What is Global Cooling Vests for Surgeons Market?

Global Cooling Vests for Surgeons Market refers to a specialized segment within the medical devices industry that focuses on providing temperature-regulating garments specifically designed for surgeons. These vests are engineered to maintain a comfortable body temperature for surgeons who often work in high-stress, high-temperature environments, such as operating rooms. The primary goal of these cooling vests is to enhance the comfort and performance of surgeons, thereby improving their focus and reducing the risk of heat-related fatigue or errors during lengthy surgical procedures. The market encompasses various types of cooling vests, each utilizing different technologies to achieve the desired cooling effect. These vests are becoming increasingly popular due to the growing awareness of the importance of maintaining optimal working conditions for healthcare professionals. As the demand for advanced medical devices continues to rise, the Global Cooling Vests for Surgeons Market is expected to see significant growth, driven by innovations in cooling technologies and an increasing emphasis on surgeon well-being.

Circulatory Powered Cooling Vests, Cold Pack Cooling Vests, Phase Change Cooling Vests, Others in the Global Cooling Vests for Surgeons Market:

Circulatory Powered Cooling Vests, Cold Pack Cooling Vests, Phase Change Cooling Vests, and other types of cooling vests each offer unique benefits and functionalities within the Global Cooling Vests for Surgeons Market. Circulatory Powered Cooling Vests utilize a system of tubes and a pump to circulate cool water throughout the vest, providing continuous and adjustable cooling. This type of vest is particularly effective for long surgeries as it can maintain a consistent temperature over extended periods. Cold Pack Cooling Vests, on the other hand, use removable ice packs or gel packs that are inserted into pockets within the vest. These packs need to be frozen before use and can provide immediate cooling relief, although their effectiveness diminishes as the packs thaw. Phase Change Cooling Vests employ materials that change phase, such as from solid to liquid, at specific temperatures. These materials absorb heat as they melt, providing a cooling effect. Once the material has fully melted, the vest needs to be recharged by placing it in a cooler environment. This type of vest offers a balance between the continuous cooling of circulatory systems and the simplicity of cold packs. Other types of cooling vests may include evaporative cooling vests, which use water evaporation to provide cooling, or hybrid systems that combine multiple cooling technologies. Each type of vest has its own set of advantages and limitations, making them suitable for different surgical environments and surgeon preferences. The choice of vest often depends on factors such as the duration of the surgery, the ambient temperature of the operating room, and the specific cooling needs of the surgeon. As technology advances, we can expect to see further innovations in cooling vest designs, enhancing their effectiveness and usability in the surgical field.

Hospital, Clinic, Others in the Global Cooling Vests for Surgeons Market:

The usage of Global Cooling Vests for Surgeons Market extends across various healthcare settings, including hospitals, clinics, and other medical facilities. In hospitals, cooling vests are primarily used in operating rooms where surgeons perform complex and lengthy procedures. The high-intensity environment of an operating room, combined with the need for precision and focus, makes temperature regulation crucial. Cooling vests help surgeons maintain a comfortable body temperature, reducing the risk of heat stress and fatigue, which can impair their performance. In clinics, where surgical procedures may be shorter but still require a high level of concentration, cooling vests provide similar benefits. They help ensure that surgeons remain comfortable and focused, even during minor surgeries or outpatient procedures. Additionally, cooling vests can be used in other medical settings, such as ambulatory surgical centers or specialized surgical units, where maintaining optimal working conditions for surgeons is equally important. Beyond these traditional healthcare environments, cooling vests may also find applications in veterinary surgery, military medical units, and disaster response teams, where surgeons often work in challenging conditions. The versatility and effectiveness of cooling vests make them a valuable tool for enhancing surgeon performance and well-being across a wide range of medical settings. As awareness of the benefits of cooling vests continues to grow, their adoption is likely to increase, further driving the growth of the Global Cooling Vests for Surgeons Market.

Global Cooling Vests for Surgeons Market Outlook:

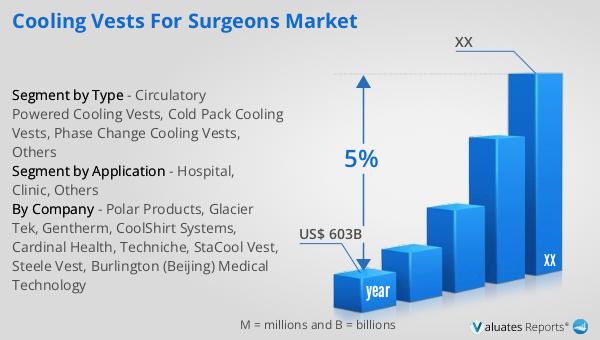

According to our research, the global market for medical devices is projected to reach approximately USD 603 billion by the year 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing demand for healthcare services, and a growing emphasis on improving patient outcomes. The medical devices market encompasses a wide range of products, from diagnostic equipment and surgical instruments to wearable health monitors and implantable devices. As the healthcare industry continues to evolve, the demand for innovative and effective medical devices is expected to rise, contributing to the overall growth of the market. Additionally, factors such as an aging population, rising prevalence of chronic diseases, and increasing healthcare expenditure are likely to further fuel the expansion of the medical devices market. With ongoing research and development efforts, new and improved medical devices are being introduced, offering enhanced functionality and better patient care. The projected growth of the medical devices market underscores the importance of continued innovation and investment in this critical sector, which plays a vital role in advancing healthcare and improving the quality of life for patients worldwide.

| Report Metric | Details |

| Report Name | Cooling Vests for Surgeons Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Polar Products, Glacier Tek, Gentherm, CoolShirt Systems, Cardinal Health, Techniche, StaCool Vest, Steele Vest, Burlington (Beijing) Medical Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |