What is Global Fishing and Aquaculture Nets Market?

The Global Fishing and Aquaculture Nets Market encompasses the production, distribution, and utilization of nets specifically designed for fishing and aquaculture activities. These nets are essential tools in the fishing industry, used to capture fish and other aquatic organisms from natural water bodies like oceans, rivers, and lakes. In aquaculture, nets are employed to create controlled environments for breeding, rearing, and harvesting fish and other marine species. The market for these nets is driven by the increasing demand for seafood, advancements in fishing techniques, and the expansion of aquaculture practices worldwide. The nets are made from various materials, including nylon, polyethylene, and polyester, each offering different levels of durability, flexibility, and resistance to environmental factors. The market also includes a range of net types, such as gill nets, trawl nets, and seine nets, each designed for specific fishing methods and aquatic conditions. The Global Fishing and Aquaculture Nets Market is a critical component of the broader fishing and aquaculture industries, supporting sustainable practices and contributing to the global food supply chain.

Fishing Nets, Aquaculture Nets in the Global Fishing and Aquaculture Nets Market:

Fishing nets are essential tools in the fishing industry, designed to capture fish and other aquatic organisms from natural water bodies. These nets come in various types, including gill nets, trawl nets, and seine nets, each tailored for specific fishing methods and aquatic conditions. Gill nets, for example, are vertical panels of netting that trap fish by their gills, while trawl nets are large, funnel-shaped nets towed behind boats to capture fish in bulk. Seine nets, on the other hand, are used to encircle and capture schools of fish. The materials used in fishing nets, such as nylon, polyethylene, and polyester, are chosen for their durability, flexibility, and resistance to environmental factors like UV radiation and saltwater corrosion. Aquaculture nets, on the other hand, are used to create controlled environments for breeding, rearing, and harvesting fish and other marine species. These nets are designed to withstand the rigors of aquaculture operations, including exposure to water currents, biofouling, and predator attacks. They are also made from materials that are resistant to wear and tear, ensuring long-term use and minimal maintenance. The Global Fishing and Aquaculture Nets Market is driven by the increasing demand for seafood, advancements in fishing techniques, and the expansion of aquaculture practices worldwide. As the global population continues to grow, the need for sustainable and efficient methods of seafood production becomes more critical. Fishing and aquaculture nets play a vital role in meeting this demand, supporting the livelihoods of millions of people involved in the fishing and aquaculture industries.

Individual Application, Commercial Application in the Global Fishing and Aquaculture Nets Market:

The Global Fishing and Aquaculture Nets Market finds applications in both individual and commercial settings. In individual applications, fishing nets are used by recreational and subsistence fishers who rely on fishing as a source of food and livelihood. These individuals often use smaller, more portable nets that are easy to handle and maintain. Recreational fishers, for example, may use cast nets or dip nets to catch fish for personal consumption or sport. Subsistence fishers, on the other hand, may use gill nets or seine nets to capture fish in larger quantities to feed their families or sell in local markets. The use of fishing nets in individual applications is often influenced by local fishing traditions, regulations, and the availability of resources. In commercial applications, fishing and aquaculture nets are used by large-scale fishing operations and aquaculture farms to capture and cultivate fish and other marine species on a much larger scale. Commercial fishing operations use a variety of nets, including trawl nets, purse seine nets, and drift nets, to capture fish in bulk and supply the global seafood market. These operations often require specialized equipment and techniques to ensure efficient and sustainable fishing practices. Aquaculture farms, on the other hand, use nets to create controlled environments for breeding, rearing, and harvesting fish and other marine species. These nets are designed to withstand the rigors of aquaculture operations, including exposure to water currents, biofouling, and predator attacks. The use of nets in commercial applications is driven by the increasing demand for seafood, advancements in fishing and aquaculture technologies, and the need for sustainable and efficient methods of seafood production. The Global Fishing and Aquaculture Nets Market plays a crucial role in supporting the livelihoods of millions of people involved in the fishing and aquaculture industries, contributing to the global food supply chain, and promoting sustainable fishing and aquaculture practices.

Global Fishing and Aquaculture Nets Market Outlook:

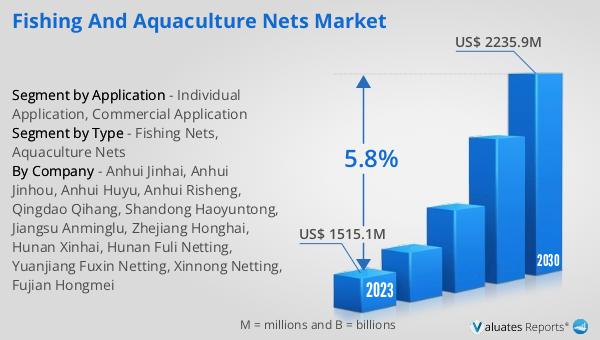

The global Fishing and Aquaculture Nets market was valued at US$ 1515.1 million in 2023 and is anticipated to reach US$ 2235.9 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. This significant growth reflects the increasing demand for seafood and the expansion of aquaculture practices worldwide. The market's growth is also driven by advancements in fishing techniques and the development of more durable and efficient net materials. As the global population continues to grow, the need for sustainable and efficient methods of seafood production becomes more critical. The Global Fishing and Aquaculture Nets Market plays a vital role in meeting this demand, supporting the livelihoods of millions of people involved in the fishing and aquaculture industries, and contributing to the global food supply chain. The market's growth is also supported by government initiatives and regulations aimed at promoting sustainable fishing and aquaculture practices. The increasing awareness of the environmental impact of overfishing and the need for sustainable seafood production is also driving the demand for more efficient and environmentally friendly fishing and aquaculture nets. The Global Fishing and Aquaculture Nets Market is expected to continue its growth trajectory, driven by the increasing demand for seafood, advancements in fishing and aquaculture technologies, and the need for sustainable and efficient methods of seafood production.

| Report Metric | Details |

| Report Name | Fishing and Aquaculture Nets Market |

| Accounted market size in 2023 | US$ 1515.1 million |

| Forecasted market size in 2030 | US$ 2235.9 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Anhui Jinhai, Anhui Jinhou, Anhui Huyu, Anhui Risheng, Qingdao Qihang, Shandong Haoyuntong, Jiangsu Anminglu, Zhejiang Honghai, Hunan Xinhai, Hunan Fuli Netting, Yuanjiang Fuxin Netting, Xinnong Netting, Fujian Hongmei |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |