What is Global High Pressure Filtration Equipment Market?

The global High Pressure Filtration Equipment market is a specialized segment within the broader filtration industry, focusing on equipment designed to operate under high pressure conditions. These systems are essential for industries that require the removal of particulates, contaminants, and other impurities from liquids and gases under high pressure. The equipment is used in various applications, including chemical processing, oil and gas production, water treatment, and more. High pressure filtration equipment is designed to withstand extreme conditions and ensure the efficient and reliable filtration of fluids. This market is driven by the increasing demand for clean and safe industrial processes, stringent environmental regulations, and the need for high-quality end products. The equipment typically includes components such as filter housings, filter elements, and pressure control systems, all engineered to handle high pressure environments. As industries continue to evolve and prioritize sustainability and efficiency, the demand for high pressure filtration equipment is expected to grow, making it a critical component in modern industrial operations.

Aluminum Alloy, Stainless Steel in the Global High Pressure Filtration Equipment Market:

Aluminum alloy and stainless steel are two primary materials used in the construction of high pressure filtration equipment, each offering unique benefits and characteristics. Aluminum alloy is known for its lightweight properties, making it an ideal choice for applications where weight is a critical factor. It also offers good corrosion resistance, which is essential in environments where the equipment is exposed to harsh chemicals or saline conditions. Aluminum alloy filtration equipment is often used in industries such as aerospace, automotive, and marine, where both weight and durability are important considerations. On the other hand, stainless steel is renowned for its exceptional strength and resistance to corrosion, making it suitable for high pressure and high temperature applications. Stainless steel filtration equipment is commonly used in the chemical industry, oil and gas sector, and public utilities, where the equipment must withstand extreme conditions and provide long-lasting performance. The choice between aluminum alloy and stainless steel depends on the specific requirements of the application, including factors such as pressure, temperature, and the nature of the fluids being filtered. Both materials offer distinct advantages, and the selection process involves careful consideration of the operational environment and performance criteria. In the global high pressure filtration equipment market, manufacturers continue to innovate and develop advanced materials and technologies to meet the evolving needs of various industries. This includes the development of specialized coatings and treatments to enhance the performance and longevity of filtration equipment. As industries demand more efficient and reliable filtration solutions, the use of high-quality materials like aluminum alloy and stainless steel will remain a key factor in the design and manufacturing of high pressure filtration equipment.

Chemical Industry, Oil and Gas Industry, Public Utilities, Others in the Global High Pressure Filtration Equipment Market:

High pressure filtration equipment plays a crucial role in various industries, including the chemical industry, oil and gas industry, public utilities, and others. In the chemical industry, high pressure filtration equipment is used to ensure the purity and quality of chemical products by removing impurities and contaminants from raw materials and finished products. This is essential for maintaining product consistency and meeting stringent regulatory standards. The equipment is designed to handle aggressive chemicals and high pressure conditions, making it a vital component in chemical processing plants. In the oil and gas industry, high pressure filtration equipment is used to filter drilling fluids, production fluids, and other process streams. This helps to protect downstream equipment, improve operational efficiency, and ensure the quality of the final product. The equipment must be robust and reliable to withstand the harsh conditions of oil and gas operations, including high pressure, high temperature, and corrosive environments. Public utilities, such as water treatment plants, also rely on high pressure filtration equipment to ensure the safety and quality of drinking water. The equipment is used to remove particulates, microorganisms, and other contaminants from water sources, providing clean and safe water for public consumption. In addition to these industries, high pressure filtration equipment is used in various other applications, including pharmaceuticals, food and beverage processing, and industrial manufacturing. Each application has unique requirements, and the equipment must be tailored to meet the specific needs of the industry. Overall, high pressure filtration equipment is essential for maintaining the efficiency, safety, and quality of industrial processes across a wide range of sectors.

Global High Pressure Filtration Equipment Market Outlook:

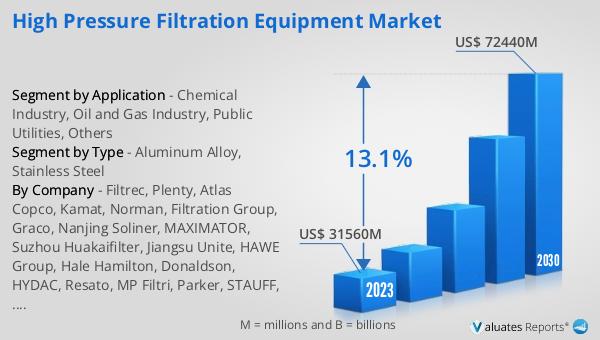

The global High Pressure Filtration Equipment market was valued at US$ 31,560 million in 2023 and is anticipated to reach US$ 72,440 million by 2030, witnessing a CAGR of 13.1% during the forecast period 2024-2030. According to our Construction Machinery research center, sales of construction machinery in Europe increased by 24% in 2021, and in 2022, the construction machinery revenue in Europe was about US$ 22 billion, while the US market sold about US$ 36 billion in construction machinery in 2022. This significant growth in the construction machinery sector highlights the increasing demand for high pressure filtration equipment, as these machines require efficient filtration systems to operate effectively and meet regulatory standards. The robust growth in the construction industry, coupled with advancements in filtration technology, is expected to drive the demand for high pressure filtration equipment in the coming years. As industries continue to prioritize efficiency, safety, and environmental sustainability, the adoption of advanced filtration solutions will play a critical role in supporting these goals.

| Report Metric | Details |

| Report Name | High Pressure Filtration Equipment Market |

| Accounted market size in 2023 | US$ 31560 million |

| Forecasted market size in 2030 | US$ 72440 million |

| CAGR | 13.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Filtrec, Plenty, Atlas Copco, Kamat, Norman, Filtration Group, Graco, Nanjing Soliner, MAXIMATOR, Suzhou Huakaifilter, Jiangsu Unite, HAWE Group, Hale Hamilton, Donaldson, HYDAC, Resato, MP Filtri, Parker, STAUFF, Schroeder Industries, Hy-Pro Filtration, ARGO-HYTOS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |