What is Global Capacitors Film Producting Lines Market?

The Global Capacitors Film Producing Lines Market is a specialized segment within the broader electronics manufacturing industry. This market focuses on the production lines that manufacture film capacitors, which are essential components in various electronic devices. Film capacitors are known for their reliability, stability, and long lifespan, making them crucial in applications ranging from consumer electronics to industrial machinery. The production lines for these capacitors involve sophisticated machinery and technology to ensure high precision and quality. These lines are designed to handle different types of film materials, such as polypropylene (PP) and polyethylene terephthalate (PET), which are used to create the dielectric layers in capacitors. The market for these production lines is driven by the increasing demand for electronic devices and the need for efficient energy storage solutions. As technology advances, the production lines are also evolving to incorporate automation and advanced quality control measures, ensuring that the capacitors meet the stringent requirements of modern electronic applications.

PP Film Lines, PET Film Lines, Others in the Global Capacitors Film Producting Lines Market:

PP Film Lines, PET Film Lines, and other types of film lines play a crucial role in the Global Capacitors Film Producing Lines Market. PP Film Lines are designed to produce capacitors using polypropylene film, which is known for its excellent electrical properties, high dielectric strength, and low dissipation factor. These lines are equipped with advanced machinery that can handle the delicate process of stretching and forming the PP film into the required shapes and sizes. The production process involves several stages, including extrusion, stretching, and winding, each of which requires precise control to ensure the quality of the final product. PET Film Lines, on the other hand, use polyethylene terephthalate film, which offers good thermal stability and mechanical strength. These lines are similar to PP Film Lines in terms of the machinery and processes involved, but they are optimized to handle the specific properties of PET film. The production process for PET film capacitors also includes extrusion, stretching, and winding, but with adjustments to accommodate the different material characteristics. Other types of film lines in this market include those that use materials like polycarbonate (PC) and polystyrene (PS), which are used for specialized applications requiring specific electrical and thermal properties. These lines are typically customized to meet the unique requirements of the materials they handle, ensuring that the capacitors produced meet the necessary performance standards. The Global Capacitors Film Producing Lines Market is characterized by continuous innovation and development, with manufacturers constantly seeking to improve the efficiency and quality of their production lines. This includes the integration of automation and advanced quality control systems, which help to reduce production costs and improve the consistency of the final products. As the demand for electronic devices and energy storage solutions continues to grow, the market for capacitors film producing lines is expected to expand, driven by the need for high-quality, reliable capacitors.

Solar Industry, Household Appliances, Power And Smart Grid, Automotive, Locomotive, Industry And Infrastructure, Others in the Global Capacitors Film Producting Lines Market:

The usage of Global Capacitors Film Producing Lines Market spans several key areas, including the solar industry, household appliances, power and smart grid, automotive, locomotive, industry and infrastructure, and others. In the solar industry, film capacitors are used in inverters and other power conversion equipment, where their high reliability and long lifespan are crucial for the efficient operation of solar power systems. These capacitors help to smooth out voltage fluctuations and improve the overall efficiency of the system. In household appliances, film capacitors are used in a variety of applications, including motor run capacitors, power factor correction, and EMI suppression. Their stability and reliability make them ideal for use in appliances that require consistent performance over long periods. In the power and smart grid sector, film capacitors are used in power conditioning and energy storage systems, where their ability to handle high voltages and currents is essential for maintaining grid stability and efficiency. In the automotive industry, film capacitors are used in electric and hybrid vehicles, where they help to manage power distribution and improve the efficiency of the vehicle's electrical systems. They are also used in various electronic control units (ECUs) and other automotive electronics, where their reliability and performance are critical. In the locomotive industry, film capacitors are used in traction systems and other power electronics, where their ability to handle high power levels and harsh operating conditions is essential. In the industrial and infrastructure sectors, film capacitors are used in a wide range of applications, including motor drives, power supplies, and lighting systems. Their durability and performance make them ideal for use in demanding industrial environments. Other areas where film capacitors are used include telecommunications, medical equipment, and aerospace, where their high performance and reliability are essential for the proper functioning of critical systems. The Global Capacitors Film Producing Lines Market plays a vital role in supporting these diverse applications, providing the high-quality capacitors needed to meet the demands of modern technology.

Global Capacitors Film Producting Lines Market Outlook:

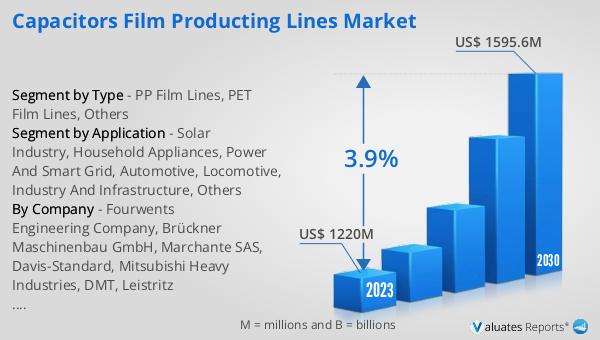

The global Capacitors Film Producing Lines market was valued at US$ 1220 million in 2023 and is anticipated to reach US$ 1595.6 million by 2030, witnessing a CAGR of 3.9% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for electronic devices and energy storage solutions. The market's growth is supported by advancements in production technology, which are enabling manufacturers to produce high-quality capacitors more efficiently. The integration of automation and advanced quality control measures is also playing a significant role in improving production efficiency and product consistency. As the demand for reliable and efficient capacitors continues to grow across various industries, the market for capacitors film producing lines is expected to expand. This growth is further supported by the increasing adoption of renewable energy sources, such as solar power, which require high-quality capacitors for efficient power conversion and storage. The automotive industry is also a key driver of market growth, with the increasing adoption of electric and hybrid vehicles creating a strong demand for capacitors. Overall, the global Capacitors Film Producing Lines market is poised for steady growth, driven by the ongoing advancements in production technology and the increasing demand for high-quality capacitors across various industries.

| Report Metric | Details |

| Report Name | Capacitors Film Producting Lines Market |

| Accounted market size in 2023 | US$ 1220 million |

| Forecasted market size in 2030 | US$ 1595.6 million |

| CAGR | 3.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Fourwents Engineering Company, Brückner Maschinenbau GmbH, Marchante SAS, Davis-Standard, Mitsubishi Heavy Industries, DMT, Leistritz Extrusionstechnik GmbH, Lindauer DORNIER GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |