What is Global Smoke Alarm Market?

The Global Smoke Alarm Market refers to the worldwide industry involved in the production, distribution, and sale of smoke alarms. Smoke alarms are essential safety devices designed to detect smoke and alert occupants of a building to the presence of a fire, thereby providing an early warning that can save lives and minimize property damage. The market encompasses various types of smoke alarms, including photoelectric, ionization, and dual sensor alarms, each with distinct detection mechanisms and applications. The demand for smoke alarms is driven by stringent fire safety regulations, increasing awareness about fire safety, and the growing need for advanced fire detection systems in residential, commercial, industrial, and public utility sectors. The market is characterized by the presence of several key manufacturers who offer a range of products to meet diverse consumer needs. As fire safety continues to be a critical concern globally, the smoke alarm market is expected to witness steady growth, driven by technological advancements and the implementation of stricter fire safety standards.

Photoelectric Smoke Alarms, Ionization Smoke Alarms, Dual Sensor Smoke Alarm in the Global Smoke Alarm Market:

Photoelectric smoke alarms, ionization smoke alarms, and dual sensor smoke alarms are the primary categories within the Global Smoke Alarm Market. Photoelectric smoke alarms use a light source and a light sensor to detect smoke. When smoke enters the chamber, it scatters the light, which triggers the alarm. These alarms are particularly effective at detecting smoldering fires, which produce a lot of smoke but less heat. They are less prone to false alarms from cooking fumes or steam, making them suitable for kitchens and bathrooms. Ionization smoke alarms, on the other hand, use a small amount of radioactive material to ionize the air in the sensing chamber. When smoke enters the chamber, it disrupts the ionization process, causing the alarm to sound. These alarms are more responsive to flaming fires, which produce less smoke but more heat. However, they are more susceptible to false alarms from cooking and steam. Dual sensor smoke alarms combine both photoelectric and ionization technologies, providing comprehensive detection of both smoldering and flaming fires. This combination enhances the reliability and effectiveness of the alarm, making it a preferred choice for many consumers. The Global Smoke Alarm Market offers a variety of these alarms to cater to different needs and preferences, ensuring that there is a suitable option for every environment.

Commercial, Industrial, Government & Public Utility, Residential in the Global Smoke Alarm Market:

The usage of smoke alarms in the Global Smoke Alarm Market spans across various sectors, including commercial, industrial, government and public utility, and residential areas. In commercial settings, smoke alarms are crucial for protecting businesses, employees, and customers. They are installed in offices, retail stores, hotels, and restaurants to provide early warning in case of a fire, ensuring timely evacuation and minimizing potential losses. Industrial applications of smoke alarms are equally important, as factories, warehouses, and manufacturing plants are often filled with flammable materials and machinery that can pose significant fire hazards. Smoke alarms in these environments help detect fires early, allowing for prompt action to prevent catastrophic damage and ensure the safety of workers. Government and public utility buildings, such as schools, hospitals, and public offices, also rely heavily on smoke alarms to safeguard the lives of occupants and maintain public safety. These buildings often have high occupancy rates, making early fire detection and evacuation critical. In residential areas, smoke alarms are essential for protecting homes and families. They are typically installed in bedrooms, hallways, and living areas to provide continuous monitoring and early warning in case of a fire. The widespread adoption of smoke alarms in residential settings is driven by fire safety regulations and the growing awareness of the importance of fire prevention. Overall, the Global Smoke Alarm Market plays a vital role in enhancing fire safety across various sectors, contributing to the protection of lives and property worldwide.

Global Smoke Alarm Market Outlook:

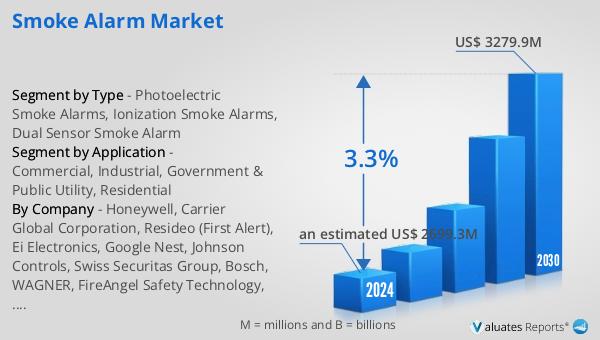

The global Smoke Alarm market is projected to reach US$ 3279.9 million by 2030 from an estimated US$ 2699.3 million in 2024 at a CAGR of 3.3% during 2024 and 2030. The global key manufacturers of smoke alarms include BRK Brands, Kidde, Honeywell Security, Tyco, Johnson Controls, Halma, Hochiki, Sprue Aegis, Xtralis, Siemens, Ei Electronics, Nohmi Bosai, and Panasonic, with about 54% market shares. In terms of its product categories, photoelectric smoke alarms hold the largest market share with 76%, followed by dual sensor smoke alarms. These manufacturers are at the forefront of innovation, continuously developing advanced smoke detection technologies to meet the evolving needs of consumers. The dominance of photoelectric smoke alarms in the market highlights their effectiveness in detecting smoldering fires, which are common in residential and commercial settings. Dual sensor smoke alarms, with their combined photoelectric and ionization technologies, offer enhanced detection capabilities, making them a popular choice for comprehensive fire safety. The steady growth of the smoke alarm market is a testament to the increasing emphasis on fire safety and the continuous efforts of manufacturers to provide reliable and efficient smoke detection solutions.

| Report Metric | Details |

| Report Name | Smoke Alarm Market |

| Accounted market size in 2024 | an estimated US$ 2699.3 million |

| Forecasted market size in 2030 | US$ 3279.9 million |

| CAGR | 3.3% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Honeywell, Carrier Global Corporation, Resideo (First Alert), Ei Electronics, Google Nest, Johnson Controls, Swiss Securitas Group, Bosch, WAGNER, FireAngel Safety Technology, ABB (Busch-jaeger), Schneider Electric, Halma, Siemens, Legrand, Smartwares, ABUS, Panasonic Fire & Security, Hochiki, Nittan Group, Zeta Alarms, Elotec, Eaton, Fireguard, Fireblitz (FireHawk), Inim Electronics, Hugo Brennenstuhl GmbH, SOMFY, eQ-3 (Homematic IP), Nohmi Bosai Limited, Minimax, Patol, FARE, Jalo Helsinki, QUNDIS GmbH, Humantechnik GmbH, X-Sense, Shenzhen Heiman Technology, ESYLUX, CPF Industriale, Chacon, Nedis, HIKVISION, Innohome Oy, Actulux A/S, D-Link, frient, Develco Products A/S, Gira, Gewiss, Delta Dore, Loxone Electronics GmbH, Neol S.A.S, DMTech Ltd, Jockel, LUPUS Electronics, TELENOT, Olympia Electronics SA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |