What is Global Catheter Sheath Market?

The Global Catheter Sheath Market is a significant segment within the broader medical device industry. Catheter sheaths are essential components used in various medical procedures, particularly in cardiovascular interventions. These sheaths serve as protective coverings for catheters, which are thin, flexible tubes inserted into the body to diagnose or treat medical conditions. The global market for catheter sheaths is driven by the increasing prevalence of cardiovascular diseases, advancements in medical technology, and the growing demand for minimally invasive procedures. Additionally, the aging population and rising healthcare expenditures contribute to the market's expansion. The market encompasses a wide range of products, including common sheaths, leak-proof sheaths, and peeling catheter sheaths, each designed to meet specific medical needs. The continuous innovation and development in catheter sheath technology are expected to enhance the efficiency and safety of medical procedures, thereby boosting the market's growth.

Common Sheath, Leak-proof Sheath, Peeling Catheter Sheath in the Global Catheter Sheath Market:

In the Global Catheter Sheath Market, various types of sheaths are utilized to cater to different medical requirements. Common sheaths are the most widely used type, providing a basic protective covering for catheters during medical procedures. These sheaths are typically made from flexible materials that allow easy insertion and maneuverability within the body. They are designed to minimize trauma to the patient's tissues and ensure smooth catheter navigation. Leak-proof sheaths, on the other hand, are specifically engineered to prevent fluid leakage during procedures. These sheaths are crucial in maintaining a sterile environment and preventing infections. They are often used in procedures where fluid management is critical, such as in cardiovascular interventions. The leak-proof design ensures that no blood or other bodily fluids escape, thereby reducing the risk of complications. Peeling catheter sheaths are another specialized type, designed to be easily removed or "peeled" away from the catheter once it is in place. This feature is particularly useful in procedures where the catheter needs to be repositioned or replaced without causing additional trauma to the patient. Peeling sheaths are made from materials that can be easily split or peeled apart, allowing for quick and efficient removal. The Global Catheter Sheath Market is characterized by continuous innovation and development, with manufacturers constantly striving to improve the performance and safety of their products. This includes the use of advanced materials, such as biocompatible polymers, and the incorporation of features like hydrophilic coatings to enhance the ease of insertion and reduce friction. The market is also witnessing a growing trend towards the development of customized sheaths tailored to specific medical procedures and patient needs. This customization ensures that the sheaths provide optimal performance and safety, thereby improving patient outcomes. Overall, the Global Catheter Sheath Market is a dynamic and evolving sector, driven by the increasing demand for advanced medical devices and the continuous advancements in medical technology.

Hospitals, Clinics in the Global Catheter Sheath Market:

The usage of catheter sheaths in hospitals and clinics is extensive and critical to the success of various medical procedures. In hospitals, catheter sheaths are commonly used in cardiovascular departments for procedures such as angioplasty, stent placement, and electrophysiology studies. These procedures often require the insertion of catheters into blood vessels to diagnose or treat heart conditions. The use of catheter sheaths in these procedures helps to protect the catheter, reduce the risk of infection, and ensure smooth navigation through the blood vessels. Additionally, catheter sheaths are used in other departments, such as radiology and urology, for procedures like catheter-based imaging and urinary catheterization. In clinics, catheter sheaths are used in a variety of outpatient procedures, including diagnostic tests and minor surgical interventions. The use of catheter sheaths in these settings helps to improve the efficiency and safety of the procedures, allowing for quicker recovery times and reduced risk of complications. The availability of different types of catheter sheaths, such as common sheaths, leak-proof sheaths, and peeling catheter sheaths, allows healthcare providers to choose the most appropriate sheath for each procedure, ensuring optimal patient care. The use of catheter sheaths in both hospitals and clinics is supported by continuous advancements in medical technology, which have led to the development of more advanced and specialized sheaths. These advancements have improved the performance and safety of catheter sheaths, making them an essential component of modern medical practice. Overall, the usage of catheter sheaths in hospitals and clinics plays a crucial role in enhancing the quality of patient care and improving the outcomes of various medical procedures.

Global Catheter Sheath Market Outlook:

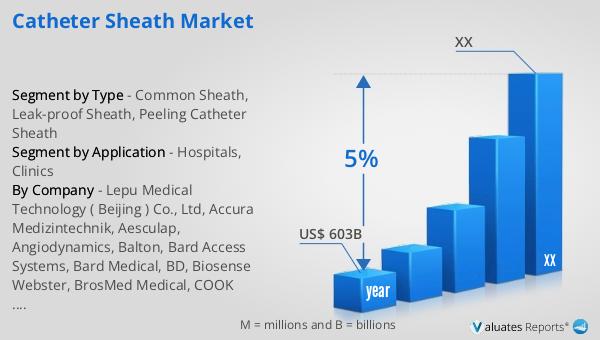

Based on our research, the global market for medical devices is projected to reach approximately $603 billion by 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for minimally invasive procedures. The aging population and growing healthcare expenditures also contribute to the expansion of the medical device market. As the market continues to grow, there will be a greater emphasis on the development of innovative and advanced medical devices, including catheter sheaths, to meet the evolving needs of healthcare providers and patients. The continuous advancements in medical technology and the increasing demand for high-quality medical devices are expected to drive the growth of the global medical device market, creating new opportunities for manufacturers and healthcare providers alike.

| Report Metric | Details |

| Report Name | Catheter Sheath Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Lepu Medical Technology ( Beijing ) Co., Ltd, Accura Medizintechnik, Aesculap, Angiodynamics, Balton, Bard Access Systems, Bard Medical, BD, Biosense Webster, BrosMed Medical, COOK Medical, Cordis |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |