What is Global Construction Waterproof Membrane Market?

The Global Construction Waterproof Membrane Market refers to the industry focused on the production and application of waterproof membranes used in construction projects worldwide. These membranes are essential for protecting buildings and structures from water infiltration, which can cause significant damage over time. Waterproof membranes are used in various applications, including roofing, walls, basements, and foundations, to ensure that water does not penetrate the structure. The market encompasses a wide range of materials and technologies designed to provide effective waterproofing solutions. With the increasing demand for durable and long-lasting construction materials, the global construction waterproof membrane market has seen substantial growth. This growth is driven by factors such as urbanization, infrastructure development, and the need for sustainable building practices. As a result, the market continues to evolve, offering innovative products that cater to the diverse needs of the construction industry.

Asphalt Waterproofing Membrane, PVC Waterproof Membrane, Polypropylene Waterproof Membrane, TPO Waterproof Membrane, EPDM Waterproof Membrane, Others in the Global Construction Waterproof Membrane Market:

Asphalt waterproofing membranes are one of the most commonly used materials in the global construction waterproof membrane market. These membranes are made from bitumen, a sticky, black, and highly viscous liquid or semi-solid form of petroleum. Asphalt membranes are known for their durability, flexibility, and resistance to water and weathering, making them ideal for roofing applications. PVC (Polyvinyl Chloride) waterproof membranes are another popular choice, known for their excellent chemical resistance, flexibility, and ease of installation. These membranes are often used in roofing, tunnels, and underground structures. Polypropylene waterproof membranes are made from a thermoplastic polymer and are known for their high tensile strength, resistance to chemicals, and UV stability. They are commonly used in roofing, foundations, and tunnels. TPO (Thermoplastic Olefin) waterproof membranes are a blend of polypropylene and ethylene-propylene rubber, offering excellent resistance to UV radiation, chemicals, and punctures. These membranes are widely used in roofing applications due to their energy efficiency and ease of installation. EPDM (Ethylene Propylene Diene Monomer) waterproof membranes are made from synthetic rubber and are known for their exceptional durability, flexibility, and resistance to extreme weather conditions. They are commonly used in roofing, pond liners, and underground structures. Other types of waterproof membranes include liquid-applied membranes, which are applied as a liquid and then cured to form a seamless, waterproof barrier, and self-adhesive membranes, which have a sticky backing that allows them to be easily applied to surfaces. Each type of waterproof membrane has its unique properties and advantages, making them suitable for different applications in the construction industry.

Residential Building, Commercial Building, Industrial Building in the Global Construction Waterproof Membrane Market:

The usage of global construction waterproof membranes spans across various types of buildings, including residential, commercial, and industrial structures. In residential buildings, waterproof membranes are crucial for protecting homes from water damage, which can lead to mold growth, structural damage, and other issues. These membranes are commonly used in roofing, basements, and bathrooms to ensure that water does not penetrate the building envelope. In commercial buildings, waterproof membranes play a vital role in maintaining the integrity of the structure and protecting valuable assets. These membranes are used in roofing, walls, and foundations to prevent water infiltration and ensure the longevity of the building. Commercial buildings, such as office complexes, shopping malls, and hotels, require reliable waterproofing solutions to protect against water damage and maintain a safe and comfortable environment for occupants. In industrial buildings, waterproof membranes are essential for protecting machinery, equipment, and other valuable assets from water damage. These membranes are used in roofing, walls, and floors to prevent water infiltration and ensure the smooth operation of industrial processes. Industrial buildings, such as factories, warehouses, and power plants, require robust waterproofing solutions to withstand harsh environmental conditions and ensure the safety and efficiency of operations. Overall, the usage of waterproof membranes in residential, commercial, and industrial buildings is critical for ensuring the durability, safety, and longevity of structures. With the increasing demand for sustainable and resilient building practices, the global construction waterproof membrane market continues to grow, offering innovative solutions to meet the diverse needs of the construction industry.

Global Construction Waterproof Membrane Market Outlook:

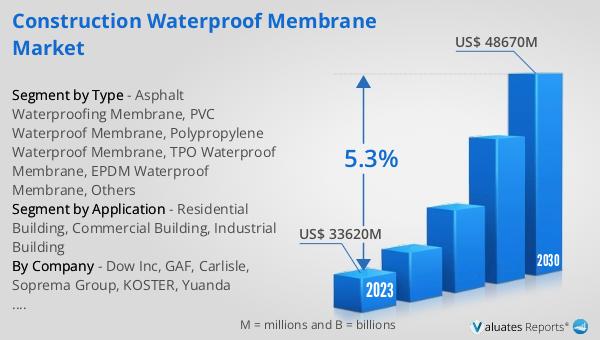

The global construction waterproof membrane market was valued at US$ 33,620 million in 2023 and is anticipated to reach US$ 48,670 million by 2030, witnessing a CAGR of 5.3% during the forecast period from 2024 to 2030. This significant growth is driven by the increasing demand for durable and long-lasting construction materials, as well as the need for effective waterproofing solutions in various applications. The market's expansion is also fueled by factors such as urbanization, infrastructure development, and the adoption of sustainable building practices. As the construction industry continues to evolve, the demand for high-quality waterproof membranes is expected to rise, providing ample opportunities for market players to innovate and expand their product offerings. The projected growth of the global construction waterproof membrane market highlights the importance of these materials in ensuring the durability and longevity of buildings and structures worldwide.

| Report Metric | Details |

| Report Name | Construction Waterproof Membrane Market |

| Accounted market size in 2023 | US$ 33620 million |

| Forecasted market size in 2030 | US$ 48670 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dow Inc, GAF, Carlisle, Soprema Group, KOSTER, Yuanda Hongyu, Versico, CKS, Shouguang Fada Cloth, Hubei Unibon, Milliken & Company, Johns Manville, Tiandingfeng(TDF), Incorporated, CHRYSO SAS, Nan Pao Resins Chemical, Hebei Qianjin, Bautex, Hongyuan Waterproof, Green Shield, RDEX Group, Imperbit Membrane, Fosroc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |