What is Global Touch Wall Light Switch Market?

The Global Touch Wall Light Switch Market refers to the worldwide industry focused on the production, distribution, and sale of touch-sensitive wall light switches. These switches are designed to replace traditional mechanical switches, offering a more modern and user-friendly interface for controlling lighting in various settings. Touch wall light switches use advanced technology to detect the presence of a finger or hand, allowing users to turn lights on or off with a simple touch. This market encompasses a wide range of products, including different types of touch switches, such as resistive and capacitive touch switches, which cater to various consumer preferences and needs. The market is driven by the increasing demand for smart home solutions, energy efficiency, and the growing trend of home automation. As more consumers seek to upgrade their living spaces with modern, convenient, and aesthetically pleasing devices, the global touch wall light switch market continues to expand, offering innovative solutions to enhance the user experience.

Resistive Touch Switch, Capacitive Touch Switch in the Global Touch Wall Light Switch Market:

Resistive touch switches and capacitive touch switches are two primary types of touch-sensitive switches used in the global touch wall light switch market. Resistive touch switches operate based on pressure applied to the surface. When a user touches the switch, it creates a physical connection between two conductive layers, completing the circuit and triggering the switch. These switches are known for their durability and reliability, making them suitable for various applications, including residential and commercial settings. They are also relatively cost-effective, which makes them an attractive option for budget-conscious consumers. However, resistive touch switches may require more force to operate compared to capacitive touch switches, which can be a drawback for some users. On the other hand, capacitive touch switches work by detecting changes in the electrical field caused by the presence of a finger or hand. These switches are highly sensitive and can be activated with a light touch, providing a more seamless and intuitive user experience. Capacitive touch switches are often preferred for their sleek design and ease of use, making them a popular choice for modern homes and commercial spaces. They are also more responsive and can support multi-touch functionality, which adds to their versatility. However, capacitive touch switches can be more expensive than resistive touch switches, which may limit their adoption in some markets. In the global touch wall light switch market, both resistive and capacitive touch switches have their unique advantages and disadvantages. The choice between the two often depends on the specific needs and preferences of the consumers. For instance, in residential settings, capacitive touch switches are often favored for their aesthetic appeal and user-friendly interface. Homeowners looking to create a modern and sophisticated living environment may opt for capacitive touch switches to complement their home automation systems. These switches can be integrated with other smart home devices, allowing users to control their lighting through voice commands or mobile apps, enhancing convenience and energy efficiency. In commercial settings, the choice between resistive and capacitive touch switches may depend on factors such as cost, durability, and ease of maintenance. Resistive touch switches, with their robust construction and lower cost, may be preferred in high-traffic areas where durability is a key consideration. For example, in office buildings, hotels, and retail spaces, resistive touch switches can withstand frequent use and are less likely to be damaged by accidental impacts. On the other hand, capacitive touch switches, with their sleek design and advanced functionality, may be chosen for upscale commercial spaces where aesthetics and user experience are paramount. These switches can enhance the overall ambiance of the space, creating a more inviting and modern environment for customers and clients. Overall, the global touch wall light switch market offers a wide range of options to cater to different consumer needs and preferences. Whether it's the durability and cost-effectiveness of resistive touch switches or the sleek design and advanced functionality of capacitive touch switches, there is a solution for every application. As technology continues to evolve, we can expect to see further innovations in this market, providing even more sophisticated and user-friendly touch wall light switches for both residential and commercial use.

Residential, Commercial in the Global Touch Wall Light Switch Market:

The usage of touch wall light switches in residential areas has seen a significant rise due to the growing trend of smart homes and home automation. Homeowners are increasingly looking for ways to enhance the convenience, efficiency, and aesthetics of their living spaces. Touch wall light switches offer a modern and intuitive way to control lighting, replacing traditional mechanical switches with a sleek and user-friendly interface. These switches can be easily integrated with other smart home devices, allowing users to control their lighting through voice commands, mobile apps, or even automated schedules. This integration not only adds to the convenience but also helps in energy management by allowing users to set timers or dim lights based on their preferences. Additionally, touch wall light switches come in various designs and finishes, enabling homeowners to choose options that complement their interior decor. The ease of installation and the ability to retrofit existing electrical systems make these switches an attractive option for both new constructions and home renovations. In commercial settings, touch wall light switches are being adopted to enhance the functionality and aesthetics of various spaces. Offices, hotels, retail stores, and other commercial establishments are increasingly opting for touch-sensitive switches to create a modern and sophisticated environment. These switches not only offer a sleek and contemporary look but also provide practical benefits such as ease of use and durability. In high-traffic areas, touch wall light switches can withstand frequent use and are less prone to wear and tear compared to traditional mechanical switches. Moreover, the ability to integrate these switches with building management systems allows for centralized control of lighting, contributing to energy efficiency and cost savings. For instance, in office buildings, touch wall light switches can be programmed to turn off lights automatically when rooms are unoccupied, reducing energy consumption. In hotels, these switches can enhance the guest experience by providing intuitive and easy-to-use lighting controls in guest rooms and common areas. Retail stores can use touch wall light switches to create dynamic lighting effects that enhance product displays and create an inviting shopping environment. Overall, the adoption of touch wall light switches in both residential and commercial settings is driven by the desire for modern, convenient, and energy-efficient lighting solutions. These switches offer a range of benefits, from enhancing the user experience to contributing to energy management and cost savings. As technology continues to advance, we can expect to see even more innovative features and functionalities in touch wall light switches, further driving their adoption in various applications.

Global Touch Wall Light Switch Market Outlook:

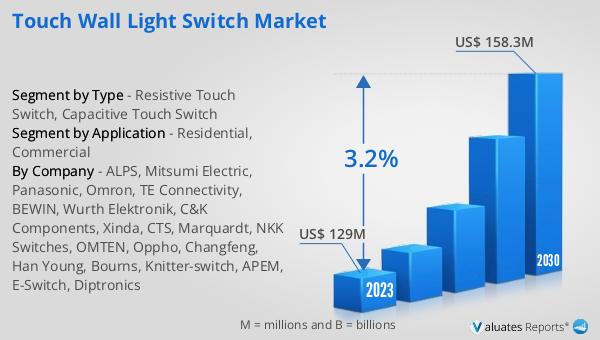

The global touch wall light switch market was valued at US$ 129 million in 2023 and is expected to grow to US$ 158.3 million by 2030, with a compound annual growth rate (CAGR) of 3.2% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for smart home solutions and the trend towards home automation. As consumers seek to upgrade their living spaces with modern and convenient devices, the market for touch wall light switches is expanding. These switches offer a user-friendly interface and can be easily integrated with other smart home devices, enhancing the overall user experience. Additionally, the growing awareness of energy efficiency and the need for sustainable solutions are contributing to the market's growth. Touch wall light switches allow users to control their lighting more efficiently, reducing energy consumption and lowering utility bills. The market is also benefiting from advancements in technology, which are leading to the development of more sophisticated and feature-rich touch wall light switches. As a result, the global touch wall light switch market is poised for steady growth in the coming years.

| Report Metric | Details |

| Report Name | Touch Wall Light Switch Market |

| Accounted market size in 2023 | US$ 129 million |

| Forecasted market size in 2030 | US$ 158.3 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ALPS, Mitsumi Electric, Panasonic, Omron, TE Connectivity, BEWIN, Wurth Elektronik, C&K Components, Xinda, CTS, Marquardt, NKK Switches, OMTEN, Oppho, Changfeng, Han Young, Bourns, Knitter-switch, APEM, E-Switch, Diptronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |