What is Global Optical Grating Sensors Market?

The Global Optical Grating Sensors Market is a rapidly evolving sector that focuses on the development and deployment of optical grating sensors. These sensors are used to measure various physical parameters such as strain, temperature, and pressure by analyzing the changes in light properties as it passes through or reflects off a grating. Optical grating sensors are highly valued for their precision, reliability, and ability to operate in harsh environments. They are widely used in industries such as aerospace, defense, chemical, and power due to their robustness and accuracy. The market for these sensors is expanding as technological advancements continue to improve their performance and reduce costs, making them more accessible for a broader range of applications. The increasing demand for high-precision measurement tools in various industries is a significant driver for the growth of the Global Optical Grating Sensors Market.

Bragg Grating, Transmission Grating in the Global Optical Grating Sensors Market:

Bragg Grating and Transmission Grating are two primary types of optical grating sensors used in the Global Optical Grating Sensors Market. Bragg Grating sensors, also known as Fiber Bragg Gratings (FBGs), are created by inscribing a periodic variation in the refractive index along the core of an optical fiber. When light travels through the fiber, specific wavelengths are reflected back while others pass through, creating a unique spectral signature that can be analyzed to determine changes in strain, temperature, or pressure. This makes Bragg Grating sensors highly effective for monitoring structural health in buildings, bridges, and other critical infrastructure. On the other hand, Transmission Grating sensors work by diffracting light into multiple beams as it passes through a grating. These sensors are often used in spectroscopy and telecommunications to separate light into its component wavelengths for analysis. Transmission Grating sensors are particularly useful in applications requiring high spectral resolution and sensitivity. Both types of sensors offer distinct advantages and are chosen based on the specific requirements of the application. The versatility and precision of these sensors make them indispensable tools in various industries, driving the growth of the Global Optical Grating Sensors Market.

Chemical Industry, Aerospace & Defense, Power Industry, Others in the Global Optical Grating Sensors Market:

The usage of Global Optical Grating Sensors Market in the Chemical Industry, Aerospace & Defense, Power Industry, and other sectors is extensive and varied. In the Chemical Industry, optical grating sensors are used for monitoring chemical processes, detecting leaks, and ensuring the safety and efficiency of operations. Their ability to provide real-time data on temperature, pressure, and strain makes them invaluable for maintaining optimal conditions in chemical plants. In the Aerospace & Defense sector, these sensors are employed for structural health monitoring of aircraft, spacecraft, and military equipment. They help in detecting any potential issues before they become critical, ensuring the safety and reliability of these high-stakes applications. In the Power Industry, optical grating sensors are used for monitoring the health of power grids, detecting faults, and optimizing the performance of power generation and distribution systems. Their ability to operate in harsh environments and provide accurate data makes them ideal for this sector. Additionally, optical grating sensors find applications in other areas such as civil engineering, medical devices, and environmental monitoring. Their versatility and precision make them suitable for a wide range of applications, contributing to the growth of the Global Optical Grating Sensors Market.

Global Optical Grating Sensors Market Outlook:

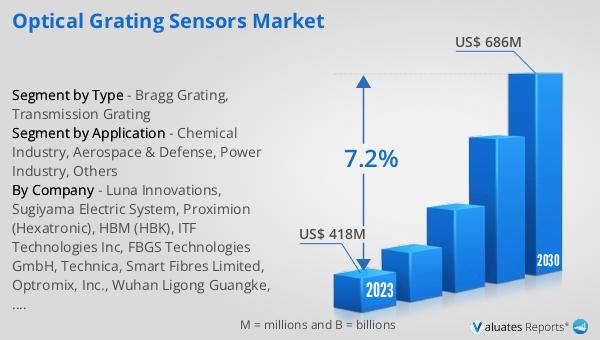

The global Optical Grating Sensors market was valued at US$ 418 million in 2023 and is anticipated to reach US$ 686 million by 2030, witnessing a CAGR of 7.2% during the forecast period 2024-2030. This significant growth is driven by the increasing demand for high-precision measurement tools across various industries. The advancements in technology have improved the performance and reduced the costs of optical grating sensors, making them more accessible for a broader range of applications. The market's expansion is also fueled by the growing need for reliable and accurate sensors that can operate in harsh environments. As industries continue to seek innovative solutions for monitoring and optimizing their operations, the demand for optical grating sensors is expected to rise, contributing to the overall growth of the market.

| Report Metric | Details |

| Report Name | Optical Grating Sensors Market |

| Accounted market size in 2023 | US$ 418 million |

| Forecasted market size in 2030 | US$ 686 million |

| CAGR | 7.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Luna Innovations, Sugiyama Electric System, Proximion (Hexatronic), HBM (HBK), ITF Technologies Inc, FBGS Technologies GmbH, Technica, Smart Fibres Limited, Optromix, Inc., Wuhan Ligong Guangke, FBG Korea, Smartec (Roctest), Timbercon (Radiall) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |