What is Global Shell of Optical Communication Device Market?

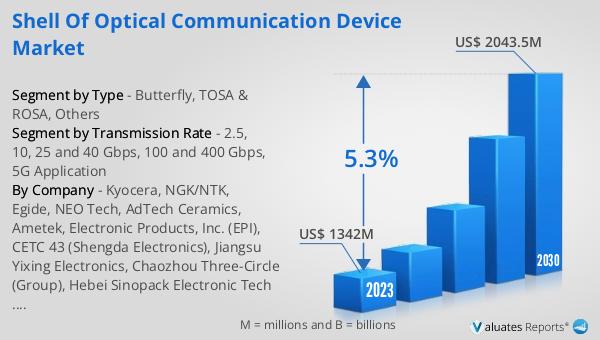

The global Shell of Optical Communication Device market is a rapidly evolving sector that plays a crucial role in the telecommunications industry. Optical communication devices are essential for transmitting data over long distances with minimal loss and high efficiency. These devices use light to carry information, making them faster and more reliable than traditional electrical communication methods. The market for these devices includes various components such as transceivers, amplifiers, and switches, all housed within protective shells to ensure durability and performance. The demand for optical communication devices is driven by the increasing need for high-speed internet, the expansion of data centers, and the growing adoption of cloud services. As technology advances, the market continues to innovate, offering more efficient and cost-effective solutions to meet the ever-growing data transmission needs. The global Shell of Optical Communication Device market was valued at US$ 1342 million in 2023 and is anticipated to reach US$ 2043.5 million by 2030, witnessing a CAGR of 5.3% during the forecast period 2024-2030. According to data from the Ministry of Industry and Information Technology of China, the cumulative revenue of telecommunications services in 2022 was 1.58 trillion, an increase of 8% over the previous year.

Butterfly, TOSA & ROSA, Others in the Global Shell of Optical Communication Device Market:

In the realm of the Global Shell of Optical Communication Device Market, various components play pivotal roles, including Butterfly, TOSA (Transmitter Optical Sub-Assembly), ROSA (Receiver Optical Sub-Assembly), and others. Butterfly packages are widely used in optical communication devices due to their compact size and high performance. These packages house laser diodes and photodiodes, which are essential for converting electrical signals into optical signals and vice versa. The compact design of Butterfly packages makes them ideal for use in dense network environments where space is a premium. TOSA, or Transmitter Optical Sub-Assembly, is another critical component in the optical communication device market. TOSAs are responsible for converting electrical signals into optical signals for transmission over fiber optic cables. They typically include a laser diode, a monitor photodiode, and other necessary components to ensure efficient signal transmission. TOSAs are used in various applications, including data centers, telecommunications networks, and enterprise networks, where high-speed data transmission is crucial. ROSA, or Receiver Optical Sub-Assembly, complements TOSA by converting incoming optical signals back into electrical signals. ROSAs typically include a photodiode, a transimpedance amplifier, and other components necessary for accurate signal reception. Like TOSAs, ROSAs are used in data centers, telecommunications networks, and other high-speed data transmission environments. Other components in the Global Shell of Optical Communication Device Market include optical amplifiers, switches, and multiplexers. Optical amplifiers are used to boost the strength of optical signals, allowing them to travel longer distances without degradation. Switches are essential for directing optical signals to their intended destinations, while multiplexers combine multiple optical signals into a single fiber for more efficient transmission. These components work together to create a robust and efficient optical communication network, capable of handling the increasing demands for high-speed data transmission. As technology continues to advance, the Global Shell of Optical Communication Device Market will likely see further innovations, leading to even more efficient and cost-effective solutions for data transmission.

in the Global Shell of Optical Communication Device Market:

The Global Shell of Optical Communication Device Market finds applications across various sectors, each leveraging the high-speed and reliable data transmission capabilities of optical communication devices. One of the primary applications is in telecommunications networks, where these devices are used to transmit data over long distances with minimal loss. Telecommunications companies rely on optical communication devices to provide high-speed internet, voice, and video services to their customers. The ability to transmit large amounts of data quickly and efficiently is crucial for maintaining the quality of service and meeting the growing demand for bandwidth. Another significant application of optical communication devices is in data centers. Data centers are the backbone of the internet, housing vast amounts of data and supporting numerous online services. Optical communication devices are used in data centers to connect servers, storage systems, and networking equipment, enabling fast and reliable data transfer. The high-speed capabilities of optical communication devices are essential for data centers to handle the increasing volume of data generated by cloud computing, big data analytics, and other data-intensive applications. Enterprise networks also benefit from the use of optical communication devices. Businesses of all sizes rely on high-speed data transmission for their daily operations, from internal communications to customer interactions. Optical communication devices enable enterprises to build robust and efficient networks that support their business needs. These devices are used in various applications, including local area networks (LANs), wide area networks (WANs), and metropolitan area networks (MANs), providing the speed and reliability required for modern business operations. Additionally, the Global Shell of Optical Communication Device Market finds applications in the healthcare sector. Medical facilities use optical communication devices to transmit large volumes of data quickly and securely. This is particularly important for telemedicine, where high-speed data transmission is necessary for real-time consultations and remote diagnostics. Optical communication devices also support the transmission of medical imaging data, enabling healthcare professionals to share and analyze images efficiently. The financial sector is another area where optical communication devices are widely used. Financial institutions rely on high-speed data transmission for trading, transactions, and other critical operations. Optical communication devices provide the speed and reliability needed to ensure that financial data is transmitted quickly and securely, minimizing the risk of delays or data loss. In summary, the Global Shell of Optical Communication Device Market serves a wide range of applications, from telecommunications and data centers to enterprise networks, healthcare, and finance. The high-speed and reliable data transmission capabilities of optical communication devices make them indispensable in today's data-driven world. As the demand for bandwidth continues to grow, the market for these devices is expected to expand, driving further innovation and development in the field.

Global Shell of Optical Communication Device Market Outlook:

The global Shell of Optical Communication Device market was valued at US$ 1342 million in 2023 and is anticipated to reach US$ 2043.5 million by 2030, witnessing a CAGR of 5.3% during the forecast period 2024-2030. According to data from the Ministry of Industry and Information Technology of China, the cumulative revenue of telecommunications services in 2022 was 1.58 trillion, an increase of 8% over the previous year. This growth reflects the increasing demand for high-speed internet and data services, driven by the proliferation of digital technologies and the expansion of the internet of things (IoT). The rise in data consumption, fueled by the growing use of smartphones, streaming services, and cloud computing, has necessitated the development of more efficient and reliable optical communication devices. As a result, the market for these devices is expected to continue its upward trajectory, supported by ongoing advancements in technology and the increasing need for high-speed data transmission. The global Shell of Optical Communication Device market is poised for significant growth, driven by the ever-increasing demand for bandwidth and the continuous evolution of digital technologies.

| Report Metric | Details |

| Report Name | Shell of Optical Communication Device Market |

| Accounted market size in 2023 | US$ 1342 million |

| Forecasted market size in 2030 | US$ 2043.5 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Transmission Rate |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Kyocera, NGK/NTK, Egide, NEO Tech, AdTech Ceramics, Ametek, Electronic Products, Inc. (EPI), CETC 43 (Shengda Electronics), Jiangsu Yixing Electronics, Chaozhou Three-Circle (Group), Hebei Sinopack Electronic Tech & CETC 13, Beijing BDStar Navigation (Glead), Fujian Minhang Electronics, RF Materials (METALLIFE), CETC 55, Qingdao Kerry Electronics, Hebei Dingci Electronic, Shanghai Xintao Weixing Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |