What is Global Face Detection Tools Market?

The Global Face Detection Tools Market refers to the worldwide industry focused on the development, production, and distribution of software and hardware solutions that can identify and verify human faces in digital images or video streams. These tools utilize advanced algorithms and machine learning techniques to detect facial features and match them against stored data for various applications such as security, authentication, and user interaction. The market encompasses a wide range of products, from simple facial recognition software integrated into smartphones to complex systems used in surveillance and access control. The growing demand for enhanced security measures, coupled with advancements in artificial intelligence, has significantly driven the expansion of this market. Additionally, the increasing adoption of face detection technology in sectors like retail, healthcare, and banking further fuels its growth. As businesses and governments continue to seek more efficient and reliable methods for identity verification and security, the Global Face Detection Tools Market is poised for substantial development in the coming years.

On-premise Deployment, Cloud Deployment in the Global Face Detection Tools Market:

On-premise deployment and cloud deployment are two primary methods for implementing face detection tools in the Global Face Detection Tools Market. On-premise deployment involves installing and running the face detection software on local servers and infrastructure within an organization. This method offers several advantages, including greater control over data security and privacy, as the data remains within the organization's premises. It is particularly beneficial for industries that handle sensitive information, such as government agencies, financial institutions, and healthcare providers. On-premise deployment also allows for customization and integration with existing systems, providing a tailored solution that meets specific organizational needs. However, it requires significant upfront investment in hardware and ongoing maintenance costs, which can be a barrier for smaller organizations. In contrast, cloud deployment involves hosting the face detection software on remote servers managed by third-party service providers. This method offers several benefits, including scalability, flexibility, and cost-effectiveness. Organizations can easily scale their usage up or down based on demand, without the need for significant capital investment in infrastructure. Cloud deployment also enables remote access, allowing users to access the face detection tools from anywhere with an internet connection. This is particularly advantageous for organizations with distributed teams or those that require real-time data processing and analysis. Additionally, cloud service providers often offer robust security measures and regular updates, ensuring that the software remains up-to-date and secure. Despite these advantages, cloud deployment also has its challenges. Data security and privacy concerns are paramount, as sensitive information is stored on external servers. Organizations must carefully evaluate the security measures and compliance standards of their chosen cloud service provider to mitigate these risks. Additionally, reliance on internet connectivity can be a limitation, particularly in regions with unstable or limited internet access. Organizations must weigh the benefits and drawbacks of each deployment method to determine the best fit for their specific needs and requirements. In summary, both on-premise and cloud deployment methods offer unique advantages and challenges for implementing face detection tools in the Global Face Detection Tools Market. On-premise deployment provides greater control over data security and customization but requires significant investment in infrastructure and maintenance. Cloud deployment offers scalability, flexibility, and cost-effectiveness but raises concerns about data security and reliance on internet connectivity. Organizations must carefully consider their specific needs, resources, and risk tolerance when choosing the most suitable deployment method for their face detection tools.

Large Corporation, SMEs in the Global Face Detection Tools Market:

The usage of Global Face Detection Tools Market in large corporations and SMEs (Small and Medium-sized Enterprises) varies significantly based on their unique needs and resources. Large corporations often have extensive security and operational requirements, making face detection tools an essential component of their infrastructure. These tools are used for various purposes, including access control, employee attendance tracking, and enhancing customer experiences. For instance, in the retail sector, large corporations use face detection technology to analyze customer behavior, personalize marketing efforts, and prevent theft. In the banking sector, face detection tools are employed for secure customer authentication and fraud prevention. The ability to integrate face detection technology with existing systems and customize it to meet specific needs makes it a valuable asset for large corporations. On the other hand, SMEs may have different priorities and constraints when it comes to adopting face detection tools. While they may not have the same level of resources as large corporations, SMEs can still benefit significantly from this technology. For example, SMEs in the retail industry can use face detection tools to enhance customer service by recognizing repeat customers and offering personalized recommendations. In the hospitality sector, SMEs can improve security and streamline check-in processes by using face detection for guest verification. Additionally, face detection tools can help SMEs in various industries improve operational efficiency by automating attendance tracking and access control. However, the adoption of face detection tools by SMEs may be influenced by factors such as cost, ease of implementation, and data security concerns. Cloud-based face detection solutions can be particularly appealing to SMEs due to their lower upfront costs and scalability. These solutions allow SMEs to access advanced face detection technology without the need for significant investment in infrastructure. Moreover, cloud-based solutions often come with regular updates and maintenance, reducing the burden on SMEs to manage the technology themselves. Nevertheless, SMEs must carefully evaluate the security measures and compliance standards of cloud service providers to ensure the protection of sensitive data. In conclusion, the usage of Global Face Detection Tools Market in large corporations and SMEs is driven by their specific needs and resources. Large corporations leverage face detection technology for enhanced security, operational efficiency, and customer engagement, while SMEs use it to improve customer service, streamline operations, and enhance security. The choice between on-premise and cloud deployment methods plays a crucial role in determining the feasibility and effectiveness of face detection tools for both large corporations and SMEs. By carefully considering their unique requirements and constraints, organizations of all sizes can harness the power of face detection technology to achieve their goals.

Global Face Detection Tools Market Outlook:

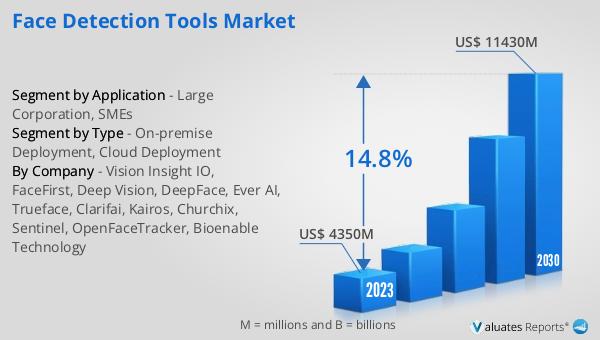

The global Face Detection Tools market was valued at US$ 4350 million in 2023 and is anticipated to reach US$ 11430 million by 2030, witnessing a CAGR of 14.8% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced security solutions and the widespread adoption of face detection technology across various industries. The market's expansion is driven by factors such as the rising need for enhanced security measures, advancements in artificial intelligence and machine learning, and the growing use of face detection tools in sectors like retail, healthcare, and banking. As businesses and governments continue to seek more efficient and reliable methods for identity verification and security, the Global Face Detection Tools Market is poised for substantial development in the coming years. The increasing integration of face detection technology in consumer electronics, such as smartphones and smart home devices, further contributes to the market's growth. Additionally, the development of innovative applications, such as emotion recognition and augmented reality, opens new opportunities for the face detection tools market. As a result, the market is expected to witness robust growth, driven by technological advancements and the expanding scope of face detection applications.

| Report Metric | Details |

| Report Name | Face Detection Tools Market |

| Accounted market size in 2023 | US$ 4350 million |

| Forecasted market size in 2030 | US$ 11430 million |

| CAGR | 14.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Vision Insight IO, FaceFirst, Deep Vision, DeepFace, Ever AI, Trueface, Clarifai, Kairos, Churchix, Sentinel, OpenFaceTracker, Bioenable Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |