutical products throughout their shelf life. Additionally, the films are used in blister packaging, where they offer a secure and tamper-evident solution for individual doses of medication. In the food and beverage industry, MOPP films are widely used for packaging a variety of products, including snacks, confectionery, dairy products, and beverages. The films help in preserving the freshness and quality of the food items by providing a barrier against moisture, oxygen, and other external factors. They are also used in the packaging of ready-to-eat meals and frozen foods, where the films' durability and flexibility ensure that the packaging remains intact during storage and transportation. In the cosmetic industry, MOPP films are used for packaging beauty and personal care products, such as creams, lotions, and shampoos. The films' excellent printability allows for attractive and high-quality packaging designs, enhancing the visual appeal of the products. Moreover, the films provide protection against moisture and UV light, ensuring that the cosmetic products maintain their quality and effectiveness. Other industries that utilize MOPP films include the agricultural sector, where the films are used for packaging seeds, fertilizers, and other agricultural products. The films' durability and resistance to environmental factors make them ideal for such demanding applications. Additionally, MOPP films are used in the electronics industry for packaging electronic components and devices, providing protection against static electricity and physical damage. Overall, the versatility and excellent properties of MOPP films make them a preferred choice for packaging in various industries.

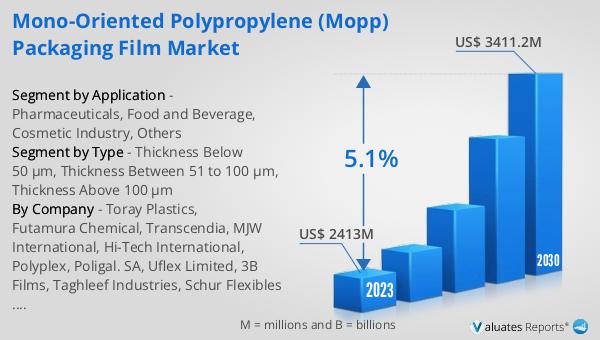

Global Mono-oriented Polypropylene (MOPP) Packaging Film Market Outlook:

The global Mono-oriented Polypropylene (MOPP) Packaging Film market was valued at US$ 2413 million in 2023 and is anticipated to reach US$ 3411.2 million by 2030, witnessing a CAGR of 5.1% during the forecast period 2024-2030. This growth can be attributed to the increasing demand for flexible and durable packaging solutions across various industries. The excellent mechanical properties of MOPP films, such as high tensile strength, good barrier properties, and resistance to moisture and chemicals, make them an ideal choice for packaging applications. The market is characterized by a diverse range of products, catering to different thickness requirements and application needs. The growing awareness of the benefits of using polypropylene materials in packaging is also driving the market growth. Additionally, the rising demand for packaged food and beverages, pharmaceuticals, and cosmetics is further fueling the demand for MOPP films. The market is expected to witness significant growth in the coming years, driven by the increasing adoption of MOPP films in various industries and the continuous advancements in film manufacturing technologies.

| Report Metric | Details |

| Report Name | Mono-oriented Polypropylene (MOPP) Packaging Film Market |

| Accounted market size in 2023 | US$ 2413 million |

| Forecasted market size in 2030 | US$ 3411.2 million |

| CAGR | 5.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Toray Plastics, Futamura Chemical, Transcendia, MJW International, Hi-Tech International, Polyplex, Poligal. SA, Uflex Limited, 3B Films, Taghleef Industries, Schur Flexibles Holding GesmbH, Oben Holding Group S.A.C., Thai Film Industries Public Company, PT. Bhineka Tatamulya, Jindal Poly Films, Profol GmbH, PT Panverta Cakrakencana, M Stretch S.p.A, Mitsui Chemicals, Polibak Plastik, Copol International, TriPack Films, LC Packaging |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |