What is Global Chromatography Instruments Market?

The Global Chromatography Instruments Market refers to the worldwide industry focused on the production, distribution, and utilization of chromatography instruments. Chromatography is a laboratory technique used to separate mixtures into their individual components, making it essential for various scientific and industrial applications. The market encompasses a wide range of instruments, including gas chromatography, liquid chromatography, supercritical fluid chromatography, and thin-layer chromatography devices. These instruments are crucial for research and development in fields such as pharmaceuticals, biochemistry, food and beverage testing, and environmental analysis. The market's growth is driven by the increasing demand for accurate and efficient analytical techniques, advancements in technology, and the expanding applications of chromatography in different sectors. As industries continue to prioritize quality control and regulatory compliance, the need for sophisticated chromatography instruments is expected to rise, making this market a vital component of the global scientific and industrial landscape.

Gas Chromatography Instruments, Liquid Chromatography, Supercritical Fluid Chromatography, Thin-Layer Chromatography, Others in the Global Chromatography Instruments Market:

Gas Chromatography Instruments are widely used in the Global Chromatography Instruments Market for their ability to separate and analyze compounds that can be vaporized without decomposition. These instruments are essential in the pharmaceutical industry for drug development and quality control, as they provide precise and reliable results. Liquid Chromatography, on the other hand, is a versatile technique used to separate and analyze compounds in liquid form. It is commonly used in biochemistry and environmental analysis to identify and quantify various substances. Supercritical Fluid Chromatography combines the benefits of gas and liquid chromatography, offering high efficiency and selectivity. It is particularly useful in the analysis of complex mixtures and is gaining popularity in the pharmaceutical and food industries. Thin-Layer Chromatography is a simple and cost-effective technique used for the qualitative analysis of compounds. It is widely used in the food and beverage industry for quality control and in environmental analysis for detecting pollutants. Other chromatography techniques, such as ion exchange chromatography and affinity chromatography, also play a significant role in the market. These techniques are used in various applications, including protein purification and the analysis of biomolecules. Overall, the Global Chromatography Instruments Market is characterized by a diverse range of instruments and techniques, each with its unique advantages and applications.

Pharmaceutical Industry, Biochemistry, Food and Beverage Testing, Environmental Analysis in the Global Chromatography Instruments Market:

The usage of Global Chromatography Instruments Market spans across several critical areas, including the Pharmaceutical Industry, Biochemistry, Food and Beverage Testing, and Environmental Analysis. In the Pharmaceutical Industry, chromatography instruments are indispensable for drug development, quality control, and regulatory compliance. They help in the identification, quantification, and purification of pharmaceutical compounds, ensuring the safety and efficacy of drugs. In Biochemistry, chromatography is used to analyze complex biological samples, such as proteins, nucleic acids, and metabolites. It aids in understanding biochemical pathways, disease mechanisms, and the development of diagnostic tools. In the Food and Beverage Testing sector, chromatography instruments are used to ensure the safety and quality of products. They help in detecting contaminants, additives, and nutritional components, ensuring compliance with food safety regulations. Environmental Analysis is another crucial area where chromatography instruments are extensively used. They help in monitoring and analyzing pollutants in air, water, and soil, contributing to environmental protection and public health. The versatility and precision of chromatography instruments make them essential tools in these areas, driving the growth of the Global Chromatography Instruments Market.

Global Chromatography Instruments Market Outlook:

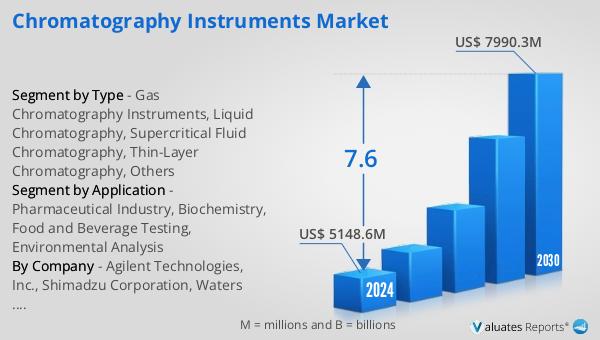

The global Chromatography Instruments market is anticipated to expand from US$ 5148.6 million in 2024 to US$ 7990.3 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 7.6% during the forecast period. The United States holds the largest share of this market, accounting for approximately 41%. Europe follows, with about 32% of the market share. The top three companies in the market collectively occupy around 39% of the market share. This growth is driven by the increasing demand for advanced analytical techniques across various industries, including pharmaceuticals, biochemistry, food and beverage testing, and environmental analysis. The market's expansion is also fueled by technological advancements and the growing need for regulatory compliance and quality control. As industries continue to prioritize precision and efficiency in their analytical processes, the demand for sophisticated chromatography instruments is expected to rise, making this market a critical component of the global scientific and industrial landscape.

| Report Metric | Details |

| Report Name | Chromatography Instruments Market |

| Accounted market size in 2024 | US$ 5148.6 in million |

| Forecasted market size in 2030 | US$ 7990.3 million |

| CAGR | 7.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Agilent Technologies, Inc., Shimadzu Corporation, Waters Corporation, Thermo Fisher Scientific, Inc., Perkinelmer, Inc., Phenomenex, Inc., GL Sciences, Inc., Pall Corporation, Novasep Holding S.A.S., Jasco, Inc., Bio-rad, GEHealthcare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |