What is Global Automotive Ethernet Switch Chips Market?

The Global Automotive Ethernet Switch Chips Market refers to the industry focused on the production and distribution of Ethernet switch chips specifically designed for automotive applications. These chips are integral components in modern vehicles, enabling high-speed data communication between various electronic systems within the car. As vehicles become more advanced with features like autonomous driving, advanced driver-assistance systems (ADAS), and infotainment systems, the demand for reliable and efficient data communication networks has surged. Ethernet switch chips facilitate this by providing a robust and scalable solution for managing data traffic. They ensure that different systems within the vehicle can communicate seamlessly, enhancing overall vehicle performance and safety. The market for these chips is growing rapidly as automakers and suppliers recognize the need for advanced networking solutions to support the increasing complexity of automotive electronics.

Automotive Local Area Network (LAN), Automotive Metropolitan Area Network (MAN) in the Global Automotive Ethernet Switch Chips Market:

Automotive Local Area Network (LAN) and Automotive Metropolitan Area Network (MAN) are two critical components within the Global Automotive Ethernet Switch Chips Market. Automotive LAN refers to the network within a vehicle that connects various electronic control units (ECUs), sensors, and actuators. This network is essential for the real-time communication required for functions such as engine control, transmission control, and safety systems like airbags and anti-lock braking systems (ABS). Ethernet switch chips play a pivotal role in automotive LANs by ensuring that data packets are efficiently routed between different components, minimizing latency and maximizing reliability. On the other hand, Automotive MAN extends the concept of networking beyond a single vehicle to connect multiple vehicles and infrastructure within a metropolitan area. This is particularly relevant for applications like vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, which are crucial for the development of smart cities and autonomous driving. Ethernet switch chips in automotive MANs enable high-speed data transfer between vehicles and roadside units, facilitating real-time traffic management, collision avoidance, and other advanced driver-assistance systems (ADAS). The integration of Ethernet switch chips in both LAN and MAN networks is driven by the need for higher bandwidth, lower latency, and greater reliability in automotive communication systems. As vehicles become more connected and autonomous, the demand for robust networking solutions will continue to grow, making Ethernet switch chips an indispensable component in modern automotive design.

Passenger Vehicle, Commercial Vehicle in the Global Automotive Ethernet Switch Chips Market:

The usage of Global Automotive Ethernet Switch Chips Market in passenger vehicles and commercial vehicles is extensive and multifaceted. In passenger vehicles, these chips are primarily used to support advanced driver-assistance systems (ADAS), infotainment systems, and in-car networking. ADAS features such as adaptive cruise control, lane-keeping assist, and automatic emergency braking rely on real-time data communication between various sensors and control units. Ethernet switch chips ensure that this data is transmitted quickly and reliably, enhancing the safety and performance of these systems. In-car infotainment systems, which include navigation, audio, video, and internet connectivity, also benefit from the high-speed data transfer capabilities of Ethernet switch chips. These chips enable seamless streaming of high-definition content and real-time navigation updates, providing a better user experience for passengers. In commercial vehicles, the application of Ethernet switch chips is equally critical. Commercial vehicles, such as trucks and buses, often require robust communication networks to support fleet management systems, telematics, and advanced safety features. Fleet management systems rely on real-time data from various sensors and control units to monitor vehicle performance, track location, and optimize routes. Ethernet switch chips facilitate this by providing a reliable and high-speed communication network within the vehicle. Telematics systems, which include GPS tracking, remote diagnostics, and driver behavior monitoring, also depend on efficient data communication enabled by Ethernet switch chips. Additionally, commercial vehicles are increasingly being equipped with advanced safety features similar to those in passenger vehicles, such as collision avoidance systems and blind-spot detection. These systems require real-time data communication between sensors and control units, which is made possible by Ethernet switch chips. Overall, the integration of Ethernet switch chips in both passenger and commercial vehicles is essential for supporting the advanced features and functionalities that modern vehicles demand.

Global Automotive Ethernet Switch Chips Market Outlook:

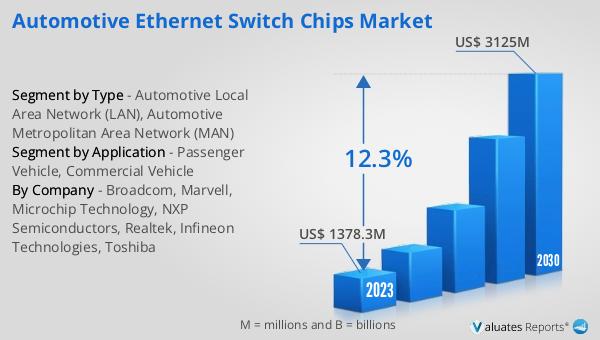

The global Automotive Ethernet Switch Chips market was valued at US$ 1378.3 million in 2023 and is anticipated to reach US$ 3125 million by 2030, witnessing a CAGR of 12.3% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced networking solutions in the automotive industry. As vehicles become more connected and autonomous, the need for reliable and high-speed data communication networks is paramount. Ethernet switch chips provide the necessary infrastructure to support these advanced features, ensuring seamless communication between various electronic systems within the vehicle. The market's robust growth is driven by the rising adoption of advanced driver-assistance systems (ADAS), infotainment systems, and in-car networking solutions in both passenger and commercial vehicles. Additionally, the development of smart cities and the increasing focus on vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication further fuel the demand for Ethernet switch chips. As automakers and suppliers continue to invest in advanced networking technologies, the global Automotive Ethernet Switch Chips market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Automotive Ethernet Switch Chips Market |

| Accounted market size in 2023 | US$ 1378.3 million |

| Forecasted market size in 2030 | US$ 3125 million |

| CAGR | 12.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Broadcom, Marvell, Microchip Technology, NXP Semiconductors, Realtek, Infineon Technologies, Toshiba |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |