What is Global Ultrasonic Diagnostic Imaging System Market?

The Global Ultrasonic Diagnostic Imaging System Market refers to the worldwide industry focused on the development, production, and distribution of ultrasonic diagnostic imaging systems. These systems utilize high-frequency sound waves to create images of the inside of the body, which are then used by healthcare professionals to diagnose and monitor various medical conditions. The market encompasses a wide range of products, including portable and stationary ultrasound machines, as well as various types of ultrasound imaging technologies such as 2D, 3D, and Doppler ultrasound. The demand for these systems is driven by factors such as the increasing prevalence of chronic diseases, advancements in ultrasound technology, and the growing need for non-invasive diagnostic procedures. The market is also influenced by regulatory policies, healthcare infrastructure, and the availability of skilled professionals to operate these systems. Overall, the Global Ultrasonic Diagnostic Imaging System Market plays a crucial role in modern healthcare by providing essential tools for accurate and timely medical diagnosis.

Black and White Ultrasound Imaging System, Color Doppler Ultrasound Imaging System in the Global Ultrasonic Diagnostic Imaging System Market:

The Global Ultrasonic Diagnostic Imaging System Market includes various types of ultrasound imaging systems, with Black and White Ultrasound Imaging Systems and Color Doppler Ultrasound Imaging Systems being two of the most prominent categories. Black and White Ultrasound Imaging Systems, also known as grayscale ultrasound, are the traditional form of ultrasound imaging. They produce images in shades of gray, which are used to visualize the internal structures of the body. These systems are widely used for general diagnostic purposes, including obstetrics, gynecology, cardiology, and abdominal imaging. They are valued for their simplicity, cost-effectiveness, and reliability. On the other hand, Color Doppler Ultrasound Imaging Systems represent a more advanced technology. These systems not only provide grayscale images but also incorporate color to visualize blood flow within the body. The color Doppler technology allows healthcare professionals to assess the direction and velocity of blood flow, which is crucial for diagnosing vascular conditions, heart diseases, and other circulatory issues. The ability to visualize blood flow in real-time enhances the diagnostic capabilities of ultrasound imaging, making Color Doppler systems particularly valuable in cardiology and vascular medicine. Both types of ultrasound imaging systems have their unique advantages and applications, contributing to the overall growth and diversification of the Global Ultrasonic Diagnostic Imaging System Market. The continuous advancements in ultrasound technology, such as the development of 3D and 4D imaging, further expand the potential uses and benefits of these systems. As a result, healthcare providers have a wide range of options to choose from, depending on their specific diagnostic needs and budget constraints. The integration of artificial intelligence and machine learning in ultrasound imaging is also an emerging trend, promising to enhance image quality, improve diagnostic accuracy, and streamline workflow in clinical settings. Overall, the Global Ultrasonic Diagnostic Imaging System Market is characterized by a dynamic and evolving landscape, driven by technological innovations and the increasing demand for high-quality diagnostic tools.

Hospital, Clinic in the Global Ultrasonic Diagnostic Imaging System Market:

The usage of Global Ultrasonic Diagnostic Imaging Systems in hospitals and clinics is extensive and multifaceted, reflecting the versatility and importance of these diagnostic tools in modern healthcare. In hospitals, ultrasonic diagnostic imaging systems are integral to various departments, including radiology, cardiology, obstetrics and gynecology, and emergency medicine. In radiology, these systems are used for general imaging purposes, such as examining the abdomen, pelvis, and other soft tissues. They help in identifying abnormalities, guiding biopsies, and monitoring the progress of treatments. In cardiology, ultrasound systems, particularly those with Doppler capabilities, are essential for evaluating heart function, detecting heart diseases, and assessing blood flow. Obstetrics and gynecology departments rely heavily on ultrasound imaging for monitoring fetal development, diagnosing pregnancy-related conditions, and examining the female reproductive system. In emergency medicine, portable ultrasound machines are invaluable for rapid assessment of trauma patients, detecting internal bleeding, and guiding emergency procedures. Clinics, on the other hand, benefit from the portability and ease of use of ultrasonic diagnostic imaging systems. These systems enable primary care physicians, specialists, and other healthcare providers to perform quick and accurate diagnostic assessments without the need for extensive infrastructure. In outpatient settings, ultrasound imaging is commonly used for routine check-ups, prenatal care, and the evaluation of various medical conditions. The non-invasive nature of ultrasound makes it a preferred choice for patients, as it reduces discomfort and eliminates the risks associated with radiation exposure. Additionally, the real-time imaging capabilities of ultrasound systems allow for immediate diagnosis and decision-making, enhancing the efficiency and effectiveness of clinical care. The widespread adoption of ultrasonic diagnostic imaging systems in both hospitals and clinics underscores their critical role in improving patient outcomes, reducing healthcare costs, and enhancing the overall quality of care.

Global Ultrasonic Diagnostic Imaging System Market Outlook:

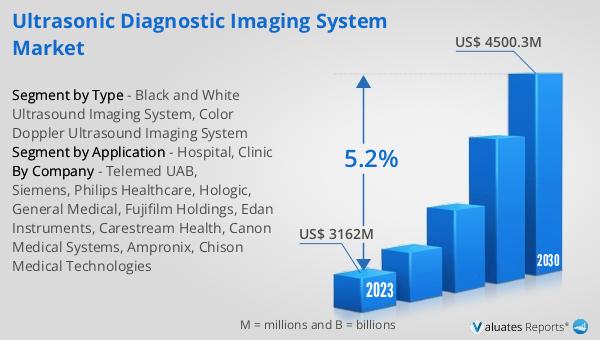

The global Ultrasonic Diagnostic Imaging System market was valued at US$ 3162 million in 2023 and is anticipated to reach US$ 4500.3 million by 2030, witnessing a CAGR of 5.2% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the ultrasonic diagnostic imaging system market over the coming years. The increasing demand for non-invasive diagnostic tools, coupled with advancements in ultrasound technology, is expected to drive this growth. The market's expansion is also supported by the rising prevalence of chronic diseases, the aging population, and the growing emphasis on early diagnosis and preventive healthcare. As healthcare providers continue to adopt advanced imaging systems to enhance diagnostic accuracy and patient care, the ultrasonic diagnostic imaging system market is poised for substantial growth. The projected increase in market value reflects the ongoing investments in research and development, as well as the continuous efforts to improve the accessibility and affordability of ultrasound imaging systems. Overall, the market outlook indicates a promising future for the global ultrasonic diagnostic imaging system market, with significant opportunities for innovation and growth.

| Report Metric | Details |

| Report Name | Ultrasonic Diagnostic Imaging System Market |

| Accounted market size in 2023 | US$ 3162 million |

| Forecasted market size in 2030 | US$ 4500.3 million |

| CAGR | 5.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Telemed UAB, Siemens, Philips Healthcare, Hologic, General Medical, Fujifilm Holdings, Edan Instruments, Carestream Health, Canon Medical Systems, Ampronix, Chison Medical Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |