What is Global MPPO Market?

The Global MPPO (Modified Polyphenylene Oxide) Market is a specialized segment within the broader plastics and polymers industry. MPPO is a high-performance thermoplastic known for its excellent mechanical properties, thermal stability, and electrical insulation capabilities. These attributes make it highly desirable in various industrial applications. The global market for MPPO is driven by its increasing demand in sectors such as electronics, automotive, medical devices, and aerospace. The material's versatility and superior performance characteristics enable it to replace traditional materials, offering enhanced efficiency and durability. As industries continue to innovate and seek materials that can withstand rigorous conditions, the demand for MPPO is expected to grow. The market is characterized by continuous research and development efforts aimed at improving the material's properties and expanding its application range. This dynamic environment fosters competition among key players, leading to advancements in production techniques and the introduction of new MPPO grades tailored to specific industry needs. Overall, the Global MPPO Market represents a critical component of the modern industrial landscape, contributing to advancements in technology and manufacturing processes.

Injection Molding Grade, Extrusion Grade, Film Grade, Fiber Grade in the Global MPPO Market:

Injection Molding Grade MPPO is specifically designed for applications requiring high precision and strength. This grade is widely used in the automotive industry for manufacturing components such as dashboards, instrument panels, and under-the-hood parts. Its excellent dimensional stability and resistance to high temperatures make it ideal for these applications. Additionally, it is used in the electronics industry for producing connectors, housings, and other components that require precise molding and durability. Extrusion Grade MPPO, on the other hand, is tailored for applications where the material needs to be extruded into long, continuous shapes. This grade is commonly used in the production of pipes, profiles, and sheets. Its high thermal stability and resistance to chemicals make it suitable for use in harsh environments, such as chemical processing plants and industrial machinery. Film Grade MPPO is designed for applications requiring thin, flexible films with excellent barrier properties. This grade is used in the packaging industry for producing films that protect sensitive electronic components, medical devices, and food products from moisture, oxygen, and other contaminants. Its high clarity and strength make it an ideal choice for these applications. Fiber Grade MPPO is engineered for applications requiring high-strength fibers with excellent thermal and chemical resistance. This grade is used in the production of high-performance textiles, such as protective clothing, filtration media, and reinforcement materials for composites. Its superior properties make it suitable for use in demanding environments, such as aerospace and military applications. Each of these MPPO grades is formulated to meet the specific requirements of its intended application, ensuring optimal performance and reliability. The continuous development of new grades and formulations is driven by the evolving needs of various industries, highlighting the importance of MPPO in modern manufacturing and technology.

Electronic, Automotive, Medical Devices, Aerospace in the Global MPPO Market:

The usage of Global MPPO Market in the electronics sector is extensive due to the material's excellent electrical insulation properties and thermal stability. MPPO is used in the production of connectors, housings, and other components that require high precision and durability. Its ability to withstand high temperatures and resist electrical interference makes it an ideal choice for electronic devices and components. In the automotive industry, MPPO is used for manufacturing various components such as dashboards, instrument panels, and under-the-hood parts. Its high strength, dimensional stability, and resistance to high temperatures make it suitable for these applications. Additionally, MPPO's lightweight nature contributes to the overall reduction in vehicle weight, improving fuel efficiency and performance. In the medical devices sector, MPPO is used for producing components that require high precision, strength, and resistance to chemicals and sterilization processes. Its biocompatibility and ability to withstand repeated sterilization cycles make it an ideal material for medical devices such as surgical instruments, diagnostic equipment, and implantable devices. In the aerospace industry, MPPO is used for manufacturing components that require high strength, thermal stability, and resistance to harsh environmental conditions. Its lightweight nature and superior mechanical properties make it suitable for use in aircraft interiors, structural components, and other critical applications. The versatility and superior performance characteristics of MPPO make it a valuable material in these industries, contributing to advancements in technology and manufacturing processes.

Global MPPO Market Outlook:

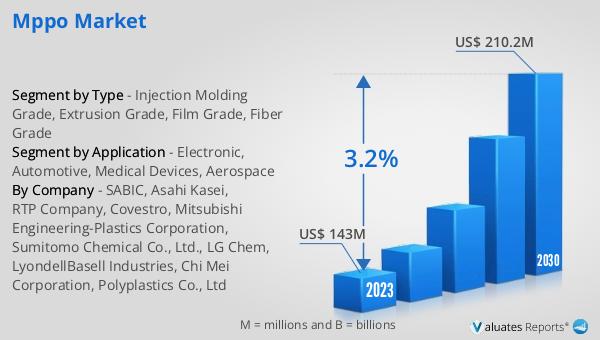

The global MPPO market, valued at US$ 143 million in 2023, is projected to grow significantly, reaching an estimated value of US$ 210.2 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.2% during the forecast period from 2024 to 2030. This upward trend reflects the increasing demand for MPPO across various industries, driven by its superior performance characteristics and versatility. The material's ability to replace traditional materials in demanding applications, such as electronics, automotive, medical devices, and aerospace, is a key factor contributing to its market growth. Continuous research and development efforts aimed at improving MPPO's properties and expanding its application range further support this positive market outlook. As industries continue to innovate and seek materials that can withstand rigorous conditions, the demand for MPPO is expected to grow, driving the market's expansion. The competitive landscape of the MPPO market is characterized by the presence of key players who are focused on developing new grades and formulations to meet the evolving needs of various industries. This dynamic environment fosters advancements in production techniques and the introduction of new MPPO grades tailored to specific industry requirements. Overall, the global MPPO market is poised for significant growth, reflecting its critical role in modern industrial applications and its contribution to technological advancements.

| Report Metric | Details |

| Report Name | MPPO Market |

| Accounted market size in 2023 | US$ 143 million |

| Forecasted market size in 2030 | US$ 210.2 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | SABIC, Asahi Kasei, RTP Company, Covestro, Mitsubishi Engineering-Plastics Corporation, Sumitomo Chemical Co., Ltd., LG Chem, LyondellBasell Industries, Chi Mei Corporation, Polyplastics Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |