What is Global Liver Transplant Anti-Rejection Drugs Market?

The Global Liver Transplant Anti-Rejection Drugs Market refers to the market for medications specifically designed to prevent the rejection of transplanted livers by the recipient's immune system. When a person undergoes a liver transplant, their immune system may recognize the new liver as a foreign object and attempt to attack it. Anti-rejection drugs, also known as immunosuppressants, are used to suppress this immune response, thereby increasing the chances of the transplant being successful. These drugs are crucial for the long-term survival and health of liver transplant recipients. The market for these drugs includes various types of medications, such as glucocorticoids, anti-proliferative drugs, and T cell-mediated immunosuppressants, each playing a unique role in preventing organ rejection. The demand for these drugs is driven by the increasing number of liver transplant surgeries worldwide, advancements in medical technology, and the growing awareness about organ transplantation. The market is also influenced by factors such as regulatory approvals, healthcare infrastructure, and the availability of generic versions of these drugs.

Glucocorticoids, Anti-Proliferative Drugs, T Cell Mediated Immunosuppressants in the Global Liver Transplant Anti-Rejection Drugs Market:

Glucocorticoids, anti-proliferative drugs, and T cell-mediated immunosuppressants are three major categories of medications used in the Global Liver Transplant Anti-Rejection Drugs Market. Glucocorticoids, such as prednisone and methylprednisolone, are steroids that help reduce inflammation and suppress the immune system. They are often used immediately after the transplant surgery to prevent acute rejection. These drugs work by inhibiting the activity of various immune cells and cytokines, thereby reducing the immune response against the transplanted liver. However, long-term use of glucocorticoids can lead to side effects such as weight gain, osteoporosis, and increased risk of infections. Anti-proliferative drugs, such as mycophenolate mofetil (CellCept) and azathioprine (Imuran), work by inhibiting the proliferation of T and B lymphocytes, which are key players in the immune response. These drugs are often used in combination with other immunosuppressants to provide a more comprehensive approach to preventing organ rejection. Anti-proliferative drugs are generally well-tolerated, but they can cause side effects such as gastrointestinal issues, bone marrow suppression, and increased risk of infections. T cell-mediated immunosuppressants, such as cyclosporine (Neoral, Sandimmune) and tacrolimus (Prograf), specifically target T cells, which are crucial for initiating and sustaining the immune response against the transplanted liver. These drugs work by inhibiting the activity of calcineurin, a protein that is essential for T cell activation. By blocking this pathway, T cell-mediated immunosuppressants effectively reduce the risk of organ rejection. These drugs are considered the cornerstone of immunosuppressive therapy in liver transplant patients and are often used in combination with glucocorticoids and anti-proliferative drugs. However, they can cause side effects such as nephrotoxicity, hypertension, and neurotoxicity. The choice of immunosuppressive regimen depends on various factors, including the patient's medical history, the type of liver transplant, and the presence of any comorbid conditions. The goal is to achieve a balance between preventing organ rejection and minimizing the side effects of the medications.

Hospital, Pharmacy, Online Sales, Medical Institutions in the Global Liver Transplant Anti-Rejection Drugs Market:

The usage of Global Liver Transplant Anti-Rejection Drugs Market spans across various areas such as hospitals, pharmacies, online sales, and medical institutions. In hospitals, these drugs are primarily used in the immediate post-transplant period to prevent acute rejection. The hospital setting allows for close monitoring of the patient's response to the medication and the management of any side effects. Hospitals often have specialized transplant units with healthcare professionals who are experienced in managing immunosuppressive therapy. This ensures that the patient receives the appropriate dosage and combination of drugs to prevent organ rejection. In pharmacies, liver transplant anti-rejection drugs are dispensed to patients for long-term use. Pharmacists play a crucial role in educating patients about the importance of adhering to their medication regimen and managing any side effects. They also provide information on drug interactions and the proper storage of medications. Community pharmacies make these drugs accessible to patients who may not have easy access to hospital-based care. Online sales of liver transplant anti-rejection drugs have become increasingly popular, especially in regions with limited access to healthcare facilities. Online pharmacies offer the convenience of home delivery and often provide a wider range of medications, including generic versions. However, it is important for patients to ensure that they are purchasing from reputable sources to avoid counterfeit or substandard drugs. Medical institutions, such as transplant centers and specialized clinics, play a critical role in the ongoing management of liver transplant patients. These institutions often have multidisciplinary teams that include transplant surgeons, hepatologists, immunologists, and pharmacists who work together to develop individualized treatment plans. They also conduct regular follow-up visits to monitor the patient's liver function, adjust medication dosages, and manage any complications. In addition to providing clinical care, medical institutions are involved in research and clinical trials to develop new and more effective immunosuppressive therapies. They also play a key role in educating healthcare professionals and patients about the latest advancements in liver transplantation and immunosuppressive therapy. Overall, the usage of liver transplant anti-rejection drugs in these various settings ensures that patients receive comprehensive care and support throughout their transplant journey.

Global Liver Transplant Anti-Rejection Drugs Market Outlook:

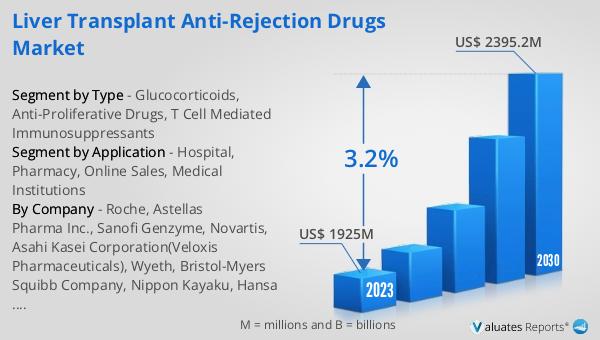

The global Liver Transplant Anti-Rejection Drugs market was valued at US$ 1925 million in 2023 and is anticipated to reach US$ 2395.2 million by 2030, witnessing a CAGR of 3.2% during the forecast period 2024-2030. This indicates a steady growth in the demand for these essential medications, driven by factors such as the increasing number of liver transplant surgeries, advancements in medical technology, and the growing awareness about organ transplantation. The market's growth is also influenced by regulatory approvals, healthcare infrastructure, and the availability of generic versions of these drugs. As the number of liver transplant recipients continues to rise, the need for effective and safe anti-rejection drugs becomes even more critical. The market is expected to see continued innovation and development of new immunosuppressive therapies that offer better efficacy and fewer side effects. This growth trajectory underscores the importance of liver transplant anti-rejection drugs in ensuring the long-term success of liver transplants and improving the quality of life for transplant recipients.

| Report Metric | Details |

| Report Name | Liver Transplant Anti-Rejection Drugs Market |

| Accounted market size in 2023 | US$ 1925 million |

| Forecasted market size in 2030 | US$ 2395.2 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Roche, Astellas Pharma Inc., Sanofi Genzyme, Novartis, Asahi Kasei Corporation(Veloxis Pharmaceuticals), Wyeth, Bristol-Myers Squibb Company, Nippon Kayaku, Hansa Biopharma, GSK, AbbVie, Huadong Medicine, North China Pharmaceutical Group, Beijing SL Pharmaceutical, Livzon Pharm, Ruibang Pharmaceutical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |