What is Global Camping Power Bank Market?

The Global Camping Power Bank Market refers to the industry focused on the production and distribution of portable power banks specifically designed for camping and outdoor activities. These power banks are essential for campers, hikers, and outdoor enthusiasts who need to charge their electronic devices, such as smartphones, GPS units, cameras, and other gadgets, while away from traditional power sources. The market encompasses a wide range of products with varying capacities, features, and technologies to meet the diverse needs of users. These power banks are typically rugged, weather-resistant, and equipped with multiple charging ports to accommodate different devices. The growing popularity of outdoor activities and the increasing reliance on electronic devices have driven the demand for camping power banks, making it a significant segment within the broader portable power bank market. Manufacturers in this market are continually innovating to offer more efficient, durable, and user-friendly products to cater to the evolving needs of outdoor enthusiasts.

Lithium Cobalt Oxide (LiCoO2), Nickel Cobalt Manganese (LiNiCoMnO2), Lithium Iron Phosphate (LiFePO4) in the Global Camping Power Bank Market:

Lithium Cobalt Oxide (LiCoO2), Nickel Cobalt Manganese (LiNiCoMnO2), and Lithium Iron Phosphate (LiFePO4) are three prominent types of lithium-ion batteries used in the Global Camping Power Bank Market. Each of these battery chemistries has unique characteristics that make them suitable for different applications and user preferences. Lithium Cobalt Oxide (LiCoO2) batteries are known for their high energy density, which means they can store a large amount of energy in a relatively small and lightweight package. This makes them ideal for power banks that need to be portable and easy to carry during camping trips. However, LiCoO2 batteries can be more expensive and have a shorter lifespan compared to other types. Nickel Cobalt Manganese (LiNiCoMnO2) batteries, on the other hand, offer a good balance between energy density, safety, and cost. They are more stable and safer than LiCoO2 batteries, making them a popular choice for camping power banks that need to withstand various environmental conditions. Additionally, LiNiCoMnO2 batteries have a longer lifespan, which is beneficial for users who require a reliable power source for extended outdoor activities. Lithium Iron Phosphate (LiFePO4) batteries are known for their excellent thermal stability and safety. They have a lower energy density compared to LiCoO2 and LiNiCoMnO2 batteries, but they are highly durable and can withstand extreme temperatures and rough handling. This makes LiFePO4 batteries an excellent choice for rugged camping power banks that need to perform reliably in harsh outdoor environments. Furthermore, LiFePO4 batteries have a longer cycle life, meaning they can be charged and discharged many times without significant degradation, providing long-term value to users. In summary, the choice of battery chemistry in the Global Camping Power Bank Market depends on the specific needs and preferences of users. LiCoO2 batteries are suitable for those who prioritize high energy density and portability, while LiNiCoMnO2 batteries offer a good balance of performance, safety, and cost. LiFePO4 batteries are ideal for users who require maximum durability and safety in challenging outdoor conditions. Manufacturers in the camping power bank market continue to innovate and optimize these battery technologies to provide the best possible solutions for outdoor enthusiasts.

Personal Use, Commercial, Others in the Global Camping Power Bank Market:

The Global Camping Power Bank Market serves a wide range of applications, including personal use, commercial use, and other specialized areas. For personal use, camping power banks are essential for individuals who enjoy outdoor activities such as camping, hiking, fishing, and backpacking. These power banks provide a reliable source of power for charging smartphones, tablets, cameras, GPS devices, and other portable electronics, ensuring that users can stay connected and capture their adventures even in remote locations. The convenience and portability of camping power banks make them a must-have accessory for outdoor enthusiasts who need to keep their devices powered up during their trips. In the commercial sector, camping power banks are used by businesses and organizations that operate in outdoor environments. For example, outdoor adventure tour companies, camping gear rental services, and event organizers often rely on camping power banks to provide power solutions for their clients and staff. These power banks enable businesses to offer a better experience to their customers by ensuring that their electronic devices remain charged and functional throughout their outdoor activities. Additionally, camping power banks are used by professionals such as photographers, researchers, and field workers who need a dependable power source for their equipment while working in remote or off-grid locations. Other specialized areas where camping power banks are used include emergency preparedness and disaster relief. In emergency situations, having a reliable power source can be crucial for communication, navigation, and accessing important information. Camping power banks can be a valuable addition to emergency kits, providing a portable and dependable power solution for charging essential devices during power outages or natural disasters. Furthermore, camping power banks are used in recreational vehicles (RVs) and boats, where access to traditional power sources may be limited. These power banks offer a convenient way to keep electronic devices charged while on the move, enhancing the overall experience for travelers and outdoor enthusiasts. In summary, the Global Camping Power Bank Market caters to a diverse range of applications, from personal use by outdoor enthusiasts to commercial use by businesses and professionals, as well as specialized areas such as emergency preparedness and recreational vehicles. The versatility and reliability of camping power banks make them an indispensable tool for anyone who needs a portable power solution in outdoor and off-grid environments.

Global Camping Power Bank Market Outlook:

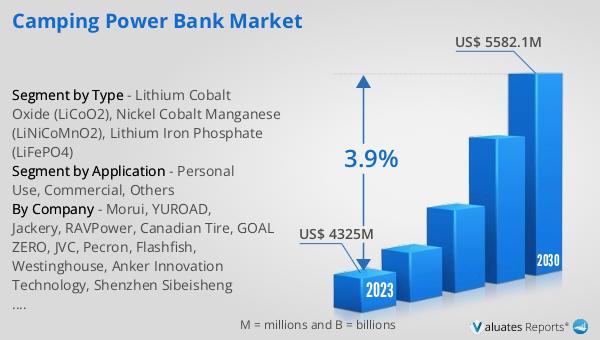

The global Camping Power Bank market was valued at US$ 4325 million in 2023 and is anticipated to reach US$ 5582.1 million by 2030, witnessing a CAGR of 3.9% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for portable power solutions among outdoor enthusiasts and professionals. The rising popularity of outdoor activities such as camping, hiking, and adventure sports has fueled the need for reliable power sources to keep electronic devices charged and functional in remote locations. Additionally, advancements in battery technology and the development of more efficient and durable power banks have contributed to the market's growth. Manufacturers are focusing on creating innovative products that cater to the specific needs of outdoor users, such as rugged and weather-resistant designs, multiple charging ports, and high-capacity batteries. The growing awareness of the importance of staying connected and powered up during outdoor activities has further boosted the demand for camping power banks. As a result, the market is expected to continue its upward trend, providing ample opportunities for manufacturers and stakeholders to capitalize on the increasing demand for portable power solutions in the coming years.

| Report Metric | Details |

| Report Name | Camping Power Bank Market |

| Accounted market size in 2023 | US$ 4325 million |

| Forecasted market size in 2030 | US$ 5582.1 million |

| CAGR | 3.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Morui, YUROAD, Jackery, RAVPower, Canadian Tire, GOAL ZERO, JVC, Pecron, Flashfish, Westinghouse, Anker Innovation Technology, Shenzhen Sibeisheng Electronic Technology Co., Ltd., Shenzhen Zhenghao Innovation Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |