What is Global Medical Polymer Materials Market?

The Global Medical Polymer Materials Market is a rapidly evolving sector that plays a crucial role in the healthcare industry. These materials are specifically designed for medical applications, offering properties such as biocompatibility, durability, and flexibility. They are used in a wide range of medical devices and products, including surgical instruments, implants, and diagnostic equipment. The market is driven by the increasing demand for advanced medical technologies and the growing prevalence of chronic diseases. Additionally, the aging population and the rising need for minimally invasive surgical procedures are contributing to the market's growth. The development of new and innovative polymer materials, along with advancements in manufacturing technologies, is expected to further propel the market. Overall, the Global Medical Polymer Materials Market is poised for significant growth, driven by the continuous advancements in medical technology and the increasing demand for high-quality medical products.

Bioabsorbable Polymer, Biocompatible Polymer, Others in the Global Medical Polymer Materials Market:

Bioabsorbable polymers, biocompatible polymers, and other types of polymers play a significant role in the Global Medical Polymer Materials Market. Bioabsorbable polymers are designed to be absorbed by the body over time, eliminating the need for a second surgery to remove implants or devices. These materials are commonly used in applications such as sutures, stents, and drug delivery systems. They offer several advantages, including reduced risk of infection and improved patient outcomes. Biocompatible polymers, on the other hand, are designed to be compatible with the human body, minimizing the risk of adverse reactions. These materials are used in a wide range of medical devices, including catheters, prosthetics, and orthopedic implants. They offer excellent mechanical properties, such as strength and flexibility, making them ideal for use in various medical applications. Other types of polymers used in the medical field include thermoplastic elastomers, which offer a combination of elasticity and strength, and thermosetting polymers, which provide excellent chemical resistance and stability. These materials are used in applications such as medical tubing, seals, and gaskets. The development of new and innovative polymer materials is driving the growth of the Global Medical Polymer Materials Market. Researchers and manufacturers are continuously working on improving the properties of these materials to meet the evolving needs of the healthcare industry. For example, the development of smart polymers, which can respond to changes in the environment, is expected to open up new possibilities for medical applications. Additionally, the use of nanotechnology in the development of medical polymers is gaining traction, offering the potential for improved drug delivery systems and advanced diagnostic tools. Overall, the Global Medical Polymer Materials Market is characterized by continuous innovation and advancements in material science, driven by the increasing demand for high-quality medical products and the need for improved patient outcomes.

Hospital, Clinic in the Global Medical Polymer Materials Market:

The usage of Global Medical Polymer Materials Market in hospitals and clinics is extensive and varied, playing a crucial role in modern healthcare. In hospitals, these materials are used in a wide range of applications, from surgical instruments and implants to diagnostic equipment and medical disposables. For instance, bioabsorbable polymers are commonly used in surgical sutures and stents, which are designed to be absorbed by the body over time, reducing the need for additional surgeries. Biocompatible polymers are used in the production of catheters, prosthetics, and orthopedic implants, offering excellent mechanical properties and minimizing the risk of adverse reactions. In addition to these applications, medical polymers are also used in the production of medical tubing, seals, and gaskets, which are essential components in various medical devices and equipment. In clinics, the usage of medical polymer materials is equally important. These materials are used in a wide range of diagnostic and therapeutic applications, including imaging equipment, drug delivery systems, and wound care products. For example, biocompatible polymers are used in the production of diagnostic imaging equipment, such as MRI and CT scanners, offering excellent mechanical properties and ensuring patient safety. Bioabsorbable polymers are used in drug delivery systems, providing controlled release of medications and improving patient outcomes. Additionally, medical polymers are used in the production of wound care products, such as dressings and bandages, offering excellent absorbency and promoting faster healing. The use of medical polymer materials in hospitals and clinics is driven by the need for high-quality, reliable, and safe medical products. These materials offer several advantages, including biocompatibility, durability, and flexibility, making them ideal for use in various medical applications. The continuous advancements in material science and the development of new and innovative polymer materials are expected to further drive the growth of the Global Medical Polymer Materials Market. Overall, the usage of medical polymer materials in hospitals and clinics is essential for providing high-quality healthcare and improving patient outcomes.

Global Medical Polymer Materials Market Outlook:

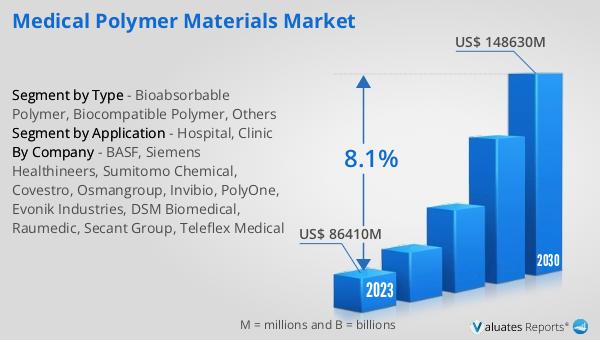

The global Medical Polymer Materials market was valued at US$ 86,410 million in 2023 and is anticipated to reach US$ 148,630 million by 2030, witnessing a CAGR of 8.1% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for advanced medical technologies and high-quality medical products. The market's expansion is driven by several factors, including the rising prevalence of chronic diseases, the aging population, and the growing need for minimally invasive surgical procedures. Additionally, continuous advancements in material science and the development of new and innovative polymer materials are contributing to the market's growth. The increasing adoption of bioabsorbable and biocompatible polymers in various medical applications is also playing a crucial role in driving the market. These materials offer several advantages, such as reduced risk of infection, improved patient outcomes, and the elimination of the need for additional surgeries. Furthermore, the use of nanotechnology in the development of medical polymers is gaining traction, offering the potential for improved drug delivery systems and advanced diagnostic tools. Overall, the Global Medical Polymer Materials Market is poised for significant growth, driven by the continuous advancements in medical technology and the increasing demand for high-quality medical products.

| Report Metric | Details |

| Report Name | Medical Polymer Materials Market |

| Accounted market size in 2023 | US$ 86410 million |

| Forecasted market size in 2030 | US$ 148630 million |

| CAGR | 8.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BASF, Siemens Healthineers, Sumitomo Chemical, Covestro, Osmangroup, Invibio, PolyOne, Evonik Industries, DSM Biomedical, Raumedic, Secant Group, Teleflex Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |