What is Global Hematology Analyzers & Systems Market?

The Global Hematology Analyzers & Systems Market is a crucial segment within the medical devices industry, focusing on the development and distribution of devices that analyze blood samples to diagnose various conditions. These analyzers are essential tools in medical laboratories and hospitals, providing critical data on blood cell counts, hemoglobin levels, and other vital parameters. The market encompasses a wide range of products, from basic manual devices to highly sophisticated automated systems. These devices are indispensable in diagnosing diseases such as anemia, leukemia, and other blood disorders. The market is driven by the increasing prevalence of these conditions, advancements in technology, and the growing demand for accurate and efficient diagnostic tools. Additionally, the rising awareness about the importance of early diagnosis and the expanding healthcare infrastructure in developing regions are contributing to the market's growth. The Global Hematology Analyzers & Systems Market is poised for significant expansion, reflecting the ongoing advancements in medical technology and the increasing need for precise diagnostic solutions.

Automatic Hematology Analyzers, Semiautomatic Hematology Analyzers in the Global Hematology Analyzers & Systems Market:

Automatic Hematology Analyzers are advanced devices designed to perform a wide range of tests on blood samples with minimal human intervention. These analyzers are equipped with sophisticated software and hardware that allow them to process large volumes of samples quickly and accurately. They can perform multiple tests simultaneously, including complete blood counts (CBC), white blood cell differentials, and reticulocyte counts. The automation reduces the risk of human error, ensures consistency in results, and enhances the overall efficiency of laboratory operations. These analyzers are particularly beneficial in high-throughput settings such as large hospitals and reference laboratories where the demand for rapid and accurate results is high. On the other hand, Semiautomatic Hematology Analyzers require some level of manual intervention. While they are capable of performing many of the same tests as their fully automated counterparts, they often require manual sample preparation and loading. These analyzers are typically more affordable and are suitable for smaller laboratories or clinics with lower sample volumes. They offer a balance between automation and cost, making them an attractive option for facilities with budget constraints. Both types of analyzers play a vital role in the Global Hematology Analyzers & Systems Market, catering to different segments of the healthcare industry based on their specific needs and resources. The choice between automatic and semiautomatic analyzers depends on various factors, including the volume of samples processed, the level of accuracy required, and the available budget. As technology continues to evolve, we can expect further advancements in both types of analyzers, enhancing their capabilities and expanding their applications in the medical field.

Hospital, Laboratory in the Global Hematology Analyzers & Systems Market:

In hospitals, hematology analyzers are indispensable tools used for diagnosing and monitoring a wide range of medical conditions. These devices are integrated into the hospital's laboratory infrastructure, enabling healthcare professionals to obtain critical information about a patient's blood composition quickly and accurately. For instance, in emergency departments, rapid blood analysis can be crucial for diagnosing conditions such as sepsis, anemia, and clotting disorders. The ability to obtain accurate results in a short time frame can significantly impact patient outcomes, allowing for timely and appropriate treatment interventions. In addition to emergency care, hematology analyzers are also used in routine check-ups and pre-surgical assessments to ensure that patients are in optimal health before undergoing any procedures. In laboratories, hematology analyzers are the backbone of diagnostic testing. These devices are used to perform a wide range of tests, from basic blood counts to more complex analyses such as flow cytometry and molecular diagnostics. Laboratories rely on these analyzers to provide accurate and reliable results, which are essential for diagnosing various medical conditions and monitoring treatment efficacy. The high throughput and automation capabilities of modern hematology analyzers enable laboratories to process large volumes of samples efficiently, reducing turnaround times and improving overall productivity. This is particularly important in large reference laboratories that handle samples from multiple healthcare facilities. The integration of advanced software and data management systems with hematology analyzers also enhances the ability to track and analyze patient data over time, providing valuable insights into disease progression and treatment outcomes. Overall, the usage of hematology analyzers in hospitals and laboratories is critical for delivering high-quality healthcare and improving patient outcomes.

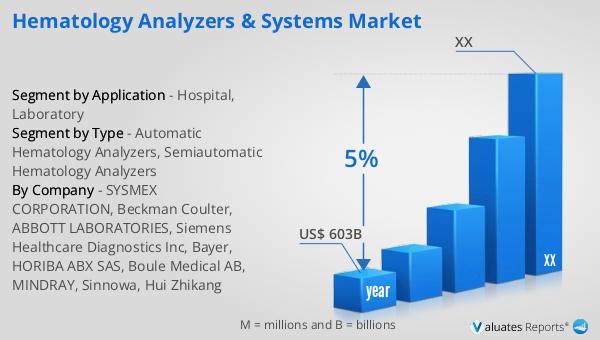

Global Hematology Analyzers & Systems Market Outlook:

According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This significant market size reflects the increasing demand for advanced medical technologies and diagnostic tools across the globe. The growth rate indicates a steady expansion driven by factors such as technological advancements, rising healthcare expenditures, and the growing prevalence of chronic diseases. The medical devices market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in modern healthcare. The continuous innovation in this field is expected to enhance the capabilities of medical devices, making them more efficient, accurate, and accessible. As a result, the market is poised for sustained growth, offering numerous opportunities for stakeholders, including manufacturers, healthcare providers, and patients.

| Report Metric | Details |

| Report Name | Hematology Analyzers & Systems Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | SYSMEX CORPORATION, Beckman Coulter, ABBOTT LABORATORIES, Siemens Healthcare Diagnostics Inc, Bayer, HORIBA ABX SAS, Boule Medical AB, MINDRAY, Sinnowa, Hui Zhikang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |