What is Global Probe Card for Wafer Testing Market?

The Global Probe Card for Wafer Testing Market is a specialized sector within the semiconductor industry that focuses on the production and utilization of probe cards. These probe cards are essential tools used in the testing of semiconductor wafers, which are thin slices of semiconductor material, such as silicon, used in the fabrication of integrated circuits and other microdevices. The primary function of a probe card is to establish an electrical connection between the test equipment and the semiconductor wafer, allowing for the testing of the electrical properties of the circuits on the wafer. This testing is crucial for ensuring the quality and functionality of the semiconductor devices before they are packaged and sold. The market for probe cards is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, telecommunications, and industrial sectors. As technology advances and the complexity of semiconductor devices increases, the need for more sophisticated and reliable probe cards also grows, making this market an essential component of the semiconductor manufacturing process.

Blade Probe Card, Cantilever Probe Card, vertical Probe Card, Membrane Probe Card, MEMS Probe Card in the Global Probe Card for Wafer Testing Market:

In the Global Probe Card for Wafer Testing Market, several types of probe cards are utilized, each with its unique design and application. Blade Probe Cards are known for their simplicity and cost-effectiveness. They consist of a series of metal blades that make contact with the wafer, providing a straightforward solution for testing. Cantilever Probe Cards, on the other hand, feature probes that extend from the card at an angle, resembling a cantilever beam. This design allows for precise contact with the wafer and is often used for testing devices with fine-pitch requirements. Vertical Probe Cards are designed with probes that make vertical contact with the wafer, offering high-density testing capabilities and minimizing the risk of damage to the wafer. Membrane Probe Cards utilize a flexible membrane to establish contact with the wafer, providing a high degree of compliance and adaptability to different wafer topographies. MEMS (Micro-Electro-Mechanical Systems) Probe Cards are the most advanced type, incorporating microfabricated structures to achieve high precision and reliability in testing. These probe cards are particularly suited for testing advanced semiconductor devices with complex architectures. Each type of probe card has its advantages and is selected based on the specific requirements of the testing application, such as the type of semiconductor device, the pitch of the contacts, and the desired level of precision and reliability. The diversity of probe card types in the market reflects the wide range of testing needs in the semiconductor industry, from basic functionality tests to highly sophisticated evaluations of cutting-edge devices.

Wireless Communication, RF Circuit, Microwave Measurement, Signal Transmission, Others in the Global Probe Card for Wafer Testing Market:

The usage of Global Probe Cards for Wafer Testing Market spans several critical areas, including Wireless Communication, RF Circuit, Microwave Measurement, Signal Transmission, and others. In Wireless Communication, probe cards are used to test the performance and reliability of semiconductor devices that enable wireless connectivity, such as transceivers, amplifiers, and filters. These tests ensure that the devices can handle the high-frequency signals and data rates required for modern wireless communication standards. In RF Circuit applications, probe cards are essential for evaluating the performance of radio frequency circuits, which are used in a wide range of applications, from mobile phones to satellite communications. The precise testing capabilities of probe cards help ensure that these circuits meet the stringent performance requirements for signal integrity and power efficiency. Microwave Measurement involves testing semiconductor devices that operate at microwave frequencies, such as radar systems and microwave communication equipment. Probe cards used in this area must be capable of handling the high frequencies and power levels associated with microwave signals. Signal Transmission testing focuses on evaluating the performance of semiconductor devices that transmit and receive signals, such as data converters and communication transceivers. Probe cards play a crucial role in ensuring that these devices can accurately and reliably transmit signals over various distances and through different media. Other applications of probe cards in the wafer testing market include testing semiconductor devices used in automotive electronics, industrial automation, and consumer electronics. In each of these areas, probe cards help ensure that the devices meet the required performance standards and are free from defects, contributing to the overall quality and reliability of the final products.

Global Probe Card for Wafer Testing Market Outlook:

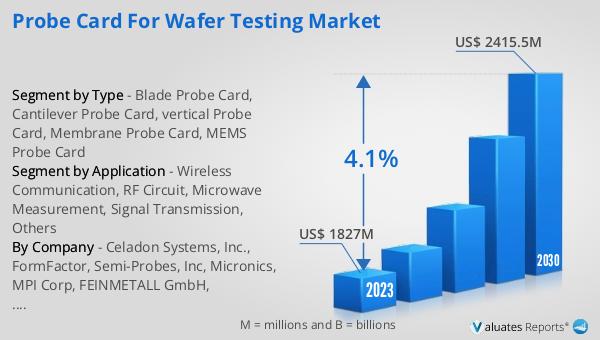

The global Probe Card for Wafer Testing market was valued at US$ 1827 million in 2023 and is anticipated to reach US$ 2415.5 million by 2030, witnessing a CAGR of 4.1% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing importance of probe cards in the semiconductor industry. The projected growth in market value reflects the rising demand for advanced semiconductor devices across various sectors, including consumer electronics, automotive, telecommunications, and industrial applications. As technology continues to evolve, the complexity and performance requirements of semiconductor devices are also increasing, driving the need for more sophisticated and reliable testing solutions. Probe cards play a crucial role in this process by enabling precise and efficient testing of semiconductor wafers, ensuring that the final products meet the required quality and performance standards. The anticipated growth in the probe card market underscores the ongoing advancements in semiconductor technology and the critical role of testing in the manufacturing process.

| Report Metric | Details |

| Report Name | Probe Card for Wafer Testing Market |

| Accounted market size in 2023 | US$ 1827 million |

| Forecasted market size in 2030 | US$ 2415.5 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Celadon Systems, Inc., FormFactor, Semi-Probes, Inc, Micronics, MPI Corp, FEINMETALL GmbH, Technoprobe, Probe Technology UK, FICT LIMITED, Translarity, ProbeLogic, STAr Technologies, Alpha Probes, CHPT, Jenoptik, BE Precision Technology, Leeno Industrial Inc, Will Technology, MaxOne, SV Probe |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |