What is Global ACQ Wood Preservative Market?

The Global ACQ Wood Preservative Market refers to the worldwide industry focused on the production, distribution, and application of Alkaline Copper Quaternary (ACQ) wood preservatives. ACQ is a water-based wood preservative that is widely used to protect wood from decay, fungi, and insect damage. This market encompasses various types of ACQ formulations, including ACQ-A, ACQ-B, ACQ-C, and ACQ-D, each with specific properties and applications. The demand for ACQ wood preservatives is driven by their effectiveness, environmental friendliness, and compliance with stringent regulations on the use of traditional wood preservatives containing arsenic and chromium. The market includes manufacturers, suppliers, and end-users such as construction companies, furniture makers, and outdoor product manufacturers. The growth of the construction industry, increasing awareness about sustainable building materials, and the need for durable wood products are key factors contributing to the expansion of the Global ACQ Wood Preservative Market.

ACQ-A, ACQ-B, ACQ-C, ACQ-D in the Global ACQ Wood Preservative Market:

ACQ-A, ACQ-B, ACQ-C, and ACQ-D are different formulations of Alkaline Copper Quaternary (ACQ) wood preservatives, each designed to meet specific requirements and applications within the Global ACQ Wood Preservative Market. ACQ-A is one of the earliest formulations and is known for its high copper content, which provides excellent protection against wood decay and insect damage. However, its high copper concentration can sometimes lead to increased corrosion of metal fasteners used in wood construction. ACQ-B is a modified version with a balanced composition that reduces the corrosive effects on metals while maintaining effective wood preservation properties. This formulation is widely used in residential and commercial construction projects where metal fasteners are commonly employed. ACQ-C is another variant that includes a higher concentration of quaternary ammonium compounds, enhancing its efficacy against a broader spectrum of fungi and insects. This makes ACQ-C suitable for applications in areas with high moisture levels or where wood is exposed to harsh environmental conditions. ACQ-D, the latest formulation, combines the benefits of previous versions with improved environmental performance. It has a lower copper content and incorporates additional biocides to provide comprehensive protection while minimizing environmental impact. ACQ-D is often preferred for applications where sustainability and reduced environmental footprint are critical considerations. Each of these formulations plays a vital role in the Global ACQ Wood Preservative Market, catering to diverse needs and ensuring the longevity and durability of wood products in various settings.

Indoor, Outdoor in the Global ACQ Wood Preservative Market:

The usage of Global ACQ Wood Preservative Market products spans both indoor and outdoor applications, each with distinct requirements and benefits. For indoor applications, ACQ wood preservatives are commonly used in the construction of wooden furniture, flooring, and structural components such as beams and joists. The primary advantage of using ACQ-treated wood indoors is its ability to resist decay and insect damage, ensuring the longevity and structural integrity of wooden elements. Additionally, ACQ-treated wood is considered safer for indoor use compared to traditional preservatives containing arsenic or chromium, as it poses fewer health risks to occupants. In outdoor applications, ACQ wood preservatives are extensively used in the construction of decks, fences, playground equipment, and landscaping structures. The outdoor environment exposes wood to various elements such as moisture, UV radiation, and biological threats like fungi and insects. ACQ-treated wood provides robust protection against these factors, making it an ideal choice for outdoor projects. The preservative's water-based formulation allows it to penetrate deeply into the wood, offering long-lasting protection even in harsh weather conditions. Moreover, ACQ-treated wood is environmentally friendly, as it does not leach harmful chemicals into the soil or water, making it suitable for use in environmentally sensitive areas. The versatility and effectiveness of ACQ wood preservatives in both indoor and outdoor applications highlight their importance in the Global ACQ Wood Preservative Market, catering to the needs of various industries and ensuring the durability and sustainability of wood products.

Global ACQ Wood Preservative Market Outlook:

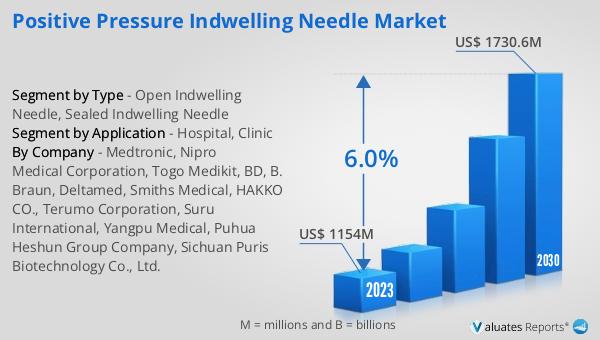

The global ACQ Wood Preservative market was valued at US$ 1154 million in 2023 and is anticipated to reach US$ 1730.6 million by 2030, witnessing a CAGR of 6.0% during the forecast period 2024-2030. This market outlook indicates a significant growth trajectory driven by increasing demand for sustainable and environmentally friendly wood preservation solutions. The projected growth reflects the rising awareness and adoption of ACQ wood preservatives across various industries, including construction, furniture manufacturing, and outdoor product development. The market's expansion is also supported by stringent regulations on the use of traditional wood preservatives, which have led to a shift towards safer and more eco-friendly alternatives like ACQ. As the construction industry continues to grow and the need for durable and long-lasting wood products increases, the Global ACQ Wood Preservative Market is expected to witness sustained demand and innovation in product formulations.

| Report Metric | Details |

| Report Name | ACQ Wood Preservative Market |

| Accounted market size in 2023 | US$ 1154 million |

| Forecasted market size in 2030 | US$ 1730.6 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF, Koopers, Lonza, KMG, Troy, Viance, Dolphin Bay, Remmers, Wykamol |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |