What is Global ESD Foot Grounders Market?

The Global ESD Foot Grounders Market refers to the worldwide industry focused on the production and distribution of Electrostatic Discharge (ESD) foot grounders. These devices are essential in environments where static electricity can cause damage to sensitive electronic components or ignite flammable substances. ESD foot grounders are typically worn on the feet and are designed to safely discharge static electricity to the ground, thereby preventing the buildup of static charges that can lead to costly damages or safety hazards. The market encompasses a variety of products, including disposable and reusable foot grounders, catering to different needs and preferences across various industries. The demand for ESD foot grounders is driven by the increasing awareness of the importance of static control in maintaining the integrity and safety of electronic devices and components. As industries such as electronics manufacturing, laboratories, and other high-tech environments continue to grow, the need for effective static control solutions like ESD foot grounders is expected to rise.

Disposable, Reusable in the Global ESD Foot Grounders Market:

In the Global ESD Foot Grounders Market, products can be broadly categorized into disposable and reusable foot grounders. Disposable ESD foot grounders are designed for single-use applications, making them ideal for environments where hygiene and contamination control are critical. These foot grounders are often used in cleanrooms, laboratories, and other settings where maintaining a sterile environment is paramount. They are typically made from lightweight materials and are easy to apply and remove, providing a convenient solution for temporary or short-term use. On the other hand, reusable ESD foot grounders are designed for long-term use and are made from more durable materials that can withstand repeated wear and tear. These foot grounders are often used in electronics manufacturing facilities, where workers need reliable and consistent static control over extended periods. Reusable foot grounders are typically more cost-effective in the long run, as they can be used multiple times before needing replacement. They are also designed to provide a secure and comfortable fit, ensuring that they remain effective throughout the workday. Both disposable and reusable ESD foot grounders play a crucial role in preventing static-related damages and ensuring the safety and reliability of electronic components and devices. The choice between disposable and reusable foot grounders often depends on the specific needs and requirements of the industry or application. For instance, in environments where contamination control is a top priority, disposable foot grounders may be preferred. In contrast, in settings where cost-effectiveness and durability are more important, reusable foot grounders may be the better option. Regardless of the type, ESD foot grounders are an essential component of any comprehensive static control program, helping to protect sensitive electronic components and ensure the safety of workers.

Laboratory, Electronics Factory, Others in the Global ESD Foot Grounders Market:

The usage of Global ESD Foot Grounders Market products spans various areas, including laboratories, electronics factories, and other high-tech environments. In laboratories, ESD foot grounders are crucial for maintaining a controlled environment where sensitive experiments and tests are conducted. Static electricity can interfere with delicate instruments and measurements, leading to inaccurate results or even damage to expensive equipment. By wearing ESD foot grounders, laboratory personnel can minimize the risk of static buildup and ensure the integrity of their work. In electronics factories, ESD foot grounders are essential for protecting electronic components and devices during the manufacturing process. Static electricity can cause significant damage to integrated circuits, semiconductors, and other sensitive components, leading to costly repairs and production delays. ESD foot grounders help to prevent these issues by providing a reliable path for static discharge, ensuring that workers can handle electronic components safely and efficiently. Additionally, ESD foot grounders are used in other high-tech environments, such as data centers, cleanrooms, and aerospace facilities, where static control is critical for maintaining the performance and reliability of electronic systems. In these settings, ESD foot grounders help to protect valuable equipment and ensure the safety of personnel. Overall, the use of ESD foot grounders in various industries highlights their importance in preventing static-related damages and ensuring the smooth operation of electronic systems.

Global ESD Foot Grounders Market Outlook:

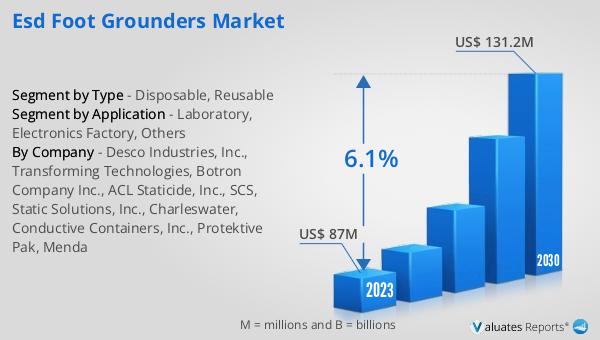

The global ESD Foot Grounders market was valued at US$ 87 million in 2023 and is anticipated to reach US$ 131.2 million by 2030, witnessing a CAGR of 6.1% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for effective static control solutions across various industries, driven by the need to protect sensitive electronic components and ensure the safety of workers. As industries such as electronics manufacturing, laboratories, and other high-tech environments continue to expand, the demand for ESD foot grounders is expected to rise. The market's growth is also supported by advancements in ESD technology and the development of new and improved foot grounder products that offer enhanced performance and durability. Overall, the global ESD Foot Grounders market is poised for significant growth in the coming years, driven by the increasing awareness of the importance of static control and the ongoing expansion of high-tech industries.

| Report Metric | Details |

| Report Name | ESD Foot Grounders Market |

| Accounted market size in 2023 | US$ 87 million |

| Forecasted market size in 2030 | US$ 131.2 million |

| CAGR | 6.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Desco Industries, Inc., Transforming Technologies, Botron Company Inc., ACL Staticide, Inc., SCS, Static Solutions, Inc., Charleswater, Conductive Containers, Inc., Protektive Pak, Menda |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |