What is Global Hollow Fiber Dialyzer Market?

The Global Hollow Fiber Dialyzer Market refers to the worldwide industry focused on the production and distribution of hollow fiber dialyzers, which are essential components in hemodialysis treatment. Hemodialysis is a medical procedure used to treat patients with kidney failure by filtering waste products and excess fluids from the blood. Hollow fiber dialyzers are preferred due to their efficient filtration capabilities and biocompatibility. These dialyzers consist of numerous tiny, hollow fibers that act as semi-permeable membranes, allowing for the selective removal of toxins while retaining essential blood components. The market encompasses various segments, including different types of membranes, applications in healthcare settings, and geographical regions. The demand for hollow fiber dialyzers is driven by the increasing prevalence of chronic kidney diseases, advancements in dialysis technology, and the growing aging population. As healthcare systems worldwide strive to improve patient outcomes and reduce treatment costs, the Global Hollow Fiber Dialyzer Market continues to expand, offering innovative solutions for effective kidney care.

Low Flux Membranes, High Flux Membranes in the Global Hollow Fiber Dialyzer Market:

Low Flux Membranes and High Flux Membranes are two primary types of membranes used in the Global Hollow Fiber Dialyzer Market, each with distinct characteristics and applications. Low Flux Membranes are designed with smaller pore sizes, which allow for the selective removal of smaller molecules such as urea and creatinine from the blood. These membranes are typically used in conventional hemodialysis treatments where the primary goal is to remove waste products without significantly altering the patient's fluid balance. Low Flux Membranes are known for their stability and reliability, making them a preferred choice for patients with stable hemodynamic conditions. On the other hand, High Flux Membranes have larger pore sizes, enabling the removal of larger molecules such as beta-2 microglobulin and middle molecules, which are often associated with long-term complications in dialysis patients. High Flux Membranes are used in high-efficiency hemodialysis and hemodiafiltration treatments, which aim to provide more comprehensive clearance of toxins and better mimic the natural kidney function. These membranes are particularly beneficial for patients with higher toxin loads or those experiencing dialysis-related complications. The choice between Low Flux and High Flux Membranes depends on various factors, including the patient's clinical condition, treatment goals, and the healthcare provider's preferences. Both types of membranes play a crucial role in the Global Hollow Fiber Dialyzer Market, offering tailored solutions to meet the diverse needs of dialysis patients. As technology advances, the development of new membrane materials and designs continues to enhance the performance and safety of hollow fiber dialyzers, contributing to improved patient outcomes and quality of life.

Hospitals, Dialysis Centers, Others in the Global Hollow Fiber Dialyzer Market:

The usage of Global Hollow Fiber Dialyzer Market products spans across various healthcare settings, including hospitals, dialysis centers, and other medical facilities. In hospitals, hollow fiber dialyzers are used for both acute and chronic dialysis treatments. Acute dialysis is often required for patients with sudden kidney failure due to conditions such as severe infections, drug overdoses, or traumatic injuries. Hospitals are equipped with advanced dialysis machines and trained medical staff to provide immediate and intensive care for these patients. Chronic dialysis, on the other hand, is administered to patients with end-stage renal disease (ESRD) who require long-term dialysis support. Hospitals offer comprehensive dialysis services, including pre-dialysis assessments, dialysis sessions, and post-dialysis monitoring, ensuring that patients receive holistic care. Dialysis centers, which are specialized facilities dedicated to providing dialysis treatments, play a significant role in the Global Hollow Fiber Dialyzer Market. These centers cater to a large number of chronic kidney disease patients who require regular dialysis sessions, typically three times a week. Dialysis centers are equipped with state-of-the-art dialysis machines and staffed by nephrologists, dialysis nurses, and technicians who specialize in renal care. The use of hollow fiber dialyzers in these centers ensures efficient and effective removal of toxins, helping patients maintain their health and quality of life. Additionally, dialysis centers often provide education and support services to help patients manage their condition and adhere to their treatment plans. Other medical facilities, such as outpatient clinics and home dialysis programs, also utilize hollow fiber dialyzers to provide flexible and convenient dialysis options for patients. Home dialysis, in particular, has gained popularity due to its ability to offer patients greater independence and control over their treatment schedules. Patients who opt for home dialysis receive training on how to perform dialysis procedures safely and effectively using portable dialysis machines and hollow fiber dialyzers. This approach not only improves patient satisfaction but also reduces the burden on healthcare facilities. Overall, the Global Hollow Fiber Dialyzer Market plays a vital role in supporting the diverse needs of dialysis patients across various healthcare settings, contributing to better health outcomes and enhanced quality of life.

Global Hollow Fiber Dialyzer Market Outlook:

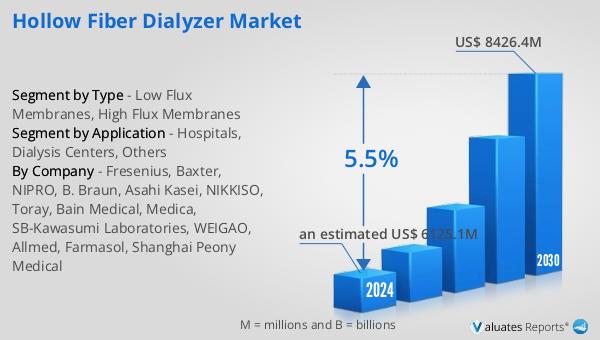

The global Hollow Fiber Dialyzer market is anticipated to grow significantly, reaching an estimated value of US$ 8426.4 million by 2030, up from US$ 6125.1 million in 2024, with a compound annual growth rate (CAGR) of 5.5% between 2024 and 2030. The market is dominated by the top three players, who collectively hold approximately 53% of the market share. North America stands as the largest market, accounting for about 33% of the total share, followed by the Asia-Pacific region and Europe, which hold shares of 31% and 28%, respectively. This growth is driven by factors such as the increasing prevalence of chronic kidney diseases, advancements in dialysis technology, and the growing aging population. The market's expansion is also supported by the rising demand for efficient and effective dialysis treatments, as well as the continuous development of innovative hollow fiber dialyzer products. As healthcare systems worldwide strive to improve patient outcomes and reduce treatment costs, the Global Hollow Fiber Dialyzer Market is poised for sustained growth, offering promising opportunities for industry players and stakeholders.

| Report Metric | Details |

| Report Name | Hollow Fiber Dialyzer Market |

| Accounted market size in 2024 | an estimated US$ 6125.1 million |

| Forecasted market size in 2030 | US$ 8426.4 million |

| CAGR | 5.5% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Fresenius, Baxter, NIPRO, B. Braun, Asahi Kasei, NIKKISO, Toray, Bain Medical, Medica, SB-Kawasumi Laboratories, WEIGAO, Allmed, Farmasol, Shanghai Peony Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |