What is Global Food Grade Ethyl Oleate Market?

The Global Food Grade Ethyl Oleate Market refers to the worldwide industry involved in the production, distribution, and sale of ethyl oleate that meets food-grade standards. Ethyl oleate is an ester formed by the condensation of oleic acid and ethanol. It is commonly used as a solvent, emulsifier, and lubricant in various food and beverage applications. The market encompasses a wide range of activities, including the sourcing of raw materials, manufacturing processes, quality control, packaging, and distribution channels. Companies operating in this market must adhere to stringent regulatory standards to ensure the safety and quality of their products. The demand for food-grade ethyl oleate is driven by its versatility and effectiveness in enhancing the texture, flavor, and shelf-life of food products. As consumer preferences shift towards natural and clean-label ingredients, the market for food-grade ethyl oleate is expected to grow.

Purity <98%, Purity ≥98% in the Global Food Grade Ethyl Oleate Market:

In the Global Food Grade Ethyl Oleate Market, the purity of the product is a critical factor that determines its suitability for various applications. Products with a purity of less than 98% (Purity <98%) are generally considered lower-grade and may contain impurities that can affect their performance and safety in food applications. These lower-purity products are often used in less demanding applications where the presence of impurities does not significantly impact the end product. On the other hand, products with a purity of 98% or higher (Purity ≥98%) are considered high-grade and are preferred for applications that require stringent quality and safety standards. High-purity ethyl oleate is used in premium food and beverage products where the presence of impurities could affect the taste, texture, or safety of the final product. The production of high-purity ethyl oleate involves more rigorous manufacturing processes and quality control measures to ensure that the product meets the required standards. This often includes advanced purification techniques, such as distillation and filtration, to remove impurities and achieve the desired level of purity. The demand for high-purity ethyl oleate is driven by the increasing consumer preference for high-quality, safe, and natural food ingredients. As a result, manufacturers are investing in advanced technologies and processes to produce high-purity ethyl oleate that meets the stringent requirements of the food industry. The market for high-purity ethyl oleate is also influenced by regulatory standards and guidelines that mandate the use of high-quality ingredients in food products. Compliance with these standards is essential for manufacturers to ensure the safety and quality of their products and to maintain consumer trust. In summary, the purity of ethyl oleate is a key factor that influences its application and demand in the Global Food Grade Ethyl Oleate Market. Products with a purity of less than 98% are generally used in less demanding applications, while high-purity products with a purity of 98% or higher are preferred for premium food and beverage applications. The production of high-purity ethyl oleate involves advanced manufacturing processes and quality control measures to ensure that the product meets the required standards. The demand for high-purity ethyl oleate is driven by consumer preferences for high-quality, safe, and natural food ingredients, as well as regulatory standards that mandate the use of high-quality ingredients in food products.

Food, Beverage, Others in the Global Food Grade Ethyl Oleate Market:

The Global Food Grade Ethyl Oleate Market finds its usage in various areas, including food, beverage, and others. In the food industry, ethyl oleate is used as an emulsifier and lubricant to improve the texture and consistency of various food products. It is commonly used in baked goods, confectionery, and processed foods to enhance their mouthfeel and shelf-life. Ethyl oleate helps in the even distribution of ingredients, preventing separation and ensuring a uniform texture. In the beverage industry, ethyl oleate is used as a flavoring agent and solvent for various flavor compounds. It helps in the dissolution and dispersion of flavoring agents, ensuring a consistent and stable flavor profile in beverages. Ethyl oleate is also used in the production of alcoholic beverages, where it acts as a carrier for flavor compounds and enhances the overall sensory experience. In addition to food and beverage applications, ethyl oleate is used in other areas such as pharmaceuticals and cosmetics. In the pharmaceutical industry, it is used as a solvent and carrier for active pharmaceutical ingredients (APIs) in various formulations. Ethyl oleate is preferred for its biocompatibility and ability to enhance the bioavailability of APIs. In the cosmetics industry, ethyl oleate is used as an emollient and skin-conditioning agent in various skincare and personal care products. It helps in improving the texture and spreadability of cosmetic formulations, providing a smooth and silky feel to the skin. Overall, the versatility and effectiveness of ethyl oleate make it a valuable ingredient in various industries, including food, beverage, pharmaceuticals, and cosmetics. Its ability to enhance the texture, flavor, and stability of products, along with its biocompatibility and safety, drive its demand in the Global Food Grade Ethyl Oleate Market.

Global Food Grade Ethyl Oleate Market Outlook:

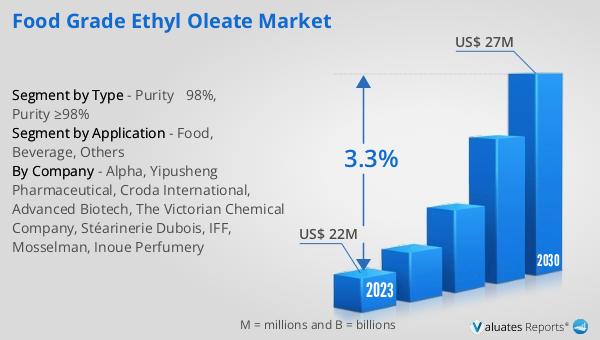

The global Food Grade Ethyl Oleate market was valued at US$ 22 million in 2023 and is anticipated to reach US$ 27 million by 2030, witnessing a CAGR of 3.3% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the food-grade ethyl oleate industry over the next several years. The increase in market value from US$ 22 million to US$ 27 million reflects a growing demand for high-quality, safe, and natural food ingredients. The compound annual growth rate (CAGR) of 3.3% suggests a consistent and moderate expansion of the market, driven by factors such as consumer preferences for clean-label products, advancements in manufacturing technologies, and stringent regulatory standards. Companies operating in this market are likely to focus on enhancing their production capabilities, improving product quality, and expanding their distribution networks to capitalize on the growing demand. The market outlook also highlights the importance of innovation and investment in research and development to meet the evolving needs of consumers and regulatory requirements. Overall, the global Food Grade Ethyl Oleate market is poised for steady growth, driven by increasing consumer awareness and demand for high-quality food ingredients.

| Report Metric | Details |

| Report Name | Food Grade Ethyl Oleate Market |

| Accounted market size in 2023 | US$ 22 million |

| Forecasted market size in 2030 | US$ 27 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Alpha, Yipusheng Pharmaceutical, Croda International, Advanced Biotech, The Victorian Chemical Company, Stéarinerie Dubois, IFF, Mosselman, Inoue Perfumery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |