What is Global Glass Fiber Reinforced Plastic and Carbon Fiber Reinforced Plastic Market?

Global Glass Fiber Reinforced Plastic (GFRP) and Carbon Fiber Reinforced Plastic (CFRP) markets are pivotal in the modern materials industry. These materials are composites, meaning they are made by combining two or more different substances to create a new material with superior properties. GFRP is made by reinforcing plastic with glass fibers, which enhances its strength and durability while keeping it lightweight. Similarly, CFRP is created by reinforcing plastic with carbon fibers, resulting in a material that is even stronger and lighter than GFRP. These advanced materials are used in various industries due to their exceptional strength-to-weight ratios, corrosion resistance, and versatility. The global market for these composites is expanding rapidly as industries seek materials that offer high performance and efficiency. The demand for GFRP and CFRP is driven by their applications in sectors such as automotive, aerospace, consumer electronics, and more, where the need for lightweight, strong, and durable materials is paramount.

Glass Fiber Reinforced Plastic, Carbon Fiber Reinforced Plastic in the Global Glass Fiber Reinforced Plastic and Carbon Fiber Reinforced Plastic Market:

Glass Fiber Reinforced Plastic (GFRP) and Carbon Fiber Reinforced Plastic (CFRP) are two of the most significant advancements in material science. GFRP is composed of a polymer matrix reinforced with glass fibers, which provides a combination of high strength, low weight, and resistance to environmental factors such as corrosion and UV radiation. This makes GFRP an ideal material for applications where durability and longevity are crucial. On the other hand, CFRP is made by embedding carbon fibers within a polymer matrix. Carbon fibers are known for their exceptional strength and stiffness, which translates to CFRP being incredibly strong yet lightweight. This makes CFRP a preferred choice in industries where weight reduction is critical without compromising on strength, such as in aerospace and high-performance automotive sectors. Both GFRP and CFRP are used extensively in manufacturing due to their ability to be molded into complex shapes, which allows for innovative design and engineering solutions. The global market for these materials is growing as industries continue to seek out advanced materials that can meet the demands of modern engineering challenges. The versatility, strength, and lightweight nature of GFRP and CFRP make them indispensable in the development of next-generation products and technologies.

Automobile, Aerospace, Consumer Electronics, Others in the Global Glass Fiber Reinforced Plastic and Carbon Fiber Reinforced Plastic Market:

The usage of Global Glass Fiber Reinforced Plastic (GFRP) and Carbon Fiber Reinforced Plastic (CFRP) spans several key industries, each benefiting from the unique properties of these advanced materials. In the automobile industry, GFRP and CFRP are used to manufacture various components such as body panels, chassis, and interior parts. The lightweight nature of these materials helps in reducing the overall weight of vehicles, which in turn improves fuel efficiency and reduces emissions. Additionally, the high strength and durability of GFRP and CFRP enhance the safety and longevity of automotive components. In the aerospace industry, the demand for lightweight and strong materials is even more critical. GFRP and CFRP are used in the construction of aircraft structures, including fuselage, wings, and tail sections. The use of these materials helps in reducing the weight of the aircraft, leading to better fuel efficiency and increased payload capacity. Moreover, the high strength-to-weight ratio of GFRP and CFRP ensures that the aircraft can withstand the extreme conditions of flight. In the consumer electronics sector, GFRP and CFRP are used in the production of lightweight and durable casings for devices such as smartphones, laptops, and tablets. The use of these materials not only enhances the aesthetic appeal of the devices but also improves their durability and resistance to impact. Other industries, such as sports equipment, construction, and renewable energy, also benefit from the unique properties of GFRP and CFRP. For instance, in the construction industry, GFRP is used to reinforce concrete structures, providing additional strength and durability. In the renewable energy sector, CFRP is used in the manufacturing of wind turbine blades, where its lightweight and high strength properties are crucial for efficient energy generation. Overall, the versatility and superior properties of GFRP and CFRP make them essential materials in various industries, driving their demand and growth in the global market.

Global Glass Fiber Reinforced Plastic and Carbon Fiber Reinforced Plastic Market Outlook:

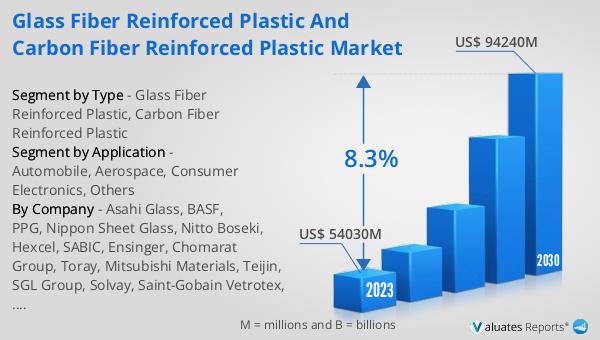

The global market for Glass Fiber Reinforced Plastic (GFRP) and Carbon Fiber Reinforced Plastic (CFRP) has shown significant growth in recent years. In 2023, the market was valued at approximately US$ 54,030 million. This substantial market size reflects the increasing demand for these advanced materials across various industries. Looking ahead, the market is anticipated to reach around US$ 94,240 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 8.3% during the forecast period from 2024 to 2030. The robust growth rate underscores the expanding applications and rising adoption of GFRP and CFRP in sectors such as automotive, aerospace, consumer electronics, and more. The increasing focus on lightweight, durable, and high-performance materials is driving the demand for GFRP and CFRP, as industries seek to enhance efficiency, reduce emissions, and improve overall product performance. The market outlook for GFRP and CFRP is promising, with continuous advancements in material science and engineering further propelling their adoption and integration into various applications.

| Report Metric | Details |

| Report Name | Glass Fiber Reinforced Plastic and Carbon Fiber Reinforced Plastic Market |

| Accounted market size in 2023 | US$ 54030 million |

| Forecasted market size in 2030 | US$ 94240 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Asahi Glass, BASF, PPG, Nippon Sheet Glass, Nitto Boseki, Hexcel, SABIC, Ensinger, Chomarat Group, Toray, Mitsubishi Materials, Teijin, SGL Group, Solvay, Saint-Gobain Vetrotex, DowAksa, Taishan Fiberglass |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |