What is Global Geothermal Heat Pump Market?

The Global Geothermal Heat Pump Market refers to the worldwide industry focused on the production, distribution, and utilization of geothermal heat pumps. These systems leverage the stable temperatures found underground to provide heating and cooling for buildings. Unlike traditional HVAC systems that rely on external air temperatures, geothermal heat pumps use the earth's consistent subterranean temperatures to transfer heat. This makes them highly efficient and environmentally friendly, as they significantly reduce greenhouse gas emissions and energy consumption. The market encompasses various components, including the heat pumps themselves, installation services, and maintenance. It is driven by increasing awareness of environmental sustainability, rising energy costs, and government incentives promoting renewable energy sources. As more people and businesses seek to reduce their carbon footprint and energy expenses, the demand for geothermal heat pumps is expected to grow. The market is also influenced by technological advancements that improve the efficiency and affordability of these systems. Overall, the Global Geothermal Heat Pump Market represents a crucial segment of the broader renewable energy industry, contributing to global efforts to combat climate change and promote sustainable development.

Vertical Closed Loop, Horizontal Closed Loop, Open Loop, Others in the Global Geothermal Heat Pump Market:

In the Global Geothermal Heat Pump Market, there are several types of systems, each with its unique installation method and application. The Vertical Closed Loop system is one of the most common types. It involves drilling deep vertical wells into the ground, typically ranging from 100 to 400 feet deep. Pipes are inserted into these wells and connected to the heat pump. This system is ideal for areas with limited land space because it requires less horizontal area compared to other systems. The Vertical Closed Loop system is highly efficient and can be used in both residential and commercial buildings. On the other hand, the Horizontal Closed Loop system involves laying pipes in shallow trenches, usually 4 to 6 feet deep, over a larger horizontal area. This system is more suitable for properties with ample land space and is generally less expensive to install than the vertical system. However, it may be less efficient in areas with extreme temperature variations. The Open Loop system, another type, uses groundwater from a well or a body of water as the heat exchange fluid that circulates directly through the heat pump system. After circulating through the system, the water is returned to the ground or the water source. This system is highly efficient but requires a sufficient supply of clean water and is subject to local water regulations. Lastly, there are other less common systems, such as the Pond/Lake Loop, which uses a nearby body of water for heat exchange. This system is cost-effective if a suitable water source is available but is less common due to geographical limitations. Each of these systems has its advantages and disadvantages, and the choice of system depends on various factors, including land availability, local climate, and water resources. The diversity of these systems allows for flexibility in meeting the specific needs of different properties and regions, making geothermal heat pumps a versatile solution for sustainable heating and cooling.

Residential Buildings, Commercial Buildings in the Global Geothermal Heat Pump Market:

The usage of geothermal heat pumps in residential buildings has been steadily increasing due to their energy efficiency and environmental benefits. In residential settings, these systems provide a reliable and sustainable solution for heating and cooling homes. Homeowners are increasingly opting for geothermal heat pumps to reduce their energy bills and carbon footprint. The installation of these systems in residential buildings involves either a vertical or horizontal closed-loop system, depending on the available land space. Vertical systems are more common in urban areas with limited space, while horizontal systems are preferred in rural or suburban areas with more land. The consistent underground temperatures ensure that homes remain comfortable throughout the year, regardless of external weather conditions. Additionally, geothermal heat pumps can also provide hot water, further enhancing their utility in residential applications. In commercial buildings, the benefits of geothermal heat pumps are even more pronounced. Large commercial spaces, such as office buildings, shopping centers, and hotels, require significant amounts of energy for heating and cooling. Geothermal heat pumps offer a cost-effective and sustainable solution for these energy needs. The initial installation cost may be higher compared to traditional HVAC systems, but the long-term savings on energy bills and maintenance costs make them a worthwhile investment. Commercial buildings often use vertical closed-loop systems due to space constraints, but horizontal systems can also be used in larger properties. The use of geothermal heat pumps in commercial buildings also contributes to corporate sustainability goals and can enhance a company's reputation as an environmentally responsible entity. Moreover, government incentives and rebates for renewable energy installations further encourage the adoption of geothermal heat pumps in both residential and commercial buildings. Overall, the versatility and efficiency of geothermal heat pumps make them an attractive option for a wide range of applications, from single-family homes to large commercial complexes.

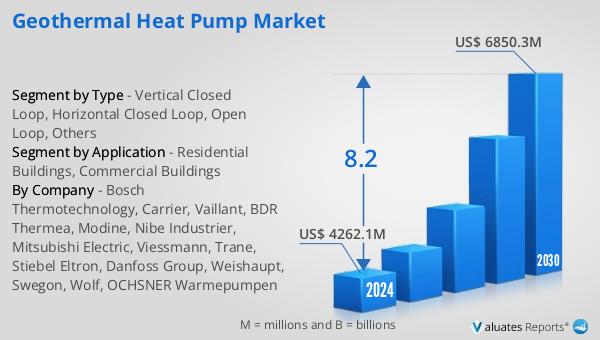

Global Geothermal Heat Pump Market Outlook:

The global Geothermal Heat Pump market is anticipated to grow significantly, reaching an estimated value of US$ 6850.3 million by 2030, up from US$ 4262.1 million in 2024, with a compound annual growth rate (CAGR) of 8.2% between 2024 and 2030. The market is dominated by five major manufacturers: Bosch Thermotechnology, Carrier, BDR Thermea, Vaillant, and Nibe Industrier, which collectively account for over 45% of the market share. Bosch Thermotechnology leads the market with approximately 10% share. Geographically, Europe holds the largest market share at over 35%, followed by North America and China, with shares of about 30% and 12%, respectively. In terms of product types, the Vertical Closed Loop system occupies the largest share of the total market, accounting for more than 45%. When it comes to product applications, Commercial Buildings dominate the market, making up about 60% of the total market share. This data highlights the significant role of geothermal heat pumps in the commercial sector and the preference for vertical closed-loop systems due to their efficiency and suitability for various applications. The market's growth is driven by increasing awareness of environmental sustainability, rising energy costs, and government incentives promoting renewable energy sources. As more businesses and homeowners seek to reduce their carbon footprint and energy expenses, the demand for geothermal heat pumps is expected to continue its upward trajectory.

| Report Metric | Details |

| Report Name | Geothermal Heat Pump Market |

| Accounted market size in 2024 | an estimated US$ 4262.1 million |

| Forecasted market size in 2030 | US$ 6850.3 million |

| CAGR | 8.2% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bosch Thermotechnology, Carrier, Vaillant, BDR Thermea, Modine, Nibe Industrier, Mitsubishi Electric, Viessmann, Trane, Stiebel Eltron, Danfoss Group, Weishaupt, Swegon, Wolf, OCHSNER Warmepumpen |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |