What is Global Hematology Sample Preparation System Market?

The Global Hematology Sample Preparation System Market is a specialized segment within the broader medical device industry, focusing on the preparation of blood samples for various diagnostic tests. Hematology is the study of blood, blood-forming organs, and blood diseases. The preparation of blood samples is a critical step in ensuring accurate diagnostic results. This market includes a range of devices and systems designed to handle, process, and prepare blood samples for analysis. These systems are used in hospitals, diagnostic laboratories, research institutions, and blood banks. They help in the detection and monitoring of various blood disorders, infections, and other medical conditions. The market is driven by the increasing prevalence of blood-related diseases, advancements in technology, and the growing demand for accurate and efficient diagnostic tools. The systems in this market are designed to improve the efficiency and accuracy of blood sample preparation, thereby enhancing the overall quality of diagnostic results.

in the Global Hematology Sample Preparation System Market:

The Global Hematology Sample Preparation System Market offers a variety of types to cater to the diverse needs of its customers. One of the primary types is the automated sample preparation system. These systems are designed to handle large volumes of samples with minimal human intervention, thereby reducing the risk of errors and increasing efficiency. Automated systems are particularly popular in large hospitals and diagnostic laboratories where the volume of samples is high. Another type is the semi-automated sample preparation system. These systems combine manual and automated processes, offering a balance between efficiency and control. They are suitable for medium-sized laboratories and hospitals where the volume of samples is moderate. Manual sample preparation systems are also available and are typically used in smaller laboratories and research institutions where the volume of samples is low, and there is a need for greater control over the preparation process. These systems require skilled technicians to handle the samples and perform the necessary steps manually. In addition to these, there are specialized sample preparation systems designed for specific applications. For example, there are systems designed for the preparation of blood smears, which are used to examine the morphology of blood cells under a microscope. There are also systems designed for the preparation of samples for flow cytometry, a technique used to analyze the physical and chemical characteristics of cells. Another type of system is the centrifuge, which is used to separate different components of blood based on their density. Centrifuges are widely used in both clinical and research settings. There are also systems designed for the preparation of samples for molecular diagnostics, which involve the analysis of DNA, RNA, and proteins. These systems are used in advanced diagnostic laboratories and research institutions. The choice of system depends on various factors, including the volume of samples, the level of automation required, the specific application, and the available budget. Each type of system has its own advantages and limitations, and customers need to carefully evaluate their needs and requirements before making a decision. The availability of a wide range of systems ensures that there is a suitable option for every customer, regardless of their size, budget, or specific needs.

in the Global Hematology Sample Preparation System Market:

The Global Hematology Sample Preparation System Market serves a wide range of applications, each with its own specific requirements and challenges. One of the primary applications is in clinical diagnostics. In this setting, hematology sample preparation systems are used to prepare blood samples for various diagnostic tests, including complete blood counts (CBC), blood smears, and flow cytometry. These tests are essential for the diagnosis and monitoring of various blood disorders, infections, and other medical conditions. The accuracy and efficiency of the sample preparation process are critical in ensuring reliable diagnostic results. Another important application is in research and development. In research laboratories, hematology sample preparation systems are used to prepare samples for various types of analysis, including molecular diagnostics, cell culture, and genetic studies. These systems are essential for the accurate and efficient preparation of samples, which is critical for the success of research projects. The ability to handle and process samples accurately and efficiently is particularly important in research settings, where the quality of the results can have a significant impact on the outcome of the study. Blood banks and transfusion centers also rely on hematology sample preparation systems for the preparation of blood samples. In these settings, the systems are used to prepare samples for testing and processing, ensuring that the blood is safe for transfusion. The accuracy and efficiency of the sample preparation process are critical in ensuring the safety and quality of the blood supply. Another application is in veterinary diagnostics. Hematology sample preparation systems are used in veterinary clinics and laboratories to prepare blood samples from animals for various diagnostic tests. These systems are essential for the accurate and efficient diagnosis of various diseases and conditions in animals. The ability to handle and process samples accurately and efficiently is particularly important in veterinary settings, where the quality of the results can have a significant impact on the health and well-being of the animals. In addition to these applications, hematology sample preparation systems are also used in forensic laboratories. In this setting, the systems are used to prepare blood samples for various types of analysis, including DNA testing and toxicology. The accuracy and efficiency of the sample preparation process are critical in ensuring reliable results, which can have a significant impact on the outcome of forensic investigations. Overall, the Global Hematology Sample Preparation System Market serves a wide range of applications, each with its own specific requirements and challenges. The availability of a wide range of systems ensures that there is a suitable option for every application, regardless of the specific needs and requirements.

Global Hematology Sample Preparation System Market Outlook:

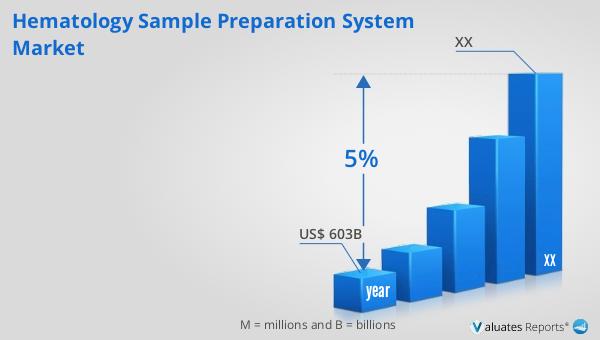

Based on our research, the global market for medical devices is projected to reach approximately $603 billion by 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by various factors, including technological advancements, increasing prevalence of chronic diseases, and the rising demand for healthcare services. The medical device market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices. The continuous innovation in medical technology is expected to drive the growth of this market, providing new and improved solutions for patient care. Additionally, the increasing aging population and the growing awareness about health and wellness are contributing to the rising demand for medical devices. The market is also benefiting from the expanding healthcare infrastructure in emerging economies, which is creating new opportunities for growth. Overall, the global medical device market is poised for significant growth in the coming years, driven by a combination of technological advancements, increasing healthcare needs, and expanding market opportunities.

| Report Metric | Details |

| Report Name | Hematology Sample Preparation System Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |