What is Global High Pressure Pumps Market?

The Global High Pressure Pumps Market refers to the worldwide industry focused on the production, distribution, and utilization of high-pressure pumps. These pumps are designed to generate a significant amount of pressure to move fluids through various systems and applications. High-pressure pumps are essential in numerous industries, including oil and gas, manufacturing, and water treatment, due to their ability to handle demanding tasks that require high levels of pressure. The market encompasses a wide range of pump types, including centrifugal, reciprocating, and diaphragm pumps, each suited for specific applications and operational requirements. The growth of this market is driven by the increasing demand for efficient and reliable pumping solutions in industrial processes, the need for advanced water treatment systems, and the expansion of the oil and gas sector. Technological advancements and innovations in pump design and materials also contribute to the market's development, offering improved performance, energy efficiency, and durability. As industries continue to evolve and seek more efficient ways to manage fluid dynamics, the Global High Pressure Pumps Market is expected to experience sustained growth and diversification.

in the Global High Pressure Pumps Market:

High-pressure pumps come in various types, each tailored to meet the specific needs of different customers in the Global High Pressure Pumps Market. Centrifugal pumps are among the most common types, known for their ability to handle large volumes of fluid with moderate pressure. They are widely used in applications such as water supply, irrigation, and industrial processes where continuous flow is essential. Reciprocating pumps, on the other hand, are designed to deliver high pressure with precise control, making them ideal for applications requiring accurate dosing and high-pressure delivery, such as in chemical processing and oil and gas industries. Diaphragm pumps are another type, known for their ability to handle corrosive and abrasive fluids without compromising performance. These pumps are often used in wastewater treatment, chemical processing, and food and beverage industries. Additionally, there are gear pumps, which are positive displacement pumps that provide a steady flow and are commonly used in hydraulic systems and lubrication applications. Screw pumps, another type of positive displacement pump, are known for their ability to handle viscous fluids and are often used in oil and gas, marine, and industrial applications. Each type of high-pressure pump offers unique advantages and is selected based on factors such as fluid type, pressure requirements, flow rate, and application-specific needs. Customers in the Global High Pressure Pumps Market benefit from a wide range of options, allowing them to choose the most suitable pump for their specific requirements, ensuring optimal performance and efficiency in their operations.

Industrial, Green Houses, Residential, Others in the Global High Pressure Pumps Market:

High-pressure pumps are utilized in various areas, including industrial, greenhouses, residential, and other applications, each with distinct requirements and benefits. In industrial settings, high-pressure pumps are essential for processes such as cleaning, cutting, and material handling. They are used in industries like manufacturing, automotive, and aerospace to ensure efficient and precise operations. For example, high-pressure water jets are employed for cutting metals and other materials with high precision, while high-pressure cleaning systems are used to maintain equipment and facilities. In greenhouses, high-pressure pumps play a crucial role in irrigation and misting systems, providing the necessary pressure to distribute water and nutrients evenly to plants. This helps in maintaining optimal growing conditions and improving crop yields. In residential applications, high-pressure pumps are used in pressure washing systems for cleaning driveways, patios, and vehicles, as well as in boosting water pressure for household water supply systems. They ensure efficient water distribution and enhance the overall quality of life for homeowners. Other applications of high-pressure pumps include firefighting, where they provide the necessary pressure to deliver water to high-rise buildings and remote areas, and in the marine industry, where they are used for ballast water treatment and hull cleaning. The versatility and reliability of high-pressure pumps make them indispensable in a wide range of applications, contributing to improved efficiency, safety, and productivity across various sectors.

Global High Pressure Pumps Market Outlook:

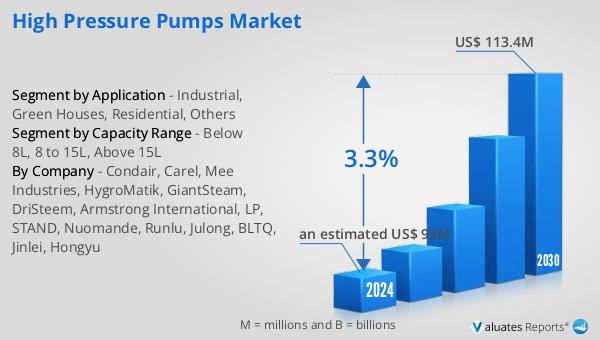

The global High Pressure Pumps market is anticipated to grow significantly, with projections indicating it will reach US$ 113.4 million by 2030, up from an estimated US$ 93 million in 2024, reflecting a compound annual growth rate (CAGR) of 3.3% between 2024 and 2030. Key players in the market include Condair, Carel, Mee Industries, HygroMatik, GiantSteam, and DriSteem, collectively accounting for approximately 35% of the market share. Europe stands out as the largest market, holding a share exceeding 27%. The industrial sector is the most prominent application area, representing over 52% of the market share. These figures highlight the significant role of high-pressure pumps in various industrial processes and the strong presence of leading companies driving innovation and growth in the market. The steady growth in demand for high-pressure pumps across different regions and industries underscores the importance of these pumps in enhancing operational efficiency and meeting the evolving needs of customers.

| Report Metric | Details |

| Report Name | High Pressure Pumps Market |

| Accounted market size in 2024 | an estimated US$ 93 in million |

| Forecasted market size in 2030 | US$ 113.4 million |

| CAGR | 3.3% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Capacity Range |

|

| Segment by Application |

|

| By Region |

|

| By Company | Condair, Carel, Mee Industries, HygroMatik, GiantSteam, DriSteem, Armstrong International, LP, STAND, Nuomande, Runlu, Julong, BLTQ, Jinlei, Hongyu |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |