What is Global Food Grade NAC (Acetylcysteine) Market?

The global Food Grade NAC (Acetylcysteine) market is a specialized segment within the broader nutraceutical and pharmaceutical industries. NAC, or N-Acetylcysteine, is a derivative of the amino acid cysteine and is known for its antioxidant properties and ability to replenish glutathione levels in the body. Food grade NAC is specifically formulated for use in dietary supplements and functional foods, ensuring it meets stringent safety and purity standards. This market is driven by increasing consumer awareness about health and wellness, particularly the benefits of antioxidants in combating oxidative stress and supporting immune function. The demand for food grade NAC is also bolstered by its applications in managing chronic conditions such as respiratory disorders and liver diseases. As consumers become more health-conscious and seek preventive healthcare solutions, the global Food Grade NAC market is poised for significant growth. The market's expansion is further supported by advancements in production technologies and the development of innovative product formulations that enhance the bioavailability and efficacy of NAC.

Effervescent Tablets, Capsule, Others in the Global Food Grade NAC (Acetylcysteine) Market:

Effervescent tablets, capsules, and other forms of NAC (N-Acetylcysteine) are integral to the global Food Grade NAC market, each offering unique benefits and catering to different consumer preferences. Effervescent tablets are popular due to their convenience and rapid absorption. When dissolved in water, these tablets create a fizzy drink that is not only easy to consume but also ensures that the NAC is quickly absorbed into the bloodstream. This form is particularly appealing to individuals who have difficulty swallowing pills or prefer a more palatable option. Effervescent tablets are often flavored, making them an enjoyable way to take supplements. Capsules, on the other hand, are favored for their precision in dosing and ease of storage. They are typically made from gelatin or plant-based materials and contain a measured amount of NAC powder. Capsules are convenient for those who prefer a straightforward, no-fuss method of supplementation. They are also ideal for individuals who need to take NAC on the go, as they can be easily carried in a purse or pocket. Other forms of NAC in the market include powders, chewable tablets, and liquid formulations. Powders offer flexibility in dosing and can be mixed with various beverages or foods, making them a versatile option for consumers. Chewable tablets provide a convenient and often tasty alternative for those who dislike swallowing pills. Liquid formulations are particularly beneficial for children or elderly individuals who may have difficulty with solid forms of supplements. Each of these forms has its own set of advantages, and the choice often depends on individual preferences, lifestyle, and specific health needs. The diversity in product forms within the global Food Grade NAC market ensures that there is an option to suit every consumer, thereby broadening the market's appeal and accessibility.

Online, Offline in the Global Food Grade NAC (Acetylcysteine) Market:

The usage of Global Food Grade NAC (Acetylcysteine) in online and offline markets highlights the diverse channels through which consumers can access this beneficial supplement. Online platforms have revolutionized the way consumers purchase dietary supplements, offering unparalleled convenience and a wide range of options. E-commerce websites, health and wellness portals, and online pharmacies provide detailed product information, customer reviews, and competitive pricing, making it easier for consumers to make informed decisions. The online market also allows for direct-to-consumer sales, which can reduce costs and increase accessibility. Subscription services for NAC supplements are becoming increasingly popular, providing consumers with regular deliveries and often at a discounted rate. This model not only ensures a steady supply of the supplement but also fosters brand loyalty. On the other hand, offline markets, including brick-and-mortar stores such as pharmacies, health food stores, and supermarkets, continue to play a crucial role in the distribution of NAC supplements. These physical stores offer the advantage of immediate purchase and the ability to consult with knowledgeable staff. Many consumers still prefer the tactile experience of shopping in a store, where they can see and feel the product before buying. Additionally, offline channels often provide opportunities for in-store promotions, sampling, and personalized customer service, which can enhance the shopping experience. The presence of NAC supplements in both online and offline markets ensures that they are accessible to a broad audience, catering to different shopping preferences and needs. The synergy between these two channels also allows for a comprehensive market reach, ensuring that consumers can easily find and purchase NAC supplements regardless of their preferred shopping method.

Global Food Grade NAC (Acetylcysteine) Market Outlook:

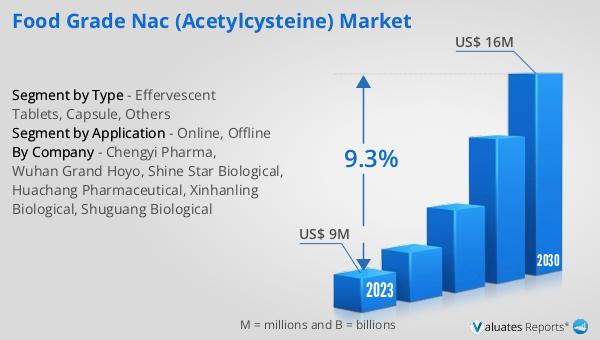

The global Food Grade NAC (Acetylcysteine) market was valued at US$ 9 million in 2023 and is projected to reach US$ 16 million by 2030, reflecting a compound annual growth rate (CAGR) of 9.3% during the forecast period from 2024 to 2030. This significant growth underscores the increasing demand for NAC as a dietary supplement, driven by its recognized health benefits and rising consumer awareness. The market's expansion is indicative of a broader trend towards preventive healthcare and the growing popularity of nutraceuticals. As more consumers seek natural and effective ways to support their health, the demand for high-quality, food grade NAC is expected to continue its upward trajectory. This positive market outlook highlights the potential for innovation and development within the industry, as manufacturers strive to meet the evolving needs and preferences of health-conscious consumers.

| Report Metric | Details |

| Report Name | Food Grade NAC (Acetylcysteine) Market |

| Accounted market size in 2023 | US$ 9 million |

| Forecasted market size in 2030 | US$ 16 million |

| CAGR | 9.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Chengyi Pharma, Wuhan Grand Hoyo, Shine Star Biological, Huachang Pharmaceutical, Xinhanling Biological, Shuguang Biological |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |