What is Global Oxygen Measuring Probe Market?

The Global Oxygen Measuring Probe Market refers to the worldwide industry focused on the production, distribution, and utilization of devices designed to measure the concentration of oxygen in various environments. These probes are essential in numerous applications, including industrial processes, medical settings, automotive systems, and environmental monitoring. They help ensure safety, optimize performance, and maintain regulatory compliance by providing accurate and real-time oxygen level readings. The market encompasses a wide range of products, from simple handheld devices to sophisticated, integrated systems used in complex industrial operations. The demand for oxygen measuring probes is driven by the need for precise oxygen monitoring in critical applications, advancements in sensor technology, and increasing awareness of environmental and safety standards. As industries continue to evolve and prioritize efficiency and safety, the global market for oxygen measuring probes is expected to grow, offering innovative solutions to meet diverse needs.

Diversion Type, Direct Plug-in in the Global Oxygen Measuring Probe Market:

Diversion Type and Direct Plug-in are two primary categories within the Global Oxygen Measuring Probe Market, each serving distinct purposes and applications. Diversion Type oxygen measuring probes are typically used in scenarios where the gas sample needs to be diverted from the main flow for analysis. These probes are often employed in industrial processes where continuous monitoring of oxygen levels is crucial for maintaining optimal conditions and ensuring safety. They are designed to handle high-pressure environments and can be integrated into complex systems to provide real-time data. On the other hand, Direct Plug-in oxygen measuring probes are designed for direct insertion into the gas stream. These probes are commonly used in applications where immediate and direct measurement of oxygen levels is required, such as in automotive exhaust systems or medical respiratory equipment. Direct Plug-in probes are known for their ease of installation and maintenance, making them a popular choice in various industries. Both types of probes utilize advanced sensor technologies, such as zirconia or electrochemical sensors, to provide accurate and reliable oxygen measurements. The choice between Diversion Type and Direct Plug-in probes depends on the specific requirements of the application, including factors like the environment, pressure conditions, and the need for continuous versus spot measurements. As technology advances, both types of probes are becoming more sophisticated, offering enhanced features like digital interfaces, wireless connectivity, and improved durability. This evolution is driven by the increasing demand for precise oxygen monitoring in critical applications, as well as the need for more efficient and user-friendly solutions. The Global Oxygen Measuring Probe Market continues to innovate, providing a wide range of options to meet the diverse needs of industries worldwide.

Automotive, Industry, Medical, Petrochemical, Others in the Global Oxygen Measuring Probe Market:

The usage of Global Oxygen Measuring Probes spans across various sectors, including Automotive, Industry, Medical, Petrochemical, and others, each with unique requirements and applications. In the Automotive sector, oxygen measuring probes are crucial for monitoring and controlling the oxygen levels in exhaust gases. This helps in optimizing the combustion process, reducing emissions, and ensuring compliance with environmental regulations. These probes are integral to the functioning of modern vehicles, contributing to improved fuel efficiency and reduced environmental impact. In the Industrial sector, oxygen measuring probes are used in processes such as combustion control, fermentation, and chemical production. Accurate oxygen measurement is essential for maintaining optimal conditions, ensuring safety, and enhancing process efficiency. These probes help in preventing hazardous situations, such as explosions or the formation of toxic gases, by providing real-time data on oxygen levels. In the Medical field, oxygen measuring probes are used in respiratory equipment, anesthesia machines, and patient monitoring systems. They play a critical role in ensuring that patients receive the correct amount of oxygen, which is vital for their health and recovery. These probes are designed to provide precise and reliable measurements, even in challenging conditions. In the Petrochemical industry, oxygen measuring probes are used to monitor oxygen levels in various processes, such as refining, gas processing, and chemical production. Accurate oxygen measurement is crucial for maintaining process efficiency, ensuring safety, and preventing equipment damage. These probes help in optimizing the production process, reducing costs, and ensuring compliance with industry standards. Other sectors that utilize oxygen measuring probes include environmental monitoring, food and beverage production, and research laboratories. In environmental monitoring, these probes are used to measure oxygen levels in air and water, helping to assess pollution levels and ensure compliance with environmental regulations. In food and beverage production, oxygen measuring probes are used to monitor oxygen levels during fermentation and packaging processes, ensuring product quality and safety. In research laboratories, these probes are used in various experiments and studies to measure oxygen levels accurately. The versatility and reliability of oxygen measuring probes make them indispensable tools in a wide range of applications, contributing to improved efficiency, safety, and compliance across various industries.

Global Oxygen Measuring Probe Market Outlook:

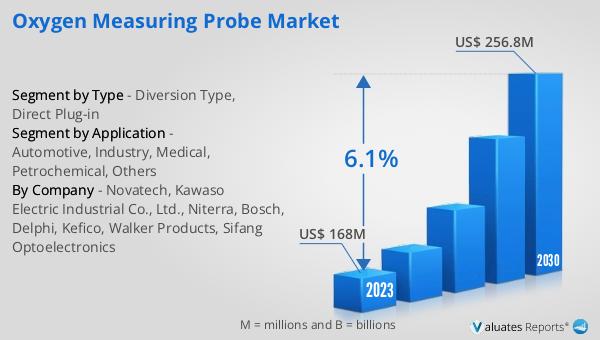

The global Oxygen Measuring Probe market, valued at US$ 168 million in 2023, is projected to grow significantly, reaching an estimated value of US$ 256.8 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 6.1% during the forecast period from 2024 to 2030. The increasing demand for accurate and reliable oxygen measurement across various industries is a key driver of this market expansion. Industries such as automotive, medical, industrial, and petrochemical are increasingly relying on oxygen measuring probes to ensure safety, optimize processes, and comply with stringent regulatory standards. The advancements in sensor technology, coupled with the growing awareness of environmental and safety concerns, are further propelling the market growth. As industries continue to evolve and prioritize efficiency and safety, the demand for innovative and high-performance oxygen measuring probes is expected to rise. This market outlook highlights the significant potential for growth and innovation in the global Oxygen Measuring Probe market, driven by the need for precise oxygen monitoring in critical applications.

| Report Metric | Details |

| Report Name | Oxygen Measuring Probe Market |

| Accounted market size in 2023 | US$ 168 million |

| Forecasted market size in 2030 | US$ 256.8 million |

| CAGR | 6.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Novatech, Kawaso Electric Industrial Co., Ltd., Niterra, Bosch, Delphi, Kefico, Walker Products, Sifang Optoelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |