What is Automated Benchtop Immunoanalyzer - Global Market?

Automated Benchtop Immunoanalyzers are compact, laboratory instruments designed to perform immunoassays, which are tests that measure the presence or concentration of substances in a sample using the reaction of an antibody or antibodies to its antigen. These devices are essential in medical diagnostics, enabling the detection of various biomarkers, hormones, and pathogens in blood, urine, and other bodily fluids. The global market for these analyzers is driven by the increasing demand for rapid, accurate, and reliable diagnostic tests. They are widely used in hospitals, diagnostic laboratories, and research institutions due to their efficiency and ease of use. The automation of these benchtop devices reduces human error, enhances throughput, and ensures consistent results, making them indispensable in modern healthcare settings. As technology advances, these analyzers are becoming more sophisticated, offering higher sensitivity, faster processing times, and the ability to handle multiple tests simultaneously. This evolution is expected to continue, further expanding their applications and market reach.

Semi-Automatic, Fully-Automatic in the Automated Benchtop Immunoanalyzer - Global Market:

Automated Benchtop Immunoanalyzers can be categorized into semi-automatic and fully-automatic systems, each with its own set of features and benefits. Semi-automatic immunoanalyzers require some manual intervention, such as sample loading and reagent preparation, but automate the actual testing process. These systems are typically more affordable and are suitable for smaller laboratories or facilities with lower testing volumes. They offer a balance between cost and functionality, making them an attractive option for many healthcare providers. On the other hand, fully-automatic immunoanalyzers handle the entire testing process from start to finish with minimal human intervention. These advanced systems can process a large number of samples simultaneously, significantly increasing throughput and efficiency. They are ideal for high-volume laboratories and hospitals where speed and accuracy are critical. Fully-automatic systems often come with advanced features such as barcode scanning, automated sample handling, and integrated data management, which further streamline the workflow and reduce the risk of errors. The choice between semi-automatic and fully-automatic systems depends on various factors, including the volume of tests, budget, and specific needs of the facility. Both types of analyzers play a crucial role in the global market, catering to different segments and ensuring that healthcare providers have the tools they need to deliver accurate and timely diagnoses. As the demand for diagnostic testing continues to grow, the market for both semi-automatic and fully-automatic benchtop immunoanalyzers is expected to expand, driven by technological advancements and the increasing emphasis on quality healthcare.

Hospitals, Diagnostic Laboratories, Others in the Automated Benchtop Immunoanalyzer - Global Market:

Automated Benchtop Immunoanalyzers are extensively used in various healthcare settings, including hospitals, diagnostic laboratories, and other medical facilities. In hospitals, these analyzers are crucial for providing rapid and accurate diagnostic results, which are essential for patient care and treatment decisions. They enable the detection of a wide range of conditions, from infectious diseases to hormonal imbalances, ensuring that patients receive timely and appropriate care. The automation of these devices reduces the workload of laboratory staff, allowing them to focus on more complex tasks and improving overall efficiency. In diagnostic laboratories, automated benchtop immunoanalyzers are indispensable tools for routine testing and specialized diagnostics. They offer high throughput and consistent results, making them ideal for large-scale screening programs and research studies. These laboratories rely on the precision and reliability of automated systems to deliver accurate results, which are critical for disease monitoring, epidemiological studies, and public health initiatives. Other medical facilities, such as clinics and research institutions, also benefit from the use of automated benchtop immunoanalyzers. In clinics, these devices provide quick and reliable test results, enabling healthcare providers to make informed decisions and improve patient outcomes. Research institutions use these analyzers for various applications, including biomarker discovery, drug development, and clinical trials. The versatility and efficiency of automated benchtop immunoanalyzers make them valuable assets in any healthcare setting, contributing to better patient care and advancing medical research.

Automated Benchtop Immunoanalyzer - Global Market Outlook:

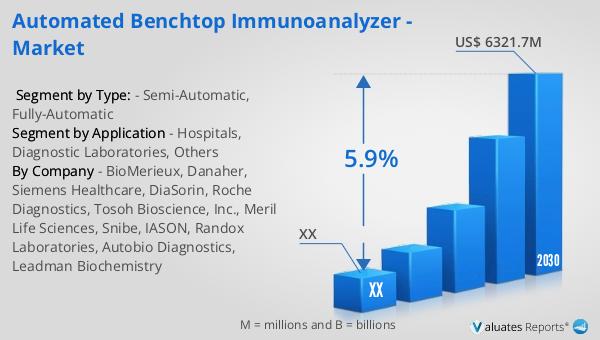

The global market for Automated Benchtop Immunoanalyzers was valued at approximately US$ 4213 million in 2023 and is projected to reach around US$ 6321.7 million by 2030, growing at a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2030. In North America, the market for these immunoanalyzers was valued at $ million in 2023 and is expected to reach $ million by 2030, with a CAGR of % over the same period. This growth is driven by the increasing demand for accurate and efficient diagnostic tools, advancements in technology, and the rising prevalence of chronic diseases. The adoption of automated benchtop immunoanalyzers in various healthcare settings, including hospitals, diagnostic laboratories, and research institutions, is contributing to the market's expansion. These devices offer numerous benefits, such as reduced human error, enhanced throughput, and consistent results, making them essential in modern healthcare. As the market continues to grow, manufacturers are focusing on developing more advanced and user-friendly systems to meet the evolving needs of healthcare providers and improve patient outcomes.

| Report Metric | Details |

| Report Name | Automated Benchtop Immunoanalyzer - Market |

| Forecasted market size in 2030 | US$ 6321.7 million |

| CAGR | 5.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BioMerieux, Danaher, Siemens Healthcare, DiaSorin, Roche Diagnostics, Tosoh Bioscience, Inc., Meril Life Sciences, Snibe, IASON, Randox Laboratories, Autobio Diagnostics, Leadman Biochemistry |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |