What is Global Inspection System for Pharmaceutical Market?

The Global Inspection System for Pharmaceutical Market is a critical component in ensuring the safety, efficacy, and quality of pharmaceutical products. These systems are designed to detect and eliminate defects in pharmaceutical products, such as tablets, capsules, and injectable solutions, before they reach consumers. They utilize advanced technologies like machine vision, X-ray, and infrared spectroscopy to inspect products for physical and chemical inconsistencies. This process is vital for maintaining compliance with stringent regulatory standards set by health authorities worldwide. By implementing these inspection systems, pharmaceutical companies can minimize the risk of product recalls, enhance their brand reputation, and ensure patient safety. The market for these systems is driven by the increasing demand for high-quality pharmaceuticals, the need for compliance with regulatory standards, and advancements in inspection technologies. As the pharmaceutical industry continues to grow, the importance of robust inspection systems becomes even more pronounced, making them an indispensable part of the pharmaceutical manufacturing process.

Automatic, Semi-automatic in the Global Inspection System for Pharmaceutical Market:

Automatic and semi-automatic inspection systems play a crucial role in the Global Inspection System for Pharmaceutical Market. Automatic inspection systems are fully automated and require minimal human intervention. They are equipped with advanced sensors, cameras, and software algorithms that can detect defects with high precision and speed. These systems are ideal for high-volume production lines where consistency and efficiency are paramount. They can inspect thousands of units per hour, ensuring that only products that meet the highest quality standards are released to the market. On the other hand, semi-automatic inspection systems combine manual and automated processes. They require human operators to load and unload products, but the inspection itself is carried out by automated machinery. This type of system is suitable for smaller production runs or for products that require more detailed inspection that cannot be fully automated. Semi-automatic systems offer a balance between cost and efficiency, making them a popular choice for many pharmaceutical manufacturers. Both types of systems are essential for maintaining product quality and compliance with regulatory standards. They help in identifying defects such as cracks, chips, contamination, and incorrect labeling, which can compromise the safety and efficacy of pharmaceutical products. The choice between automatic and semi-automatic systems depends on various factors, including production volume, budget, and the specific requirements of the inspection process. As technology continues to advance, we can expect to see even more sophisticated inspection systems that offer greater accuracy, speed, and reliability. These systems not only help in ensuring product quality but also contribute to the overall efficiency and profitability of pharmaceutical manufacturing operations.

Pharmaceutical Industry, Health Products Industry in the Global Inspection System for Pharmaceutical Market:

The usage of Global Inspection Systems in the Pharmaceutical Industry and Health Products Industry is extensive and multifaceted. In the Pharmaceutical Industry, these systems are employed at various stages of the manufacturing process to ensure that the final products meet the required quality standards. They are used to inspect raw materials, in-process materials, and finished products. For instance, during the production of tablets, inspection systems can detect defects such as cracks, chips, and incorrect dimensions. In the case of injectable solutions, they can identify particulate contamination and ensure that the solutions are free from any foreign particles. These systems also play a crucial role in verifying the accuracy of labeling and packaging, which is essential for ensuring that patients receive the correct medication and dosage. In the Health Products Industry, inspection systems are used to ensure the quality and safety of a wide range of products, including dietary supplements, medical devices, and over-the-counter medications. These systems help in detecting defects and contaminants that could pose a risk to consumer health. For example, in the production of dietary supplements, inspection systems can identify inconsistencies in tablet size and shape, as well as the presence of foreign materials. In the case of medical devices, they can detect defects such as cracks, chips, and incorrect assembly, which could compromise the safety and efficacy of the devices. By implementing robust inspection systems, companies in the Health Products Industry can ensure that their products meet the highest quality standards and comply with regulatory requirements. This not only helps in protecting consumer health but also enhances the reputation and credibility of the companies. Overall, the usage of Global Inspection Systems in the Pharmaceutical and Health Products Industries is essential for ensuring product quality, safety, and compliance with regulatory standards.

Global Inspection System for Pharmaceutical Market Outlook:

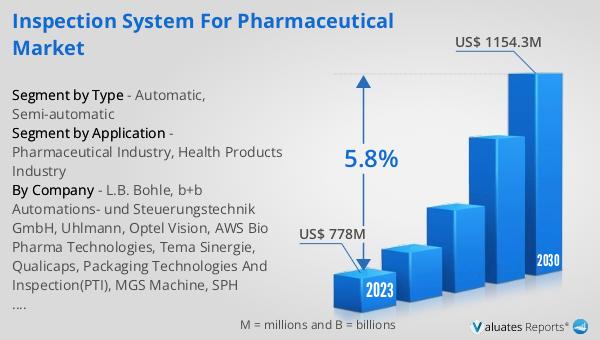

The global Inspection System for Pharmaceutical market was valued at US$ 778 million in 2023 and is anticipated to reach US$ 1154.3 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. The global pharmaceutical market is 1475 billion USD in 2022, growing at a CAGR of 5% during the next six years. In comparison, the chemical drug market is estimated to increase from 1005 billion in 2018 to 1094 billion U.S. dollars in 2022. This growth highlights the increasing demand for high-quality pharmaceutical products and the critical role that inspection systems play in ensuring product safety and efficacy. As the pharmaceutical industry continues to expand, the need for advanced inspection systems becomes even more pronounced. These systems help in maintaining compliance with stringent regulatory standards, minimizing the risk of product recalls, and ensuring patient safety. The market for inspection systems is driven by the increasing demand for high-quality pharmaceuticals, advancements in inspection technologies, and the need for compliance with regulatory standards. As technology continues to evolve, we can expect to see even more sophisticated inspection systems that offer greater accuracy, speed, and reliability. These systems not only help in ensuring product quality but also contribute to the overall efficiency and profitability of pharmaceutical manufacturing operations.

| Report Metric | Details |

| Report Name | Inspection System for Pharmaceutical Market |

| Accounted market size in 2023 | US$ 778 million |

| Forecasted market size in 2030 | US$ 1154.3 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | L.B. Bohle, b+b Automations- und Steuerungstechnik GmbH, Uhlmann, Optel Vision, AWS Bio Pharma Technologies, Tema Sinergie, Qualicaps, Packaging Technologies And Inspection(PTI), MGS Machine, SPH Group, Cozzoli Machine Company, MG America, Anchor Mark, Marchesini Group, Mettler Toledo, Nipro |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |