What is Global Spinning Flow Formed Hubs Market?

The Global Spinning Flow Formed Hubs Market is a specialized segment within the automotive industry that focuses on the production and distribution of hubs created through a process known as flow forming. This technique involves spinning a preform or blank at high speeds while applying pressure to shape it into the desired hub form. The result is a product that boasts superior strength, durability, and precision compared to traditionally manufactured hubs. These hubs are essential components in various types of vehicles, providing the necessary support and stability for wheels. The market for these hubs is driven by the increasing demand for high-performance and lightweight automotive components, which contribute to better fuel efficiency and enhanced vehicle performance. As automotive technology continues to advance, the need for more reliable and efficient hubs is expected to grow, making the Global Spinning Flow Formed Hubs Market a critical area of focus for manufacturers and suppliers alike.

Casting Spinning Hubs, Forging Spinning Hubs in the Global Spinning Flow Formed Hubs Market:

Casting Spinning Hubs and Forging Spinning Hubs are two primary types of hubs within the Global Spinning Flow Formed Hubs Market, each with distinct manufacturing processes and characteristics. Casting Spinning Hubs are produced by pouring molten metal into a mold, allowing it to cool and solidify into the desired shape. This method is cost-effective and suitable for mass production, making it a popular choice for standard vehicle applications. However, casting can sometimes result in inconsistencies in the material's density, which may affect the hub's overall strength and durability. On the other hand, Forging Spinning Hubs are created by heating a metal blank and then deforming it under high pressure to achieve the final shape. This process aligns the metal's grain structure, resulting in a denser and more robust product. Forging is typically more expensive and time-consuming than casting, but it produces hubs with superior mechanical properties, making them ideal for high-performance and heavy-duty applications. Both types of hubs undergo the flow forming process, which further enhances their strength and precision by refining the material's microstructure and ensuring uniform thickness. The choice between casting and forging depends on various factors, including the intended use of the hub, cost considerations, and performance requirements. In the context of the Global Spinning Flow Formed Hubs Market, manufacturers must carefully evaluate these factors to determine the most suitable production method for their specific needs.

Ordinary Car, Sports Car, Racing, Others in the Global Spinning Flow Formed Hubs Market:

The usage of Global Spinning Flow Formed Hubs Market extends across various types of vehicles, including ordinary cars, sports cars, racing vehicles, and others. In ordinary cars, these hubs play a crucial role in ensuring smooth and reliable wheel rotation, contributing to overall vehicle safety and performance. The enhanced strength and durability of flow-formed hubs make them a preferred choice for everyday vehicles, where longevity and cost-effectiveness are key considerations. For sports cars, the demand for high-performance components is paramount. Flow-formed hubs offer the perfect balance of lightweight construction and superior strength, allowing sports cars to achieve better acceleration, handling, and fuel efficiency. The precision and reliability of these hubs are essential for maintaining optimal performance under various driving conditions. In the racing industry, the stakes are even higher. Racing vehicles require components that can withstand extreme stress and high speeds. Flow-formed hubs provide the necessary durability and precision, ensuring that the wheels remain securely attached and perform flawlessly during races. The ability to produce hubs with consistent quality and performance is critical in this high-stakes environment. Beyond ordinary cars, sports cars, and racing vehicles, flow-formed hubs are also used in other applications, such as commercial vehicles, motorcycles, and specialized equipment. In commercial vehicles, the need for robust and reliable components is crucial for handling heavy loads and long-distance travel. Motorcycles benefit from the lightweight and strong nature of flow-formed hubs, which contribute to better handling and performance. Specialized equipment, such as agricultural machinery and industrial vehicles, also relies on the durability and precision of these hubs to operate efficiently. Overall, the versatility and superior performance of flow-formed hubs make them an invaluable component across a wide range of vehicles and applications.

Global Spinning Flow Formed Hubs Market Outlook:

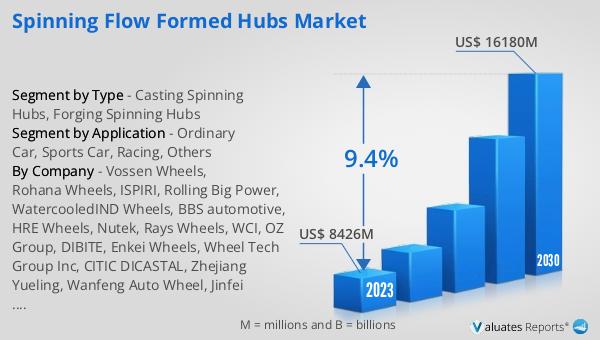

The global Spinning Flow Formed Hubs market was valued at US$ 8426 million in 2023 and is anticipated to reach US$ 16180 million by 2030, witnessing a CAGR of 9.4% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-performance and lightweight automotive components that enhance vehicle efficiency and performance. The market's expansion is driven by advancements in automotive technology, which require more reliable and durable hubs to support the evolving needs of modern vehicles. As manufacturers continue to innovate and improve the flow forming process, the quality and performance of these hubs are expected to reach new heights, further fueling market growth. The rising popularity of electric and hybrid vehicles, which demand lightweight and efficient components, also contributes to the market's positive outlook. Additionally, the growing emphasis on sustainability and reducing carbon emissions in the automotive industry aligns with the benefits of flow-formed hubs, as they help improve fuel efficiency and reduce overall vehicle weight. As a result, the Global Spinning Flow Formed Hubs Market is poised for substantial growth in the coming years, offering numerous opportunities for manufacturers, suppliers, and stakeholders to capitalize on this expanding market.

| Report Metric | Details |

| Report Name | Spinning Flow Formed Hubs Market |

| Accounted market size in 2023 | US$ 8426 million |

| Forecasted market size in 2030 | US$ 16180 million |

| CAGR | 9.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Vossen Wheels, Rohana Wheels, ISPIRI, Rolling Big Power, WatercooledIND Wheels, BBS automotive, HRE Wheels, Nutek, Rays Wheels, WCI, OZ Group, DIBITE, Enkei Wheels, Wheel Tech Group Inc, CITIC DICASTAL, Zhejiang Yueling, Wanfeng Auto Wheel, Jinfei Holding Group, Lizhong Wheel Group, Kunshan Liufeng Machinery, Zhongnan Aluminum Wheel, Hongtian Automotive Technology, Advanti Racing (YHI Group) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |