What is Global Dentistry Rotary Endodontic File Market?

The Global Dentistry Rotary Endodontic File Market refers to the worldwide industry focused on the production, distribution, and utilization of rotary endodontic files used in dental procedures. These specialized tools are essential for root canal treatments, where they help in cleaning and shaping the root canals of teeth. The market encompasses various types of rotary endodontic files, including those made from stainless steel and nickel-titanium (NiTi) alloys. The demand for these files is driven by the increasing prevalence of dental diseases, advancements in dental technology, and the growing awareness of oral health. Dental professionals rely on these tools for their efficiency, precision, and ability to reduce treatment time, thereby improving patient outcomes. The market is also influenced by factors such as regulatory standards, technological innovations, and the availability of skilled dental practitioners. As dental care continues to evolve, the Global Dentistry Rotary Endodontic File Market is expected to expand, offering new opportunities for manufacturers, suppliers, and healthcare providers.

Stainless Steel Endodontic File, Nitinol Endodontic File in the Global Dentistry Rotary Endodontic File Market:

Stainless steel endodontic files and Nitinol (nickel-titanium) endodontic files are two primary types of rotary endodontic files used in the Global Dentistry Rotary Endodontic File Market. Stainless steel endodontic files are known for their rigidity and durability, making them suitable for initial canal exploration and negotiation. They are less flexible compared to Nitinol files, which can be a limitation when navigating curved root canals. However, their strength and resistance to fracture make them a reliable choice for many dental practitioners. On the other hand, Nitinol endodontic files are highly flexible and have shape memory properties, allowing them to adapt to the complex anatomy of root canals. This flexibility reduces the risk of canal transportation and ledging, ensuring a more thorough cleaning and shaping process. Nitinol files are also more resistant to cyclic fatigue, which is a common cause of file breakage during root canal procedures. The choice between stainless steel and Nitinol files often depends on the specific requirements of the dental procedure and the preference of the dental professional. Both types of files play a crucial role in endodontic treatments, contributing to the overall success of root canal therapy. The Global Dentistry Rotary Endodontic File Market continues to innovate, with manufacturers developing new designs and materials to enhance the performance and safety of these essential dental tools.

Hospital, Dental Clinic in the Global Dentistry Rotary Endodontic File Market:

The usage of rotary endodontic files in hospitals and dental clinics is a critical aspect of the Global Dentistry Rotary Endodontic File Market. In hospitals, these files are used by dental specialists and endodontists to perform complex root canal treatments. Hospitals often handle cases that require advanced dental care, including patients with severe dental infections or those undergoing multiple dental procedures. The availability of rotary endodontic files in hospital settings ensures that dental professionals can provide high-quality care, reduce treatment time, and improve patient outcomes. In dental clinics, rotary endodontic files are widely used for routine root canal treatments. Dental clinics are often the first point of contact for patients seeking dental care, and the use of these files allows general dentists to perform efficient and effective root canal procedures. The precision and reliability of rotary endodontic files help in achieving better clinical results, reducing the need for retreatments, and enhancing patient satisfaction. Both hospitals and dental clinics benefit from the advancements in rotary endodontic file technology, which include improved file designs, enhanced cutting efficiency, and increased resistance to fracture. These innovations contribute to the overall growth of the Global Dentistry Rotary Endodontic File Market, ensuring that dental professionals have access to the best tools for providing optimal patient care.

Global Dentistry Rotary Endodontic File Market Outlook:

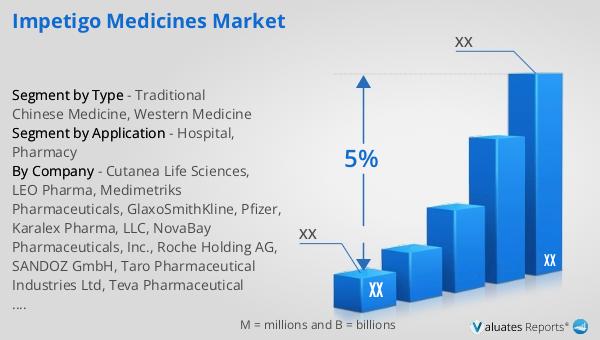

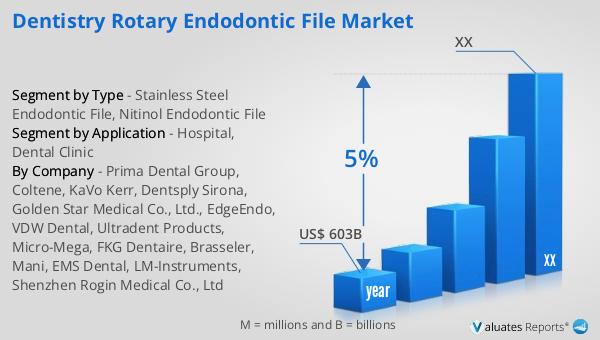

Based on our research, the global market for medical devices is projected to reach approximately USD 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory underscores the increasing demand for medical devices across various healthcare sectors, driven by technological advancements, rising healthcare expenditures, and the growing prevalence of chronic diseases. The medical device market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in modern healthcare delivery. As the market continues to expand, it presents significant opportunities for manufacturers, suppliers, and healthcare providers to innovate and improve patient care. The steady growth rate also highlights the importance of regulatory compliance, quality assurance, and strategic partnerships in maintaining a competitive edge in this dynamic industry.

| Report Metric | Details |

| Report Name | Dentistry Rotary Endodontic File Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Prima Dental Group, Coltene, KaVo Kerr, Dentsply Sirona, Golden Star Medical Co., Ltd., EdgeEndo, VDW Dental, Ultradent Products, Micro-Mega, FKG Dentaire, Brasseler, Mani, EMS Dental, LM-Instruments, Shenzhen Rogin Medical Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |