What is Global Biodegradable Food Service Disposables Market?

The Global Biodegradable Food Service Disposables Market refers to the industry that produces and sells disposable items used in food service, which are designed to break down naturally and reduce environmental impact. These items include plates, cups, cutlery, and packaging materials made from biodegradable materials such as paper, plant-based plastics, and other organic substances. The market is driven by increasing awareness of environmental issues, government regulations, and consumer demand for sustainable products. As more people become conscious of the negative effects of plastic waste on the environment, there is a growing preference for biodegradable alternatives. This market is expanding globally, with significant growth in regions like North America, Europe, and Asia-Pacific. Companies in this market are continuously innovating to improve the performance and cost-effectiveness of biodegradable products, making them more accessible to a wider range of consumers and businesses.

Paper, Plastic, Others in the Global Biodegradable Food Service Disposables Market:

In the Global Biodegradable Food Service Disposables Market, products are primarily categorized into three main types: paper, plastic, and others. Paper-based disposables are widely used due to their natural biodegradability and ease of recycling. These include items like paper plates, cups, and napkins. They are often made from renewable resources such as wood pulp and are designed to decompose quickly in composting conditions. Paper products are popular in various settings, including restaurants, cafes, and events, due to their eco-friendly nature and cost-effectiveness. On the other hand, biodegradable plastics are made from plant-based materials like corn starch, sugarcane, and potato starch. These plastics are designed to break down more quickly than traditional petroleum-based plastics, reducing their environmental impact. Biodegradable plastic disposables include items like cutlery, straws, and food containers. They offer the convenience of traditional plastics but with a reduced carbon footprint. However, the decomposition of biodegradable plastics often requires specific conditions, such as industrial composting facilities, which can limit their effectiveness in reducing waste. The "others" category includes a variety of biodegradable materials such as bagasse (a byproduct of sugarcane processing), bamboo, and palm leaves. These materials are used to create sturdy and attractive disposable items like plates, bowls, and trays. Bagasse, for example, is highly durable and can withstand hot and cold temperatures, making it suitable for a wide range of food service applications. Bamboo and palm leaf products are also gaining popularity due to their natural appearance and strength. These materials are often used in upscale dining and catering services where presentation is important. Each type of biodegradable disposable has its own set of advantages and challenges. Paper products are widely accepted and easy to compost, but they may not be as durable as plastic alternatives. Biodegradable plastics offer the convenience of traditional plastics but require specific conditions to decompose effectively. Other materials like bagasse, bamboo, and palm leaves provide a balance of durability and eco-friendliness but may come at a higher cost. Overall, the choice of material depends on the specific needs of the food service operation, including factors like cost, durability, and environmental impact. As technology and consumer preferences continue to evolve, the market for biodegradable food service disposables is likely to see further innovation and diversification.

Bakery, Convenience Store, Others in the Global Biodegradable Food Service Disposables Market:

The usage of biodegradable food service disposables is particularly significant in areas such as bakeries, convenience stores, and other food service establishments. In bakeries, biodegradable disposables are used for packaging and serving a variety of baked goods. Items like paper bags, boxes, and trays made from biodegradable materials help reduce the environmental impact of packaging waste. These products are not only eco-friendly but also help maintain the freshness and quality of baked goods. Biodegradable packaging is especially important in bakeries that emphasize organic and natural ingredients, as it aligns with their overall commitment to sustainability. Convenience stores also benefit from the use of biodegradable food service disposables. These stores often sell a wide range of ready-to-eat and packaged foods, which require disposable packaging for convenience and hygiene. Biodegradable options such as paper cups, plates, and cutlery provide a sustainable alternative to traditional plastic disposables. This is particularly important in urban areas where waste management is a significant concern. By offering biodegradable disposables, convenience stores can appeal to environmentally conscious consumers and reduce their overall environmental footprint. Other food service establishments, including restaurants, cafes, and catering services, also utilize biodegradable disposables to enhance their sustainability efforts. In restaurants and cafes, items like biodegradable straws, cutlery, and takeout containers are becoming increasingly popular. These products help reduce plastic waste and appeal to customers who prioritize eco-friendly practices. Catering services, which often handle large events and gatherings, use biodegradable plates, bowls, and trays to minimize waste and promote sustainability. The use of biodegradable disposables in these settings not only helps protect the environment but also enhances the brand image of the establishment. Customers are more likely to support businesses that demonstrate a commitment to sustainability, making biodegradable disposables a valuable investment. Overall, the usage of biodegradable food service disposables in bakeries, convenience stores, and other food service establishments is driven by the need to reduce environmental impact and meet consumer demand for sustainable products. As awareness of environmental issues continues to grow, the adoption of biodegradable disposables is likely to increase, further supporting the global market for these products.

Global Biodegradable Food Service Disposables Market Outlook:

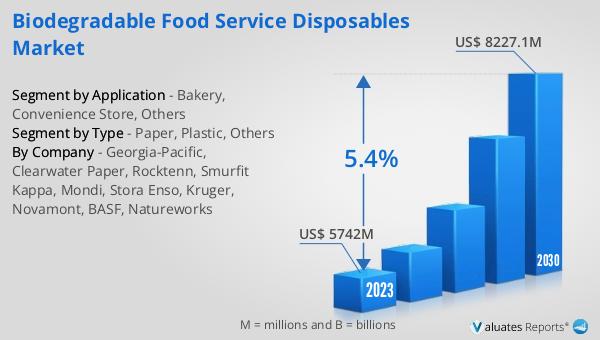

The global Biodegradable Food Service Disposables market was valued at US$ 5742 million in 2023 and is anticipated to reach US$ 8227.1 million by 2030, witnessing a CAGR of 5.4% during the forecast period 2024-2030. This market outlook indicates a significant growth trajectory driven by increasing consumer awareness and demand for sustainable products. The rising environmental concerns and stringent government regulations are pushing businesses to adopt biodegradable alternatives to traditional plastic disposables. As a result, the market is expected to expand substantially over the coming years. Companies operating in this market are focusing on innovation and development of cost-effective, high-performance biodegradable products to cater to the growing demand. The projected growth also highlights the potential for new entrants and existing players to capitalize on the expanding market opportunities. Overall, the market outlook for biodegradable food service disposables is positive, with substantial growth expected in the coming years.

| Report Metric | Details |

| Report Name | Biodegradable Food Service Disposables Market |

| Accounted market size in 2023 | US$ 5742 million |

| Forecasted market size in 2030 | US$ 8227.1 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Georgia-Pacific, Clearwater Paper, Rocktenn, Smurfit Kappa, Mondi, Stora Enso, Kruger, Novamont, BASF, Natureworks |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |