What is Global Dental Biomaterial Tester Market?

The Global Dental Biomaterial Tester Market is a specialized segment within the broader medical device industry, focusing on the evaluation and testing of materials used in dental applications. These biomaterials include substances like dental implants, crowns, bridges, and other restorative materials that are used to replace or repair damaged teeth and oral structures. The market for dental biomaterial testers is driven by the need for high-quality, durable, and biocompatible materials that can withstand the mechanical stresses of the oral environment. These testers are essential for ensuring that dental materials meet stringent regulatory standards and perform effectively in clinical settings. The market encompasses a range of testing equipment designed to assess various properties of dental biomaterials, such as their mechanical strength, bonding capabilities, and resistance to wear and tear. As dental technology continues to advance, the demand for reliable and precise testing equipment is expected to grow, making the Global Dental Biomaterial Tester Market a critical component of the dental industry.

Bend Test, Bond Strength Test, Compression Test, Other in the Global Dental Biomaterial Tester Market:

In the Global Dental Biomaterial Tester Market, several key tests are conducted to evaluate the performance and durability of dental materials. The Bend Test is one such evaluation, where a sample material is subjected to bending forces to determine its flexibility and resistance to fracture. This test is crucial for materials used in dental bridges and crowns, which must endure significant bending stresses during chewing and biting. The Bond Strength Test assesses the adhesive properties of dental materials, ensuring that they can form strong and durable bonds with natural teeth and other dental structures. This test is particularly important for dental adhesives and cements, which must provide reliable bonding to prevent restoration failures. The Compression Test measures the ability of dental materials to withstand compressive forces, which are common in the oral environment. Materials used for dental implants and fillings must exhibit high compressive strength to maintain their integrity under the pressure of chewing. Other tests in the Global Dental Biomaterial Tester Market include fatigue testing, wear resistance testing, and biocompatibility assessments. Fatigue testing evaluates the long-term durability of dental materials by subjecting them to repeated loading cycles, simulating the stresses experienced over time in the mouth. Wear resistance testing examines how well materials can resist abrasion and wear, which is essential for maintaining the longevity of dental restorations. Biocompatibility assessments ensure that dental materials do not cause adverse reactions in the body, such as inflammation or allergic responses. These tests are vital for ensuring the safety and effectiveness of dental biomaterials, contributing to the overall quality of dental care. The comprehensive evaluation provided by these tests helps manufacturers develop and refine dental materials that meet the high standards required for clinical use. As a result, the Global Dental Biomaterial Tester Market plays a pivotal role in advancing dental technology and improving patient outcomes.

Hospital, Research and Development Centres, Others in the Global Dental Biomaterial Tester Market:

The Global Dental Biomaterial Tester Market finds extensive usage in various settings, including hospitals, research and development centers, and other healthcare facilities. In hospitals, dental biomaterial testers are used to evaluate the performance of materials used in dental procedures, such as implants, crowns, and bridges. These tests ensure that the materials meet the necessary standards for safety and effectiveness, providing patients with reliable and durable dental restorations. Hospitals rely on these testers to maintain high-quality dental care and to minimize the risk of complications associated with dental materials. In research and development centers, dental biomaterial testers are essential tools for developing new and innovative dental materials. Researchers use these testers to conduct a wide range of tests, including mechanical strength assessments, bonding evaluations, and biocompatibility studies. These tests provide valuable data that helps researchers understand the properties and performance of new materials, guiding the development of advanced dental products. The insights gained from these tests contribute to the creation of materials that offer improved durability, aesthetics, and biocompatibility, ultimately enhancing patient care. Other healthcare facilities, such as dental clinics and academic institutions, also utilize dental biomaterial testers for various purposes. Dental clinics use these testers to ensure that the materials they use in their practice meet the required standards, providing patients with high-quality dental restorations. Academic institutions use dental biomaterial testers for educational purposes, training future dental professionals in the evaluation and selection of dental materials. These testers provide hands-on experience and practical knowledge, preparing students for their careers in dentistry. Overall, the Global Dental Biomaterial Tester Market plays a crucial role in ensuring the quality and safety of dental materials used in various healthcare settings. By providing reliable and accurate testing, these testers contribute to the advancement of dental technology and the improvement of patient outcomes.

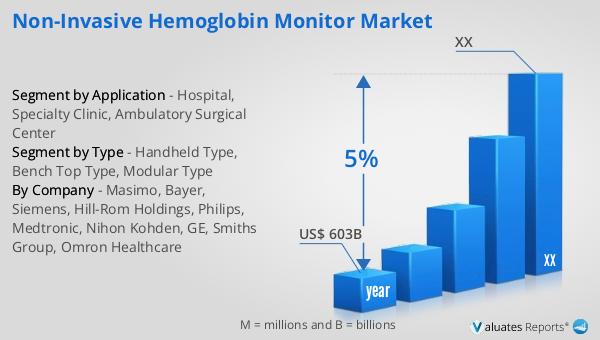

Global Dental Biomaterial Tester Market Outlook:

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This significant market size underscores the importance of medical devices in the healthcare industry, including the specialized segment of dental biomaterial testers. The steady growth rate reflects the ongoing advancements in medical technology and the increasing demand for high-quality healthcare solutions. As the medical device market expands, the need for reliable and precise testing equipment, such as dental biomaterial testers, becomes even more critical. These testers play a vital role in ensuring that dental materials meet stringent regulatory standards and perform effectively in clinical settings. The growth of the medical device market is driven by factors such as the aging population, rising prevalence of chronic diseases, and increasing healthcare expenditure. These trends highlight the importance of continuous innovation and development in the medical device industry, including the Global Dental Biomaterial Tester Market. By providing accurate and reliable testing, dental biomaterial testers contribute to the overall quality and safety of dental care, supporting the broader goals of the healthcare industry. The projected growth of the medical device market emphasizes the need for ongoing investment in research and development, ensuring that new and improved medical devices continue to meet the evolving needs of patients and healthcare providers.

| Report Metric | Details |

| Report Name | Dental Biomaterial Tester Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ADMET, MTS Systems, ZwickRoell, Rheolution, CellScale, Intertek Group, Applied Test Systems, Presto Group, TestResources, World Precision Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |