What is Global Car Cast Camshaft Market?

The Global Car Cast Camshaft Market is a significant segment within the automotive industry, focusing on the production and distribution of camshafts made from cast materials. Camshafts are crucial components in internal combustion engines, responsible for controlling the timing and movement of the engine's valves. The market encompasses various types of camshafts, including those made from cast iron and other alloys, which are preferred for their durability and cost-effectiveness. The demand for cast camshafts is driven by the need for efficient engine performance, fuel efficiency, and adherence to stringent emission norms. This market is influenced by factors such as advancements in manufacturing technologies, increasing vehicle production, and the growing emphasis on reducing vehicle weight to improve fuel efficiency. The global reach of this market indicates its importance in both developed and developing regions, catering to a wide range of automotive manufacturers and suppliers.

Alloy Cast Iron Camshafts, Ductile Iron Camshafts in the Global Car Cast Camshaft Market:

Alloy cast iron camshafts and ductile iron camshafts are two prominent types within the Global Car Cast Camshaft Market. Alloy cast iron camshafts are known for their excellent wear resistance and strength, making them suitable for high-performance engines. These camshafts are typically made by adding various alloying elements such as chromium, molybdenum, and nickel to the base iron, enhancing their mechanical properties and resistance to thermal fatigue. This makes them ideal for use in engines that operate under high stress and temperature conditions. On the other hand, ductile iron camshafts, also known as nodular iron camshafts, offer a unique combination of strength, toughness, and machinability. The addition of nodular graphite in the iron matrix gives these camshafts superior fatigue resistance and impact strength compared to traditional grey cast iron camshafts. Ductile iron camshafts are often used in commercial vehicles and heavy-duty applications where durability and reliability are paramount. Both types of camshafts play a crucial role in the automotive industry, ensuring optimal engine performance and longevity. The choice between alloy cast iron and ductile iron camshafts depends on the specific requirements of the engine and the operating conditions it will face. As the automotive industry continues to evolve, the demand for high-quality camshafts that can withstand rigorous operating conditions is expected to grow, further driving innovation and development in the Global Car Cast Camshaft Market.

Passenger Vehicle, Commercial Vehicle in the Global Car Cast Camshaft Market:

The usage of cast camshafts in passenger vehicles and commercial vehicles highlights the versatility and importance of these components in the automotive industry. In passenger vehicles, cast camshafts are essential for ensuring smooth engine operation, fuel efficiency, and compliance with emission standards. These vehicles require camshafts that can provide precise valve timing and durability to withstand everyday driving conditions. The use of alloy cast iron camshafts in passenger vehicles is common due to their ability to offer a balance between performance and cost. These camshafts help in achieving optimal engine performance, contributing to a smoother and more efficient driving experience for consumers. On the other hand, commercial vehicles, which include trucks, buses, and other heavy-duty vehicles, demand camshafts that can endure more strenuous operating conditions. Ductile iron camshafts are often preferred in these applications due to their superior strength and fatigue resistance. Commercial vehicles typically operate for longer hours and under heavier loads, making the durability and reliability of camshafts critical. The ability of ductile iron camshafts to withstand high stress and impact makes them suitable for these demanding applications. Additionally, the use of cast camshafts in commercial vehicles contributes to lower maintenance costs and longer engine life, which are crucial factors for fleet operators and businesses. Overall, the Global Car Cast Camshaft Market caters to a wide range of vehicle types, ensuring that both passenger and commercial vehicles can benefit from the advancements in camshaft technology.

Global Car Cast Camshaft Market Outlook:

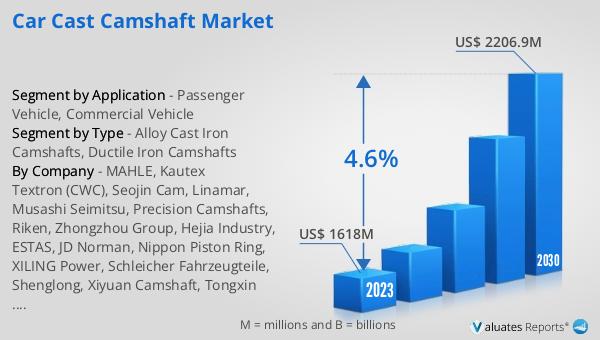

The global Car Cast Camshaft market was valued at US$ 1618 million in 2023 and is anticipated to reach US$ 2206.9 million by 2030, witnessing a CAGR of 4.6% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by factors such as increasing vehicle production, advancements in manufacturing technologies, and the growing emphasis on fuel efficiency and emission control. The rising demand for high-performance and durable camshafts in both passenger and commercial vehicles is expected to contribute significantly to this growth. As automotive manufacturers continue to innovate and improve engine designs, the need for reliable and efficient camshafts will remain a critical component of the industry. The projected growth in the Global Car Cast Camshaft Market underscores the importance of these components in achieving optimal engine performance and meeting regulatory standards.

| Report Metric | Details |

| Report Name | Car Cast Camshaft Market |

| Accounted market size in 2023 | US$ 1618 million |

| Forecasted market size in 2030 | US$ 2206.9 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MAHLE, Kautex Textron (CWC), Seojin Cam, Linamar, Musashi Seimitsu, Precision Camshafts, Riken, Zhongzhou Group, Hejia Industry, ESTAS, JD Norman, Nippon Piston Ring, XILING Power, Schleicher Fahrzeugteile, Shenglong, Xiyuan Camshaft, Tongxin Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |